In the past few years, most banks have come to understand that if data is the new oil for companies, then it just might be the new gold for them. Following this, most banks also realise that it will take Artificial Intelligence (AI) to unlock that data gold. Sounds pretty straightforward, right?

In this blog we are going to talk about the 1, 2, 3 of unlocking that banking data for intelligent use. In fact we could, if we wanted to, extend our criteria to include most companies but we will focus mostly on banks here.

What we are suggesting is an oversimplification. Of this, we are aware, so please give us some poetic license as we need to focus on a theme to keep these blogs from turning into tomes. Nevertheless, we have noticed three clear trends emerging in the last few years. They are: 1), pretty much every financial institution (and company) is interested in some form of AI to unlock data, but… 2), most don’t know what to do with it, and… 3) even if they did, there is a problem finding the talent that knows how to use it.

When it comes to data banking, please don’t say “the new normal”!

We hear a lot about the new normal. (sorry, we said it). And we can’t lie, here on our blog team, we despise that phrase. But darn it, sometimes it’s the right one.

Let’s take banks for example. They’ve been around for a long time and are an integral part of our individual and collective lives. We trust them, and because we have done so for years and years, that trust is tied up in the notion of their longevity and stability. So using a bank is normal. Banks are nothing new. But consumer behaviours have changed, digitalisation arrived, and stricter compliance has come along with a sea change of regulations. Banks are the same animals, but are being forced to change their spots. This is very true when it comes to Artificial Intelligence (AI).

Over time, it was normal for banks to amass huge amounts of data – financial, behavioural, transactional, statistical etc. What’s new is the way that banks now understand they have the ability with data analytics and artificial intelligence (AI) techniques to unlock that data, and put it to intelligent use to make data driven-decisions to grow their business, create a smarter and more efficient organisation, manage risk and regulatory compliance, help with fraud detection, and reduce operations risks and costs (and a host of other purposes).

Luxembourg is data driven and getting more so!

In the broader PwC survey, we clearly see evidence that pretty much every company – including financial institutions – is incorporating advanced analytics tools and data expertise into their day-to-day business, to increase knowledge on customers, foster innovation, and optimise their processes. Luxembourg is well positioned on a global level, when it comes to the adoption of AI tools and moving from spreadsheets to tailored data solutions. The use of AI tools has already doubled since 2019 and is bound to grow further in the future. Indeed, according to the Government’s AI Readiness Index 2020 (Oxford Insights), Luxembourg is ranked in the 15th position (out of 172 countries) and in the 9th position if we look at Western European countries only. Besides, the Responsible AI Sub-Index indicates that Luxembourg is highly competitive, achieving a third rank.

Luxembourg has attracted the 4th highest investment per capita in AI as reported by the Financial Times in 2019. These investments have already started to show their effects as we can see through the findings of the survey. Companies in Luxembourg find it easy to create Proofs of Concepts (PoCs) to test new concepts and possibilities in Data and AI and at the same time are dedicating a significant share of their turnover into the development of AI. Although there are new challenges such as lack of talent and visibility on return of this investment, AI initiatives are well resourced in Luxembourg.

The use of AI in the risk and finance functions of Luxembourg banks

Financial institutions both global and local have realised that it is essential that they learn how to reap greater benefits from their data and to leverage artificial intelligence, process automation and advanced analytics techniques to increase their capabilities and to rationalise their operations. As early as 2018, a global PwC study on Data and Analytics in Financial Institutionsconcluded that, “Financial institutions will look for success by combining business domain, analytics, and artificial intelligence (AI) experts who understand algorithms and new techniques, as well as data engineers/scientists who can work with cloud technology and machine learning systems.”

So we can agree, pretty much every bank (and company) is interested in AI. But we also see that few companies and financial institutions really know what to do with it. There are a number of questions that many of them still don’t have the answers to:

What are the specific use cases that I can actually profit from?

How do I actually make that happen?

What is my immediate tangible benefit ?

How would I go about achieving that?

To get those questions answered takes specialised expertise. As our broader survey also revealed, functional specialisation in Luxembourg companies and banks indicates a better understanding of data and maturity. Increased specialisation in the data domain is also becoming apparent, with growing roles in data architecture, data management, and data governance. Instead of single data scientists, more commonly whole teams are present. However, talent remains a main concern, with most companies reporting difficulties in finding the most quality candidates in a scarce talent pool. To complicate matters even more, and as is so often the case in anything technology related, it is even harder to find resources that understand not only the data/AI aspects, but also the business needs.

A slice of Luxembourg

To start with, and to gauge the current state of the use of artificial intelligence in Luxembourg, PwC conducted a survey, specifically within the Luxembourg banking sector.

