First, a question:

What’s happening around us? How did we get here? This question has most likely crossed your minds while reading the news over the past weeks, or let’s be honest, years. At times, the headlines can make it feel as though we are living in a parallel‑universe storyline. Many of us in Luxembourg would probably have preferred to live in the world once described as the “End of History”: a world where economic integration deepened, liberal democracy spread, and geopolitics slowly faded into the background.

But, well, here we are.

War in Ukraine, Palestine, and Iran. Geopolitical tensions. Blockages in the strait of Hormuz. Economic decline. Europe ageing. Productivity growth stalled. Investment has declined.

Over the past fifteen years since the global financial crisis, European GDP has grown far more slowly than that of the United States, creating a structural gap of around 20 %. This is a worrying trend. As stated by Carlo Thelen, Director General, Chamber of Commerce, in his welcome speech at the 19th Journée de l’Economie, Luxembourg*, this divergence with the US is now visible not only in macroeconomic charts, but in living standards. Hitting people where it counts most.

The risk, he argued, is not a sudden collapse, but a gradual erosion: a scenario in which others move faster, invest more decisively, and shape the rules while Europe hesitates.

For small, highly open economies such as Luxembourg, staying competitive is simply a fact of life: when growth slows, investment fragments, and geopolitical risks intensify, meaning the margin for complacency disappears. Stability can no longer be taken for granted and must be actively sustained.

“What does sovereignty mean in today’s interconnected and often turbulent world? Can it protect Europe from external shocks, or does long-term stability depend on collaboration?”. These are two of the big questions discussed at the 19th Journée de l’Economie, that took place on 18 March 2026 at the Chamber of Commerce in Luxembourg-City and aims to explore whether sovereignty is the right path and whether Luxembourg can save Europe. This blog is inspired by the keynote speeches and panel discussions from that day.

The new age of empires

We may not like to admit it, but the global order did not shift overnight.

The transformation began already in the early 2000s, when the belief that economic integration would naturally produce political convergence started to erode.

The 2008 financial crisis was a decisive moment in this process. It exposed the limits of a model built on the assumption that markets alone could discipline states and align interests. Instead, the crisis accelerated a return to state power, strategic intervention, and economic nationalism (more on this below in Jeromin Zettelmeyer, Director, Bruegel keynote)

Around the same time, Russia, which had only recently reintegrated into the global political system, returned to explicit power politics (first in Georgia and later in Ukraine).

China’s trajectory provided a third, equally consequential signal. As China’s economic weight grew in the 2010s, it became clear that Beijing was benefiting from global markets without embracing the norms required for fair competition, integrating selectively while reinforcing state control. These developments were signs that collaboration and multilateralism were no longer sufficient to structure international relations, marking the re-emergence of empires as the central actors of world affairs. This was the conclusion Guy Verhofstadt, former Prime Minister of Belgium and Member of the European Parliament, delivered to a rap audience at the Journée de l’Economie.

In today’s new order, he explained, it is no longer 199 nation states collectively shaping the future of humanity based on a shared set of rules.

Instead, the direction of the world is increasingly driven by competition between large power blocs, “where power matters more than values, and security more than sovereignty,” as Mr Verhofstadt argued. Today, those empires are the United States, China, Russia, and with others, such as India, following.

As both a result and a prerequisite of this shift, the global economy is fragmenting. Already under the Biden administration, export controls, subsidies, and derisking strategies accelerated the same logic that, ultimately, only power is power, to put it in the words of Cersei Lannister (from Game of Thrones).

Overlaying this is a deeper conflict: an existential struggle between democracy and autocracy. Not only abroad, but within Europe itself. Liberal democracies are weakening from the inside as populism becomes mainstream. Elections, it seems, are no longer about policy direction, but about democracy itself.

In short: Europe — fragmented, idealistic, and anchored in values — is not prepared for this world order.

To survive a new age of empires, Europe must itself change fundamentally, or so Guy posited. Not into a traditional empire of domination, but into an “empire of the good”, that is capable of acting, defending itself and shaping outcomes.

To become such an empire, Europe needs to go through three core transformations.

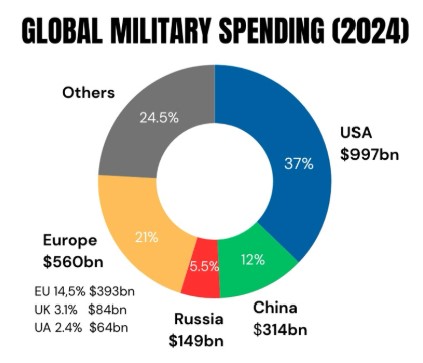

- The first is defence. Europe already spends enormous sums on defence (roughly €560 billion annually when including the UK and Ukraine) yet remains dramatically inefficient. With nearly thirty armies and over a hundred different weapons systems, Europe achieves barely a fraction of the operational effectiveness of the United States or China, which rely on around twenty‑five systems each. Duplication, not under‑spending, is the real problem.

