An important (and often overlooked) element in infrastructure financing

Infrastructure financing and insurance capital are often described as a natural match. In practice, however, this relationship is more complex. Solvency II, through its focus on risk and regulatory capital, influences the boundaries of what insurers can invest in, often exposing gaps between theoretical alignment and practical experience.

Infrastructure assets are long term and capital-intensive investments, requiring significant upfront funding commitments. Institutional investors are often regarded as a go-to place for infrastructure financing. This resonates strongly with insurance and reinsurance companies, particularly life and life alike, whose liabilities are themselves long-dated and cash-flow driven, hence they are in need of predictable cashflows as well as an opportunity to earn an “illiquidity premium”. In principle, this creates a strong (theoretical) structural match between infrastructure financing needs and insurers’ investment profiles.

In practice, the allocation of insurance investments cannot be considered independently of prudential considerations. Insurers must hold regulatory capital commensurate with the risks they assume. The fundamental principle is that same risk attracts the same capital charge; different risks attract different charge. As a result, investments with comparable return profiles can still carry materially different insurance capital requirements. This directly influences how insurers construct their portfolios: strategic asset allocation is driven not only by yield, but also by capital charge they attract.

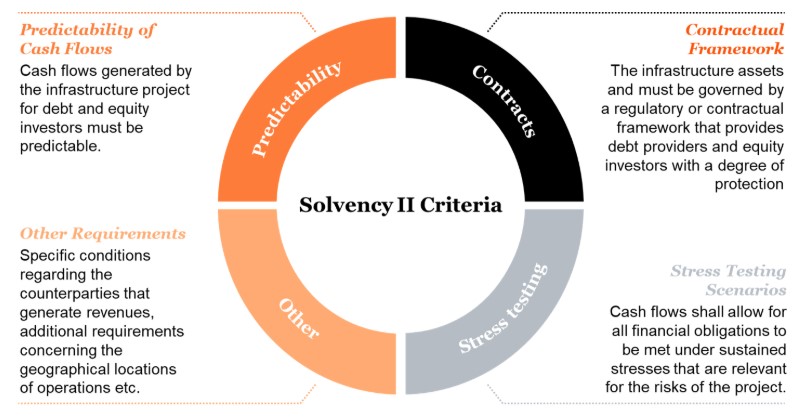

In Europe, these considerations are governed by Solvency II, the prudential framework applicable to (re)insurance undertakings. Solvency II introduced a specific treatment for qualifying infrastructure investments, under the standard formula, reflecting their (relatively) better risk characteristics as well as broader policy objectives to support long–term investment in the real economy. This treatment combines relatively favourable capital charges with clearly defined eligibility criteria and enhanced risk management expectations. To qualify, an investment must meet a set of eligibility criteria, including:

How has this worked in practice over recent years?

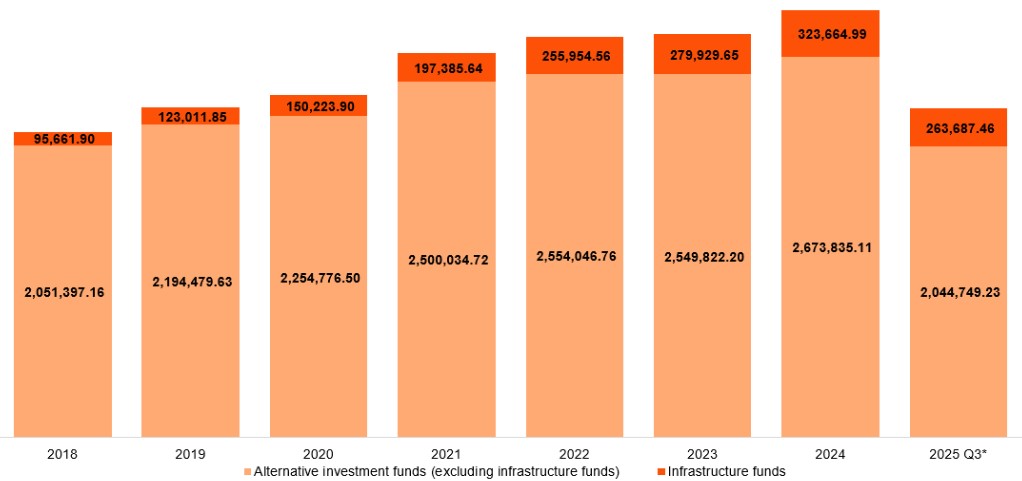

Insurer appetite for alternative investments has grown steadily in recent years. Allocations to infrastructure have increased materially, relatively outpacing other alternative categories, although from a relatively small base. As Figure 1 shows, total investments in alternatives increased by 40% from 2018 to 2024, while allocations to infrastructure alternative assets more than tripled.

On the surface, this would suggest that regulatory treatment has been efficient in reducing barriers to infrastructure investments since the introduction of the dedicated infrastructure category in 2016. Nevertheless, compared with insurers’ overall investment portfolios, infrastructure remains far from a core holding.

EEA insurers’ allocations to fund-based alternative assets (EUR millions)

*2025 figures are based on data available up to Q3 and therefore understate the full-year investment flows.Source: EIOPA

Despite years of supportive regulatory treatment under Solvency II, infrastructure continues to be under–represented in insurers’ portfolios when compared with its theoretical appeal. This raises an important question for both insurers and infrastructure sponsors: if the regulatory framework is supportive, why does the gap still exists?

What have been some common challenges?

Several structural frictions continue to limit the translation of appetite into meaningful allocation.