As expected, in the survey, The use of AI in the risk and finance functions of Luxembourg banks, the results show that there is significant interest in the market for integrating artificial intelligence (AI) and process automation into day-to-day risk and finance operations. But where there is concern is that, at the same time, a majority of banks surveyed stated that they do not currently use AI or that their use of AI is still in its infancy.

The polled banks also indicated that the major impediments to the use of AI they are facing are insufficient data quality, lack of qualified staff, and restrictions arising from their own internal governance and IT.

Use of Data Analytics and Artificial Intelligence 2021 in the banking sector

The key results of PwC Luxembourg’s survey indicate that while there is a large interest in AI for risk and finance, there is a lagging adoption and often weak data governance.

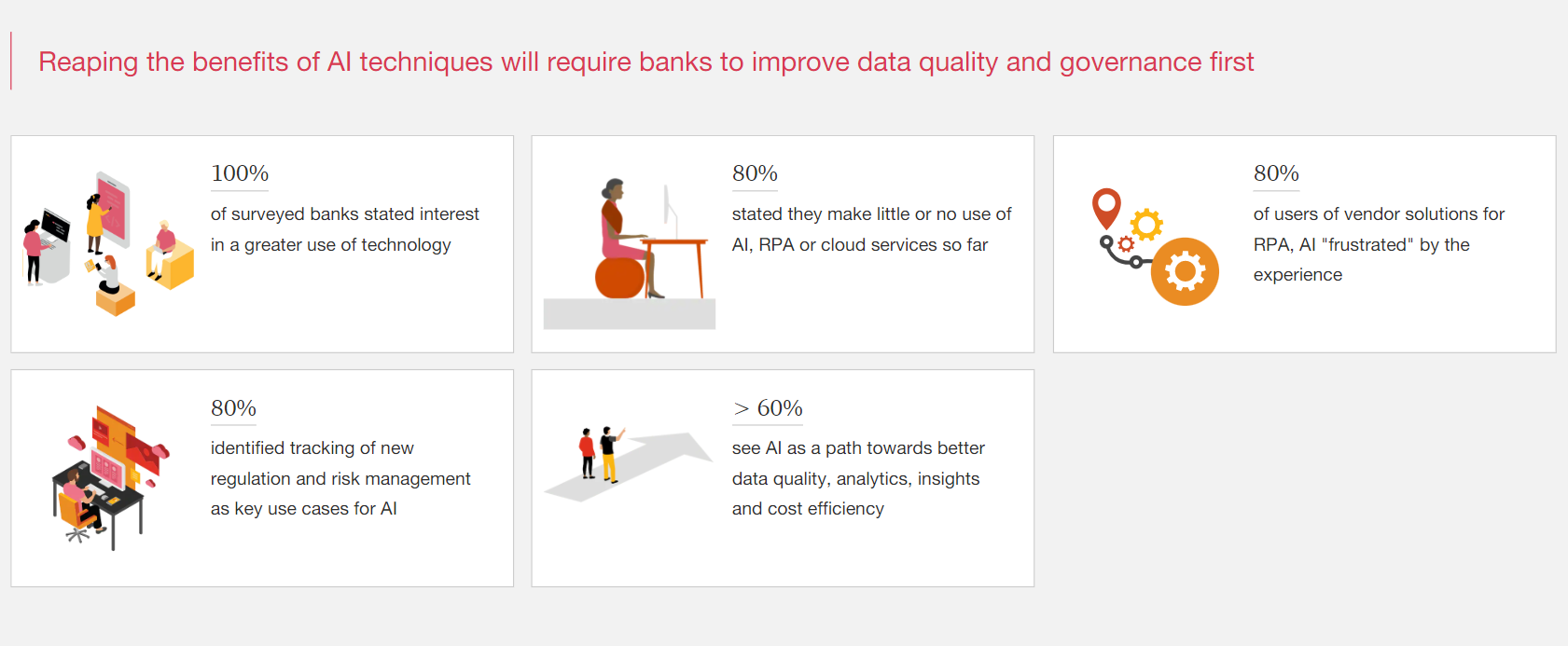

Reaping the benefits of AI techniques will require banks to improve data quality and governance first.

100% of surveyed banks stated interest in a greater use of technology

80% stated they make little or no use of AI, RPA or cloud services so far

80% of users of vendor solutions for RPA, AI “frustrated” by the experience

80% identified tracking of new regulation and risk management as key use cases for AI

> 60% see AI as a path towards better data quality, analytics, insights and cost efficiency

The results of this and the broader survey demonstrate the relatively large disconnect we see in many companies between the interest they have in the topic of AI and the fact they have little tangible idea what to do with it, or how.

This is not to say that there are no companies in the world currently making excellent use of data and analytics, there are—we have the Amazons, the Ubers, the Netflixes of this world. There is also a growing list of fintechs that, as this article puts it, are “crushing data-driven innovation”.

