In our previous article, we delved into the effect of real estate supply and demand—side catalysts on Luxembourg’s dynamic prices—primarily focusing on the impact of relative supply scarcity compared to surging demand on lowering the risk of overvaluation.

In this article, we aim to take a brief look at recent changes in the Grand Duchy’s real estate prices in order to validate the conclusions drawn in the previous article. We then shift our focus to the formulation of some key supply measures that we believe will prove instrumental in allowing Luxembourg’s Real Estate ecosystem to address (and adapt to) radical changes in individuals’ sustainability preferences.

Recent housing prices dynamics in Luxembourg

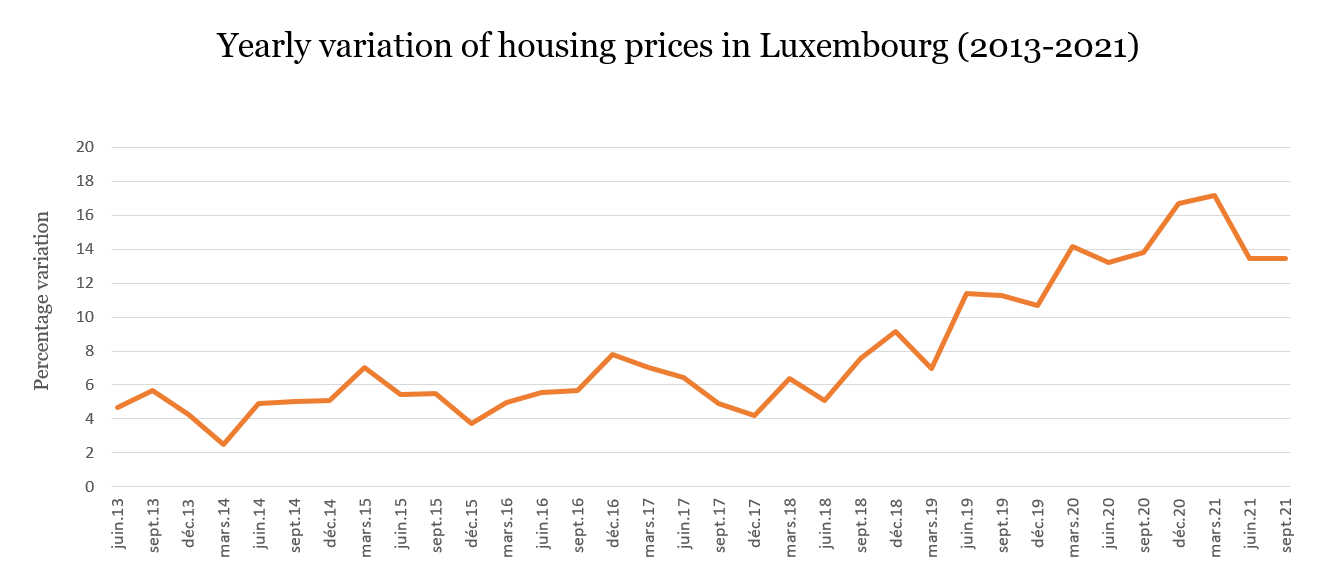

Housing prices in Luxembourg have undergone an unabated rise over the years, rising by over 10% annually since 2019.

Although Statec predicted a deceleration for 2021*, this increase has shown no signs of slowing, with prices surging 13.4% from Q3 2020 to Q3 2021 alone (See Exhibit 1). However, recent inflationary pressures may soon bring a shift in Luxembourg’s real estate market.

Indeed, while the low interest rate environment has long augmented the borrowing capacity of households** rising inflation may see policymakers increasing interest rates, tightening borrowing conditions and potentially curbing mortgage demand.

That being said, the effect of rising inflation on housing demand remains to be seen. First, the materialisation (and extent of) reactionary monetary policy changes remain, as of yet, uncertain, as the evolution of the communications of the major central banks shows.