- Insurers and infrastructure companies / asset managers often do not speak the same language or metrics. Asset managers are used to thinking in terms of projects, execution, internal rates of return and deal structuring. Insurers, on top of these, also consider impact on solvency ratios, capital shocks, cash flow matching and governance. Without translation between these perspectives, potentially eligible infrastructure can remain practically inaccessible.

- Limited supply and not fit for insurer appetite.Historically, there has also been a problem of supply: few projects, even fewer good projects, where risk-return would fit. Further, there were few infrastructure projects that were designed with a bank regulatory mindset as compared to insurance- oriented one (both having their own nuances).

- Infrastructure assets under Solvency have specific criteria. Infrastructure is not defined by branding or sector alone. To qualify, assets must provide or support essential public services to support the well-being of the population (this may cover services in all of the following areas: health, safety, security, economic and social), be long term in nature, and be sufficiently capital intensive.

- Eligibility under Solvency II is often misunderstood or assumed rather than demonstrated. Many of the underlying Solvency II eligibility conditions such as cash flow predictability, robustness of investor protections, counterparty exposure and geographic concentration are not fully understood or assessed early enough and are often analysed only late in the investment process. Crucially, these characteristics must hold throughout the life of the investment and be evidenced on an ongoing basis, rather than implied or assumed at inception.

- Creation of additional risks.Infrastructure financing can introduce additional risks that insurers perceive as harder to manage, including liquidity constraints, valuation uncertainty and limitations on exit flexibility.

How some participants have successfully closed the gap

Experience shows that successful infrastructure financing strategies aimed at insurers do not start with individual assets, but with objectives.

A recurring lesson is the importance of addressing a set of foundational questions upfront, including:

- What is the nature of business written by (re)insurers and how will infrastructure cashflows align with the insurers’ liability profiles, in particular from a duration and currency matching perspective.

- What Solvency II treatment is being targeted, and if/how this fits with the insurer’s own objectives (e.g. equity versus debt exposures, what brings in capital optimisation).

- How governance, risk oversight and ongoing compliance will be organised and managed over time for insurer’s risk capital calculation and reporting.

- How liquidity or exit options could be achieved, should circumstances or strategy evolve.

It has also been observed that financing is most effective when Solvency II considerations are embedded early in the investment assessment process. High-level indicative treatment is typically assessed as part of initial due diligences and refreshed regularly to reflect portfolio evolution, (any) regulatory developments, and jurisdiction specific nuances.

Another best practice is recognising that different partnership models reflect different levels of insurer sophistication and expectations. Larger insurers may favour direct investments or bespoke partnerships, especially when they may have internal models for explicit capital shock calibrations. Others may rely on funds structures, where the Solvency II standard formula, supported by robust look-through, provides a common reference point.

An equally important factor observed has been planning for change. Exit strategies – whether through asset rotation, secondary transactions or investor replacement – should be considered as part of the initial design, to also allow for any change in dynamic of insurer’s portfolio.

Bringing it together amid recent developments

Infrastructure, when properly structured, should not be viewed as an exotic alternative asset. When the right questions are asked and a shared understanding is developed, infrastructure can become a natural extension of an insurer’s balance sheet, enabling the effective translation of appetite into allocation.

Recent regulatory and market developments reinforce the increasing importance of this conversation. While infrastructure as an asset class has long been recognised under Solvency II, the 2020 review and subsequent reforms have reinforced a broader policy direction aimed at facilitating insurers’ participation in long‑term investment in the real economy.

One example is the removal of certain qualitative requirements for Long-Term Equity Investment (LTEI) to encourage long term equity investment, while offering lower capital charge for (re)insurers. In this context, infrastructure financing only aligns naturally with reforms that seek to better reflect long‑term investment horizons within a risk‑based prudential framework.

From insurers’ perspective, market dynamics are further evolving. Life insurers continue to seek long‑dated predictable, cash‑flow‑driven assets to support liability matching, particularly in mature markets where traditional business models face structural and cost pressures. This raises a strategic choice: return capital, take materially more risk, or deploy capital more efficiently in hope of higher yet stable returns.

At the same time, in an environment of rising geopolitical uncertainty and expanding public borrowing, long term investments must be assessed holistically – across funding costs, credit conditions, liquidity and balance sheet interactions.

As Solvency II and geopolitical situations continues to evolve, those who understand both insurance and infrastructure will be best placed to bridge long‑term capital with long‑term assets. The opportunity is real, but so is the discipline required to capture it. Because existence of finance may not be the constraint. Alignment is.

Frequently Asked Questions:

1. Why do infrastructure investments appeal to (re)insurers under Solvency II?

Infrastructure investments offer long-term, predictable cash flows that align well with insurers’ long-dated liabilities. Solvency II also provides favourable capital treatment for qualifying infrastructure assets, making them attractive from both a yield and capital efficiency perspective.

2. If Solvency II is supportive, why is infrastructure still underrepresented in insurer portfolios?

Despite favourable regulation, several frictions remain, including differences in “language” between insurers and asset managers, limited suitable deal supply, complex eligibility requirements, and concerns around liquidity, valuation, and exit flexibility. These factors often prevent theoretical appetite from translating into actual allocations.

3. What helps insurers successfully invest in infrastructure assets?

Success depends on early integration of Solvency II considerations, clear alignment with liability profiles, strong governance and risk frameworks, and well-planned exit strategies. Partnerships that translate infrastructure projects into insurance capital terms are key to closing the gap between interest and investment.

At its core, this is about bringing together different worlds – infrastructure entities, funds, (re)insurers – that do not naturally speak the same language, each shaped by different metrics, rules and expectations.

The increased demand from insurers for higher long-term yields should encourage asset managers to develop attractive products. We can already see this happening.