It’s interesting to think about what externalities meant to business years ago, before the current context with SDGs, corporate responsibility and ESGcriteria gaining ground. The general opinion was that they had no impact on profitability.

Indeed, for many decades, economists considered the impact of production and consumption on the environment as an externality. Business operational processes weren’t supposed to suffer any direct or indirect consequences.

However, research based on practical business cases show the opposite. The consideration of externalities has become necessary for any attempt to match business operational processes with sustainability.

For any company thinking long term, it makes sense to consider the impact it has on the environment and society to increase the sustainability of the business. Who can do business when there’s no fertile land that can produce, a large middle class wealthy enough to invest, a healthy population to insure, safe cities to visit and nature to enjoy (or even survive), and so on?

No. Embedding sustainability in both operations and strategy shouldn’t be considered an act of benevolence any longer, if ever it was. Neither is it a response to popular outcry or an almost feverish obsession of regulators to protect Earth.

It’s a smart business decision to maintain.

This article takes you through a quick yet interesting review of how the concept of externalities have been incorporated into business and, more specifically, into financial services. Equally, it introduces to you the concept of “shared value”, and why it matters for sustainability.

Interiorising Externalities: the key concepts

Also called “spillover effects”, externalities are, simply put, the positive or negative consequence of any industrial or commercial activity which affects third parties without being reflected in market prices.

For example, waste is an externality that derives from consumption; carbon emissions from factories and cattle raising are an externality resulting from production activities. There is a caveat to keep in mind when it comes to externalities: third parties –- any individual, organisation, property owner, or resource that is not the producer or consumer – can barely control those consequences or impacts, their emergence and the amplitude or extent of them. But, by investing sustainably, this status quo can be challenged.

Negative externalities are—commonly— costs. And because price markets don’t consider the cost of negative externalities, this exclusion generates a gap between the gain or loss of private individuals and of the society as a whole.

Considering externalities in the profitability equation

In 1995,Stuart Hart was one of the first economists who shifted the focus towards a natural-resource-based view, where the capabilities of a firm to produce a good are naturally constrained by the biophysical environment (1).

For instance, manufacturers and service companies have to deal with naturally limited resources of raw material and a limited supply of skilled employees due to demographic changes or technological advancements. Research has proven there is evidence of the direct effect that externalities have on the market price of a firm.

In 2005, a study by Karpoff, Lott and Wehrly showed that businesses violating environmental regulations suffer significant losses in the firm equity market value (2). Further studies show that investors incorporate the sustainability performance of a firm into the firm’s market price and, ultimately, its equity cost of capital (3).

A more recent study from 2017 confirmed that finding by analysing the stock market’s reaction of news related to ESG factors (4).

What affects a firm’s market value most?

We’ve seen that environmental and social externalities seem to have a significant effect on a firm’s’ value. But what’s the main influencing factor?

The amount of the decrease in firm value is largely relative to the volume of the regulatory penalties. In fact, although reputational concerns contribute to this decrease, it’s to a small extent compared to the effect of legal and regulatory penalties, as Karpoff and his team, legal and regulatory suggest in their research.

Thus, the impact of externalities on firm value is significantly influenced by governmental regulations and taxation incentives. This fact calls for new business models where businesses properly identify the effects of externalities and incorporate them into their strategic and operational setup.

Thinking sustainability

Nowadays, the terms Corporate Responsibility (CR) and Environment, Social and Governance (ESG) are used to highlight externalities.

In the early stages of the battle for sustainability to claim a space at the business strategy table, these terms were used to describe a society´s expectation that firms consider such external effects into their operational planning.

But currently, businesses themselves are increasingly asking companies to consider these effects because of the impact they will have on operational capabilities and, ultimately, profitability.

Farmers having to incorporate the increasing likelihood of drought or flood when planning production, investing or defining prices could be an example Loan providers, functioning as intermediaries between investors and capital acquirers, need to incorporate risks resulting from climate change in order to estimate the default probability of their debtors.

Fund managers are required to consider these risks when estimating the expected return of their funds when investing in climate-affected sectors. Ultimately, the effects externalities have on financial performance influence every entity— up and down the channel of capital flow.

In 2006, Porter and Kramer took the first step in defining the concept of “shared value”. According to their approach, a firm uses investments in ESG as a new way to create a competitive advantage and, thus, generate a value not only for its external but also for its internal stakeholders (5).

To achieve a shared value, a business has to act ahead of already imposed legal regulations and develop innovative business models and products that allow them to create competitive advantage or bring about a different value to its clients, competitors’ clients and other stakeholders.

A suggested first step to embrace the shared value approach is to perceive policy and technology uncertainty as a chance or a triggering excuse to adapt or change rather than as a burden, and conduct scenario analysis to be well prepared for any kind of event.

The transition from an unsustainable to a sustainable business model is where businesses can make the highest profits. During this transition, they identify and take advantage of new economies of scale and improvements of operational efficiency.

However, when a business has already incorporated sustainability criteria and deployed it, the potential for further improvements and gaining additional value is limited.

This evidence calls for a rethinking of the externalities-inclusion matter.

The question is not just that firms have to incorporate environmental and social externalities produced by their operational actions, but also how they have to do it so they can generate shared value.