Further, Luxembourg’s economy is proliferating strongly – with GDP expected to have rebounded by 7% in 2021 and being forecast to rise a further 5% in 2022. Employment has also been very resilient, with the unemployment rate declining to 5.8% in 2021.

To summarise, should rising interest rates generate a slowdown in housing demand, putting downward pressure on prices, these will likely be offset by the country’s solid economic performance.

Exhibit 1. Yearly variation of housing prices in Luxembourg 2013-2021 (Click to enlarge)

Source: Statec

(*) Note de Conjoncture STATEC June 2021; (**) As of December 2021, the interest rates applicable to new mortgages stand at 1.58 %

The case of sustainable real estate

As demographic and economic trends largely dictate demand shifts, there is little potential for action.

Supply increases represent the most compelling solution, easing pricing pressure and increasing housing affordability for workers and employers alike. Additionally, increasing housing supply (especially in the capital) would further serve to alleviate Luxembourg’s congestion issues, which hinder the country’s environmental objectives.

However, increasing supply is easier said than done and often requires a multifaceted approach that takes into account one major paradigm change: meeting the burgeoning demand for sustainable developments/builds.

Sustainability is quickly emerging as a top concern among society and its stakeholders, urging a paradigm ESG (Environment, Social and Governance) shift in Europe’s financial and regulatory landscape.

Given the tangible nature of the built environment, and the fact that real estate alone accounts for 40% of global energy consumption and almost one third carbon emissions, it is no surprise that the industry is impacted by (and reacting to) the wide-scale prioritisation of sustainability and the actions needed to secure a prosperous and equitable future.

In addition, the pandemic has served to further reinforce sustainability concerns; leading current and prospective buyers increasingly valuing high quality, sustainable indoor and outdoor spaces.

Nevertheless, embedding ESG into Real Estate shouldn’t solely be discussed in the context of addressing sustainability risks. There are, in fact, tremendous value creation opportunities that stand to be unlocked from the effective consideration and implementation of sustainability criteria when developing, constructing and maintaining real estate projects.

Namely, in the real estate landscape of tomorrow, the developers that opt for ESG-enhanced projects will likely benefit from increased access to financing.

