The 2017 tax reform becomes effective on 1 January and with it comes along a series of tax measures aimed at tackling corporate taxation. We’re looking at what the tax reform means for companies and what further measure could strengthen Luxembourg’s credibility and attractiveness.

What’s cooking for companies?

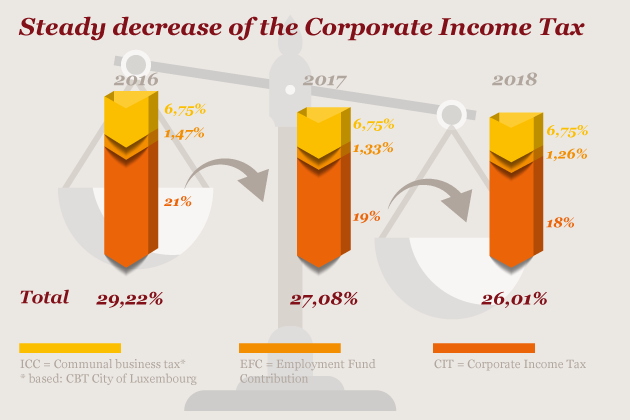

Corporate Income Tax (CIT)

In 2017, the CIT rate will go from 21% to 19%, and then to 18% in 2018. To strengthen entrepreneurship in Luxembourg and especially startups, the reform will lower the rate of the CIT from 20% to 15% for SMEs whose taxable income will be less than 25,000 euros in 2017.

While decreasing the CIT rate is undoubtedly a positive measure, it’s still not enough to maintain the attractiveness of the country and keep up with other countries. All the more so as the Government has acknowledged that the OECD BEPS Action Plan will broaden the tax base of Luxembourg-based communities.

Communal business tax (ICC)

The communal business tax (ICC) rate will not change. This means that the corporate tax rate applicable in Luxembourg City will decrease from 29.22% to 27.08% in 2017, and to 26.01% in 2018.

Net Wealth Tax

The Net Wealth Tax applicable to financial holding companies (e.g. Soparfi) will increase by 50% of the minimum amount. This practice, which has become recurrent, could seriously undermine the patience of investors and their confidence in the stability and predictability of Luxembourg taxation.

Withholding tax on interest

The withholding tax payable on interest will increase from 10% to 20% in Luxembourg in 2017.

Tax exemption for the transfer of family businesses

While the transfer itself will be tax exempt, the buildings and land belonging to the company remain a question to address. The capital gain will not be taxable as long as the business continues to exist.

In our view, for relevant results, the 2017 tax reform should have addressed three categories of measures:

Strengthening tax attractiveness by:

(i) reducing the corporate tax rate to 15%;

(ii) broadening the scope of the withholding tax exemption;

(iii) abolishing the net wealth tax;

(iv) creating an incentive for companies with significant equity capital.

2. Introducing compensatory measures To achieve significant rate reductions without putting down tax revenues as a whole, authorities should consider an equitable and balanced widening of the tax base, as well as reductions in tax credits.

3. Promoting transparency Finally, Luxembourg must comply fully and quickly with international rules to secure its reputation and credibility. Acting in a coordinated and coherent way with the measures adopted in other countries is crucial. Moreover, quickly putting in place certain aspects of the BEPS project could send a strong message of compliance and allow Luxembourg to be seen as an early adopter.

What if…

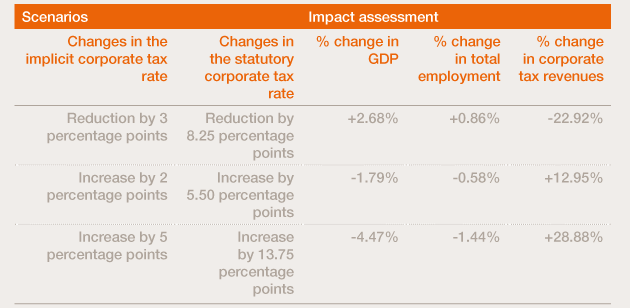

We simulated three scenarios based on the current nominal rate (29.22%) and assessed the impact on GDP, employment and tax revenues.

What we think

Wim Piot, Tax Leader

Any proposed tax reform must be beneficial to the Luxembourg economy, which is largely based on foreign and mobile capital. As a matter of fact, Luxembourg is an open financial economy highly dependent on foreign investment. The first objective of the country’s fiscal policy should therefore be to maintain and develop Luxembourg’s international position as a strategic investment location. Any proposal for tax measures should strengthen Luxembourg’s reputation as a strong economic partner, complying with international standards and governance, and strengthen its credibility as a member of the European Union and the OECD.