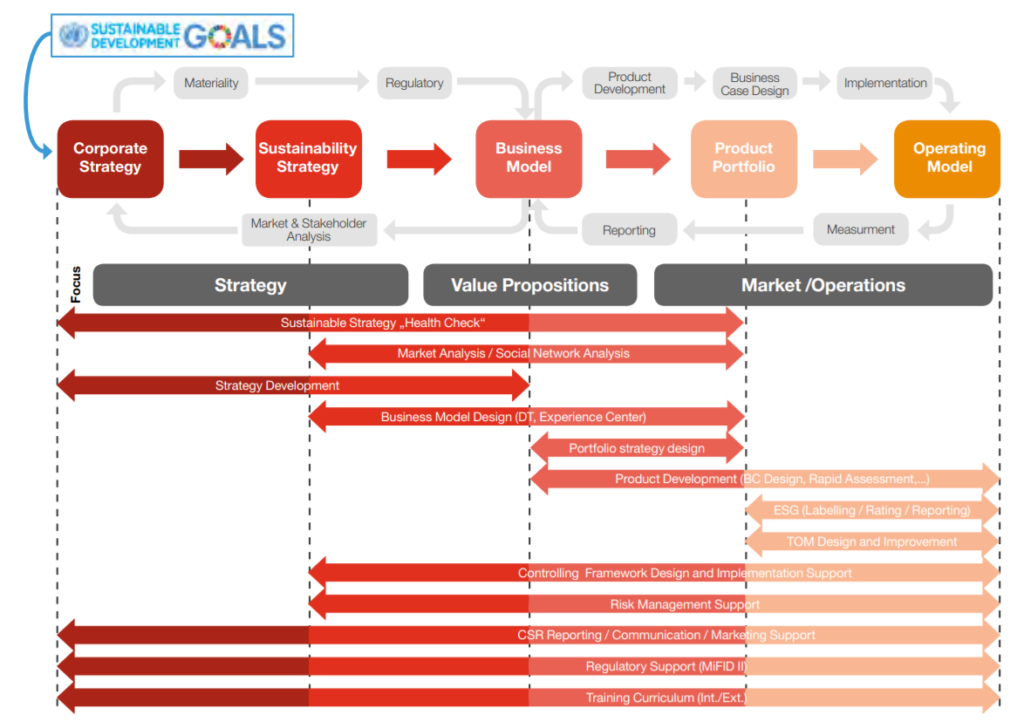

Towards a corporate sustainability strategy

Any attempt to move from a firm’s classical corporate strategy towards a corporate sustainability strategy requires a step-by-step approach. Because externalities have a material impact on business financial performance, the analysis and dissection of the corporate strategy is crucial to identifying them. The true shared-value is a result of mitigating externalities’ negative effects or material impact.

Then, both sides, the environment and society as well as business shareholders, will profit from including sustainability as part of the business strategy.

The next steps are linked to putting together a suitable business model which serves as the basis for a product portfolio of new sustainable finance products.

What we think

Jörg Ackermann, Partner at PwC Luxembourg

The mitigation of negative externalities is the first natural consequence of the transition towards more sustainable business models. However, Sustainable Finance should go one step further. Its ultimate goal should not be limited to the avoidance of harm – thus, of negative externalities – but should rather focus on the creation of a real and long-lasting positive impact by addressing environmental, social and governance issues.

Daniel Theobald, Banking Advisory Manager at PwC Luxembourg

Negative externalities represent a cost which may be more evident for third parties, but which in fact is also relevant for the organization itself when we consider a long-term perspective. If you disregard the negative impact you are having on society or on the environment, you are threatening your own business continuity.

We thank the Sustainable Finance Team that help us put together this interesting article!

Footnotes

(1) Hart, S. (1995), “A Natural Resource-Based View of the Firm”, Academy of Management Review, vol. 20(4), pp. 986-1014

(2) Karpoff, J.M., J.R. Lott Jr. and E.W. Wehrly (2005), “The Reputational Penalties for Environmental Violations: Empirical Evidence”, Journal of Law and Economics, vol. 48(2), pp. 653-675

(3) Krueger, P. (2014), “Corporate Goodness and Shareholder Wealth”, Journal of Financial Economics, vol. 115, pp.304-329; Dhaliwal, D.S., O. Z. Li, A. Tsang and Y.G. Yang (2011),”Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Re-porting”, The Accounting Review, vol. 86(1), pp. 59-100; El Ghoul, S., O. Guedhami, C. C.Y. Kwok, D.R. Mishra (2011), “Does corporate social responsibility affect the cost of capital?”, Journal of Banking and Finance, vol. 35(9), pp. 2388-2406; Chava, S. (2014), “Environmental Externalities and Cost of Capital”, Management Science, vol. 60(9), pp. 2223-2247

(4) Capelle-Blancard, G., & Petit, A. (2017). Every little helps? ESG news and stock market reaction. Journal of Business Ethics, 1-23

(5) Porter, M.E., G. Hills, M. Pfitzer, S. Patscheke, and E. Hawkins (2012), Measuring Shared Value. How to Unlock Value by Linking Social and Business Results