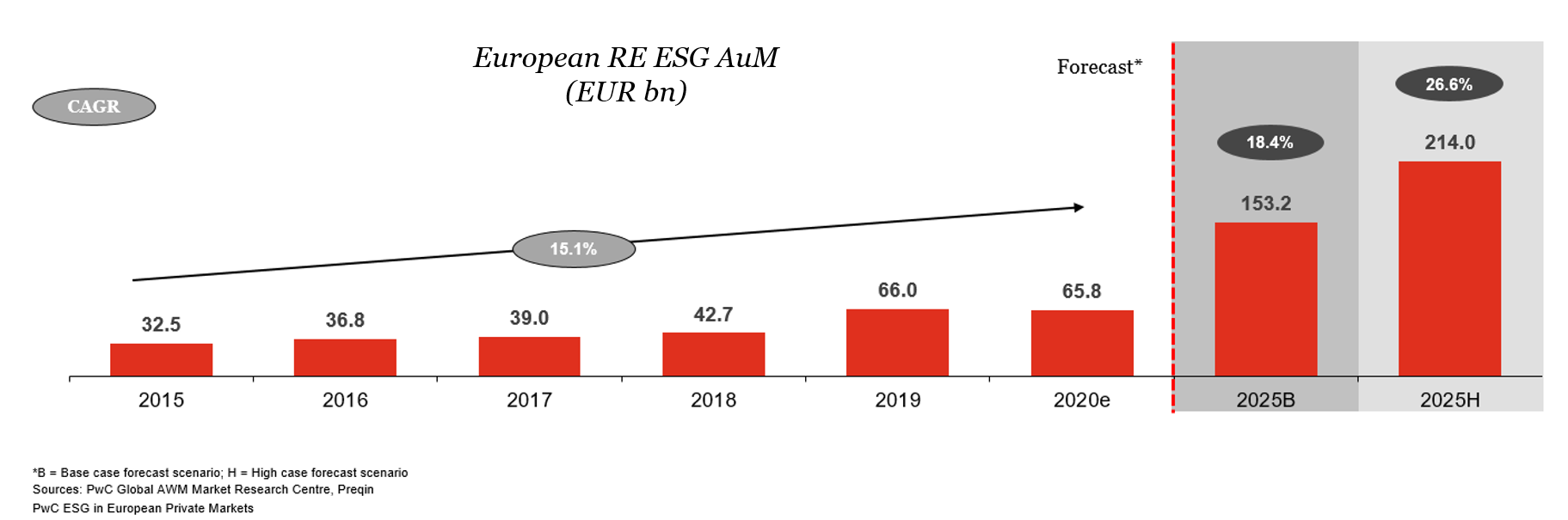

Surging investor appetite for ESG-aligned investments has seen ESG assets in the European Real Estate Private Markets more than double since 2015, reaching EUR 65.8bn in 2020.

In light of this—and the fact that we expect ESG assets to account for 33.7% of Europe’s total Real Estate AuM by 2025—it follows that sustainable housing will see an ever-increasing share of investment capital moving forward.

Exhibit 2. European Real Estate ESG AuM (Click to enlarge)

Unlocking the sustainable real estate opportunity

In order to unlock this opportunity, industry and government actors need to continue re-strategising, adapting the existing and prospective housing supply in accordance with ESG considerations.

These new requirements may be onerous, but will prove absolutely essential in not only protecting, but actively enhancing Luxembourg’s value proposition as a place to live and work.

Marrying real estate and sustainability will require heightened collaboration between developers, architects, and public authorities in Luxembourg to ensure that housing develops in parallel with mobility infrastructure, green areas, electricity power stations, and include an impact assessment on the soil and the risk of natural disasters generated by the development of residential areas.

Banks also have a role to play, and an opportunity to seize, in catalysing the transition towards a sustainable real estate landscape in the Grand Duchy.

With the upcoming climate stress tests, banks will need to assess their mortgages’ exposures to climate risks. This further incentivises banks to closely monitor the value and risks associated with their real estate loan portfolio, scrutinising its characteristics such as energy efficiency or location. This would ultimately benefit them through enhanced resiliency.

In addition, banks (particularly public ones) have a role in supporting the financing of social housing, be it for rental or acquisition purposes. Again, public authorities have a coordination role to play, ensuring that good governance rules are applied at all levels of decision and planning.

These structural changes should be complemented with small and direct actionable steps: the first step being improving the dialogue among the various stakeholders to shorten the time spent to obtain building permits and related administrative authorizations.

It is a widely held view within the real estate realm that procedural delays represent a major hindrance whose circumvention will require a coordinated effort between all parties, from the initial land acquisition to the completed dwellings.

A study by the Observatoire de l’habitat highlights that the current supply shortage in Luxembourg is not a land availability issue, as current available land meant for housing could generate housing for 300,000 additional people. Rather, the issue likely arises from a lack of incentives for landowners to sell or develop on their land. Should the above-mentioned procedural hindrances be addressed, however, this could see this barrier being removed altogether.

To conclude, RE players are expected to assume an even greater role in the ESG landscape as tenant demand for high-quality, sustainable properties surges in the post-pandemic landscape, and as policymakers increasingly recognise the built environment’s role in the transition towards a low-carbon economy.

What we think

Christelle Sapata, Manager at Market Research Center, PwC Luxembourg

A sustainability driven approach to real estate would represent a huge opportunity to support the long-term value of real estate in Luxembourg.

…………………………………………

Amaury Evrard, Partner, Real Estate & Infrastructure leader at PwC Luxembourg