The solution is not incremental coordination, but a qualitative leap: a European Defence Community acting as a European pillar of NATO that truly enables a strategic autonomy vis-à-vis the United States. “If Europe cannot defend Estonia without American leadership, then sovereignty remains an illusion,” Mr Verhofstadt argued. Defence integration would also allow Europe to align military needs with industrial capacity, instead of letting national champions compete against one another.

Europe collectively spends more than half of US defence expenditure yet delivers significantly less integrated capability.

- The second transformation concerns the European economy and single market. “The single market works for chocolate and cars, but not for data, digital services or capital”. Mr Verhofstadt says. Europe may be legally integrated, but economically it remains fragmented. This directly constrains innovation: while around €1.7 trillion is mobilised annually in the United States, Europe attracts only a fraction of that amount. Without genuinely unified capital markets and a single framework for digital regulation, European firms continue to scale abroad rather than at home.

The same is true for data. Europe generates vast quantities of it yet lacks the structures to monetise it effectively. Value creation takes place elsewhere, where markets are larger, rules more coherent, and capital more readily available. In consequence, Europe regulates at continental scale but competes at national scale: a mismatch that systematically weakens its economic base.

- The third reform is institutional. Europe’s decision making remains trapped in unanimity, producing what Mr Verhofstadt described as a pattern of “too little, too late.” Some policy areas, such as trade work because it is federal, but foreign policy, defence and crisis financing stall because a single veto can block collective action.

Changing the treaties however is unlikely. But enhanced cooperation and a “coalition of willing”, as it happened with Schengen or the euro, remains both legal and necessary in a world that will not wait for consensus.

European economic nationalism: Made in China?

Geopolitics tells us why Europe feels under pressure, economics shows us how that pressure is already materialising.

Jeromin Zettelmeyer’s keynote started by unpacking a confusion that increasingly dominates the European debate. Economic nationalism rests on the idea that prosperity is a zero-sum game: that one country’s success necessarily comes at another’s expense.

This way of thinking was largely rejected after the Second World War. In Europe in particular, economic policy has traditionally pursued a different goal: raising growth and welfare through openness, competition, and integration.

There was one notable exception: developing economies were long granted room for protection under the “infant industry” argument. The goal was that temporary shelter from competition would allow some countries to catch up. That rationale was embedded in the rules of the GATT and later the WTO.

That world is over.

China is no longer an economy in need of protection. It has caught up, and it has done so at unbelievable scale! Yet it continues to deploy a form of economic nationalism well beyond what the “infant industry” logic would justify. State support, excess capacity, and an export‑led response to weak domestic demand have produced a rapidly growing trade surplus, particularly in manufacturing.

This is not an abstract macroeconomic concern: Chinese firms increasingly compete head‑to‑head with European producers in precisely the same product categories. This matters because it changes the nature of the problem: even if Chinese overcapacity eases, structural competition will not.

It also reveals an uncomfortable reality: Europe will never return to where it stood ten years ago. China has already moved into a lot of spaces Europe once occupied.

The implication, Mr Zettelmeyer argued, is that Europe cannot afford a single‑objective response. It requires holding three goals simultaneously:

- The first is to slow the immediate shock of cheap imports or what Mr Zettelmeyer called the “Chinese steamroller”: the logic here is defensive but pragmatic: when a surge of artificially cheap imports threatens to hollow out entire sectors, Europe may need breathing space to avoid losing productive capacity irreversibly.

- The second objective is structural transformation: even under the most benign scenario Europe’s industrial model must change. Future growth will depend less on volume production and more on specialisation, innovation, and high‑spillover activities. Protection alone cannot deliver this shift; in fact, the wrong kind of protection risks even delaying it.

- The third objective is preserving rules‑based trade: Europe remains an open, energy‑importing, and export‑dependent economy. Any next growth model will still rely on access to global markets and on diversifying away from excessive dependency on China. Trying to produce everything domestically would be economically unviable.

These objectives inevitably conflict. Heavy or permanent protection may shield established companies, but slow adjustment and undermine the very trade system Europe depends on. Conversely, doctrinaire openness risks accelerating deindustrialisation before new growth engines are in place.

Mr Zettelmeyer’s conclusion was therefore deliberately nuanced. Some protection may be necessary, but it should be narrow, temporary, and rules‑based. WTO‑compatible safeguards, rather than permanent tariffs or “Buy European” mandates, are better suited to addressing temporary import surges without destroying the trading system. Local content requirements may sound assertive, but they are legally fragile, economically costly, and ultimately self-defeating.

The uncomfortable truth is that structural change is unavoidable. The question is not whether Europe will adapt, but whether policy will actively shape that adaptation, or merely react to it once the costs have already materialised.

Sovereignty without illusion

After Mr Verhofstadt’s diagnosis of a world governed by power, and Mr Zettelmeyer’s analysis of structural economic competition, Luxembourg Prime Minister Luc Frieden’s intervention brought the debate back to first principles.

Sovereignty, he argued, is too often discussed as a legal or symbolic concept. It comes down to something much simpler: economic strength.

Without prosperity, there is no capacity to invest, to innovate, or to defend. And without that capacity, Europe cannot secure its interests, its values, or its security, no matter how often it invokes sovereignty.