But most larger financial institutions, globally and in Luxembourg, are still at a low level of maturity when it comes to using AI and achieving excellence in data analytics on clear-cut business objectives.

In order to move ahead with advanced analytics, banks need good quality data or they cannot get results. In computer science there is a saying— garbage in, garbage out (GIGO)— which is the concept that flawed, or nonsense (garbage) input data produces nonsense output. To be anywhere close to using AI or any of these complex analytical or learning tools that financial institutions have available to them, they need to get the basics right.

In PwC’s 22nd Annual Global CEO Survey, over 80% of Luxembourg’s CEOs stated they believe that AI will significantly change the way they do business. Yet they also listed two of their biggest challenges arising from Data and AI, where, despite the progress made in this area, there is still a significant gap in the information available to decision makers. Just 29% of respondents view the data available to them as adequate.

Obtaining this solid foundation is something that banks have missed for multiple reasons.

Large banks are complex. They are often international, have various entities, various subsidiaries and legacy systems and processes that are holding them back. They have different types of data, or data that is siloed or different ways of using that data making it difficult to aggregate across those divisions.

Often when you compare them to customer-centric and agile fintechs and startups traditional banking institutions are lagging. When specifically talking about big data, the situation can be even worse with legacy and outdated systems not able to cope up with the growing workload. Huge amounts of data when collected and stored using outdated infrastructure can put the stability of the entire system at risk.

Finding an answer to the talent war for data banking

The number 3 question when unlocking banking data for intelligent use is, Who will do it? This transverses finance and is a growing problem in Luxembourg and beyond as the war for talent heats up.

AI is a key driver of innovation in Luxembourg, across all sectors. But companies are competing for talents, with significant investments focussing on data specialists, enabling a more widespread operational use of AI.

According to our earlier blog there are two underlying reasons. One is more structural, namely, it’s linked to the lack of training or a scarce training offering in both market and Academia. As a result, there is a limited availability of graduates and experts in fields relevant to AI although it’s increasing. To this, one needs to consider that, in general, the knowledge of AI among executives still falls short.

The second reason is the increasing number of competencies that Data and AI professionals have to respond to. This has to do with the way AI solutions best work, fusing themselves with analytics, the Internet of Things (IoT) and other enterprise systems. This requires, clearly, specialised roles, resources and processes to keep all technologies integrated and properly running.

This is a growing challenge.

Demand for Artificial Intelligent (AI), and Machine Learning (ML) in particular, has grown in recent years as the financial services sector undergoes a period of digital transformation. COVID-19 only serves to accelerate this transformation but in the world of finance there is a hydra of complexities that also need to be taken into consideration.

For example, as pointed out in this blog by our colleagues in the UK, Artificial Intelligence in financial services: An evolving regulatory focus, the use of AI brings with it a number of unique regulatory, and indeed ethical, challenges. “What’s the right level of explainability for decisions supported by AI and ML? Is there a higher bar for decisions which impact consumers? How much understanding should a firm’s board have on the tools being deployed? How can accountability be ensured and bias mitigated? Many firms are grappling with these challenges and looking for guidance from policymakers.”

In PwC’s 22nd Annual Global Ceo Survey, CEOs globally and locally confirmed they are confronted with a need for higher skills, but have an increasingly hard time finding that talent.

And it is increasingly difficult for Luxembourg to find the talent as is clearly evident in a spate of articles and PwC’s own challenge in finding talent, one of the key messages of the PwC Luxembourg 2021 Annual Review, specialised profiles being the most difficult. And you see this in both the broader survey as well as the smaller survey. How do we attract the right talent? This is a bigger phenomenon than just local.

Concluding reflection on data banking

The increased regulatory focus on AI suggests the pressure on firms to get these decisions right will only increase. This means that as firms embark on adoption of AI they need to factor these considerations in, even as the regulatory framework is developing. Firms need the right capabilities to identify, manage and mitigate the unique risks that AI poses, for example in model risk management. The current regulatory focus on AI is likely to result in more guidance but firms will still need to carefully judge the ethical and reputational implications of the use of these exciting tools and ensure they are meeting the outcomes the regulators expect to see delivered.

It seems quite irrefutable that there is room for growth for AI in Luxembourg. Still, a large number of companies do not fully leverage the new technologies and risk falling behind the competition, citing a lack of clarity about the return on investment and the lack of talented people as main reasons for this. If only it was as easy as 1,2,3.

To thrive, banks understand they need to adopt AI technologies to come up with new value propositions and deliver unique customer experiences. But in order to mine the new gold, they need first to clearly consider what their objective is, how they are going to achieve it and ensure they have the right talent that can carry their intentions to success.