Why have Luxembourg authorities implemented the VAT Group regime until now and what does it mean for you, companies and me?

The draft bill N° 7278 implementing the VAT Grouping regime into Luxembourg VAT Law was voted on 26 July. We consider this as one of the most interesting developments in this area for the last couple of years.

We thought it would be very helpful to share with you what we have learnt during the “gestation period” of the draft bill regarding the content, the context and the potential opportunities and challenge of the regime.

The result is this infographic with eight things to keep in mind about the VAT Group.

Before starting out on the VAT Grouping road…

As with most new regulations, the VAT Grouping brings opportunities and challenges to the journey. While the advantages seem to be clear, you may also encounter disadvantages. Think about the situation for example when one of the group members happens to be a passive holding company, and Luxembourg VAT should now be reverse-charged by that company member of a new VAT group on services purchased from suppliers established outside of Luxembourg, when before this was not the case. Think also about the possible impact on head-office to branches supplies, or on the members’ VAT recovery profile.

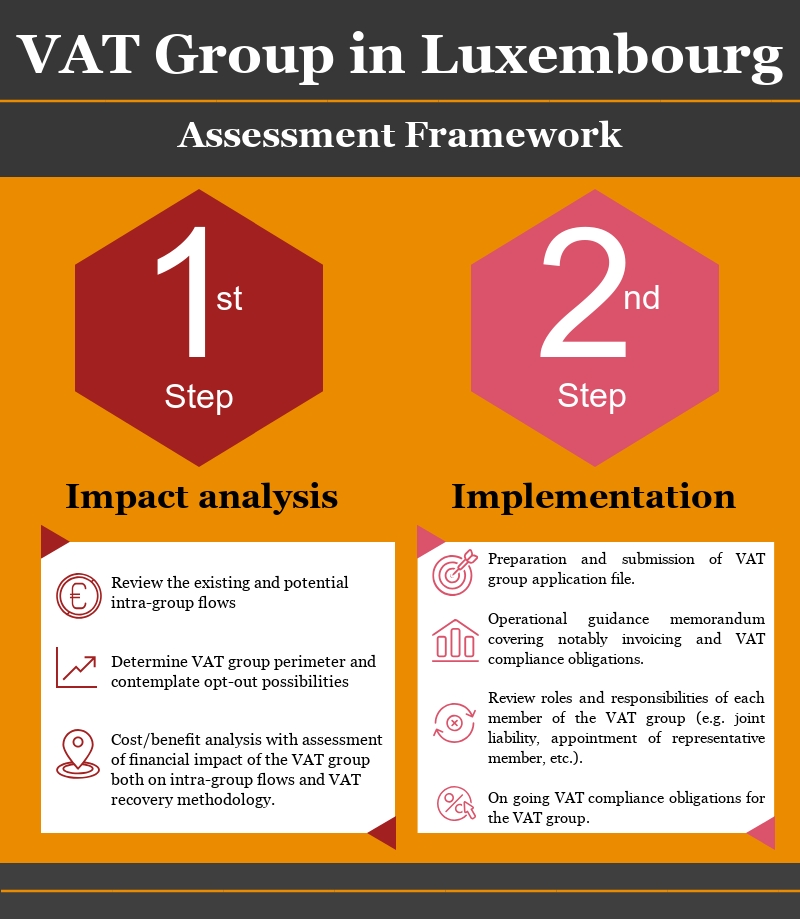

We invite you to assess carefully weather a VAT Group will be beneficial for you. Take a look at the assessment framework VAT Group in Luxembourg:

What we think

Fréderic Wersand, VAT Partner at PwC Luxembourg

VAT Groups are widely used in other Member States as a way to mitigate irrecoverable VAT costs and cash flow effects on intra-group charges. But not all companies will have a business case, and downsides can sometimes exceed financial benefits. As the new regime is now available, let’s have a look at it sooner rather than later, and see if this is fit for purpose for your own business.