Yet sovereignty does not mean isolation. In today’s world, no European country — and certainly not Luxembourg — can be sovereign on its own. Europe’s comparative advantage has never been self‑sufficiency, but its ability to organise interdependence: to turn openness into leverage rather than vulnerability.

This becomes quite obvious in the domains that now define power. Energy security, artificial intelligence, defence technologies, critical raw material: none of these challenges can be mastered at national scale.

For Frieden, the answer therefore lies neither in a Fortress Europe nor in a return to naïve openness. What is needed is a more deliberate and more strategic form of cooperation: pooling demand where scale matters, aligning investments where fragmentation is costly, using public procurement as an instrument of policy rather than an administrative afterthought, and simplifying regulation so that ambition does not collapse under its own complexity.

Seen from this perspective, Luxembourg’s role becomes clearer, and more modest. Not as a would-be champion of scale, but as a platform of precision.

Now, can Luxembourg save Europe?

Quite frankly, no.

Luxembourg cannot, by itself, resolve Europe’s demographic decline, close its investment gap, or reverse the fragmentation of the global order. Pretending otherwise would be another form of illusion.

But that is not the right benchmark. The real question is whether Luxembourg can shape how Europe adapts.

Once slogans are stripped away, strategic autonomy looks far less like self-sufficiency and far more like priority setting. It is not about producing everything everywhere or to dominate every step of every value chain, but about identifying critical dependencies, deciding which ones truly matter, and ensuring that they are managed rather than ignored.

In fact, after all this pessimism, we are not doing so bad. Many of the instruments Europe needs already exist. From investment screening and defence initiatives to industrial coordination and programmes designed to de‑risk private capital, the toolbox is fuller than often assumed, as explained by Anne Calteux.

The bottleneck lies elsewhere: in speed, coherence, and execution. Fragmentation between national systems, regulatory regimes, and investment incentives continues to dilute impact.

This is where small member states punch above their weight. Influence does not come from scale alone. It also comes from credibility, from the ability to convene stakeholders across borders, and from providing reliable platforms where public priorities and private capital can meet. Europe’s problem is not a lack of capital, but its dispersion — and the difficulty of mobilising it quickly for projects that serve a strategic purpose.

That, ultimately, defines Luxembourg’s role. Not as a champion of scale, but as a platform of precision. A place where financial infrastructure, regulatory reliability, and technical expertise can help turn European objectives into investable, operational realities.

This is what will save Europe: It will be shaped slowly and imperfectly by the choices made now.

*The “Journée de l’Economie” is organised in Luxembourg by the Ministry of the Economy, the Luxembourg Chamber of Commerce, IDEA and FEDIL – The Voice of Luxembourg’s Industry with the support of PwC Luxembourg.

Frequently Asked Questions:

- Why is Europe said to be falling behind economically?

Over the past 15 years, Europe has experienced significantly slower economic growth than the United States, resulting in a structural GDP gap of around 20%. This divergence reflects weaker productivity growth, declining investment, demographic ageing, and increasing geopolitical uncertainty. The concern is not sudden collapse, but a gradual erosion of competitiveness and living standards over time.

- What has changed in the global geopolitical landscape?

The global order has shifted from cooperation-driven globalisation to competition between major power blocs, including the United States, China, and Russia. Events such as the War in Ukraine highlight the return of geopolitics as a dominant force. Economic integration no longer guarantees stability, and power politics increasingly shapes global trade, security, and technology.

- What are Europe’s main internal weaknesses?

Despite deep integration, Europe remains structurally fragmented in key areas:

- Defence: Multiple national systems and duplicated capabilities reduce efficiency;

- Economy: The single market is incomplete for digital services, capital, and data; and

- Governance: Decision-making is slowed by unanimity requirements.

This fragmentation limits Europe’s ability to scale innovation, mobilise investment, and respond quickly to external shocks.

- What reforms does Europe need to remain competitive?

Europe must pursue coordinated structural transformation across three areas:

- Defence integration: Improve efficiency and interoperability through stronger coordination and shared capabilities;

- Economic deepening: Complete the single market, especially in capital, data, and digital services; and

- Institutional reform: Enable faster decision-making through flexible cooperation mechanisms rather than strict unanimity.

The goal is not isolation, but stronger collective capacity to act in a fragmented global environment.

- What role can Luxembourg play in Europe’s transformation?

While Luxembourg cannot resolve Europe’s structural challenges alone, it can play a meaningful enabling role. Its strength lies in acting as a platform for precision—connecting capital, institutions, and industry to turn European priorities into investable and executable projects.

In Europe’s future model, influence depends not only on scale, but also on credibility, coordination, and execution capacity.

What we think

Europe stands ready to convert structural challenges into opportunity, deepening integration, fostering innovation, and using its values and openness to drive renewed global leadership.

Journée de l’Economie in Luxembourg this year touched on the burning issues being discussed across Europe right now. The keynote speakers clearly heralded a call that the time has come to transform European priorities into impactful projects and discussion into unified actions that will make a stronger, more competitive future for Europe.