Raising this type of question is of growing importance. The last few years have seen a growing public interest in the role business plays in society, and that will only grow in the future. The fact that ESG is reshaping the European Private markets landscape, with all of the industry’s stakeholders attributing an unprecedented degree of importance to sustainability considerations, is a tangible example.

Certainly, one cannot overlook the rate and scale with which the ESG shift is redefining Europe’s Private Markets (PM) landscape. In a recent study, PwC Global AWM Market Research Centre forecasted Europe-domiciled ESG PM assets to reach between EUR 775.7bn and EUR 1.2tn by 2025, making up between 27.2% and 42.4% of European Private Market assets, up from 14.8% as of end 2020.

Don’t have time to read the whole blog entry? Then watch our “Blog in 1 minute” video for a quick summary of its main points:

However, all PM’s asset classes don’t seem to have the same level of ESG adoption. In this article we focus on how the ESG performance of Private equity (PE), including both GP (General Partners) and their investors (Limited Partners or LP), is seen by consumers and the public opinion. The analysis is based on online content and engagement that we fetched from public web sources.

Arguably, one of the most distinguishable features of PE is how influential this asset class’s players are over their portfolio companies.They are, then, in a unique privileged position to drive the ESG transition in an industry that lags behind other PM players.

More specifically, this article shows consumer sentiment regarding EU and US private equity firms’ ESG performance, encompassing aspects such as share of voice, ESG sentiment and ESG’s subtopics relevance.

The data we used correspond to the period August 2020-August 2021. Both historical and real-time data can provide accurate market and consumer sentiment information, assess brand valuation and, in this particular case, understand and benchmark GPs’ sustainability and ESG reputation as well as that of their competitors and underlying investors.

How we did the case study

Taking advantage of a service we put together some years ago called Digital Intelligence, we analysed public web sources such as online news and magazines, discussion forums, Q&A sites, blogs, and, a staple in this list, social media posts.

But for the analysis, naturally, we defined a set of key variables that allowed us to reach the results we mentioned in the introduction. Here they are:

Share of voice: this metric gives an overview of which brand is receiving the most ESG attention online. With it, we benchmarked ESG-related conversations against other general discussions on the organisation.

Mentions: this is the total number of results (articles, social media posts, etc.) with one or more keywords of the query featured at least once in the text.

Sentiment: this is the opinion or feeling expressed within the result(s). It can be positive, neutral or negative. It’s determined via machine learning based on the semantics and intensity of the words and emojis used.

You might be wondering how we actually measure them. Well, based on queries we create that contain keywords and phrases, our Digital Platform crawls the internet to find answers. But does it make this trip alone?

In fact, it’s exactly the opposite. It’s well accompanied by new technologies such as NLP (natural language processing), ML (machine learning) and AI (Artificial Intelligence).

With the help of these technologies, we quantify the variables and, as a result, we can assess and rank the brands or organisations we are researching.

Let’s explore our findings.

Want to know more?

Brand metrics scores are calculated using various different social listening KPIs with different weightings to accurately reflect both quantity and quality of the results. This methodology reduces potential false effects from bots, spam accounts, paid likes, etc.

For instance, some of them are audience engagement (retweets, likes, replies), sentiment, content created (volume), potential reach and network scope, and market influencers.

Private Equity’s take on ESG

Needless to mention, the need for GPs to hold an accurate and ongoing view of how investors and the broader market perceive them with respect to ESG and sustainability-related matters is only growing.

However, among all the private markets’ asset classes, Private Equity, despite having grown at a CAGR of 17.8% from 2015 to reach EUR 98.3% in 2020, is lagging behind its public and portfolio management equivalents in terms of ESG uptake, with only 10.7% of European PE assets being allocated towards ESG funds as of end 2020. (Source: MRC)

LPs are becoming increasingly cognisant of ESG’s role as an effective lever for value creation and risk mitigation. The risk management dimension, in particular, has risen in prominence – with LPs increasingly observing that ESG considerations have an actual material impact on the future value of their portfolios as well as the “external” corporate image driving shareholder value more broadly.

According to PwC Global AWM Market Research Centre, LP’s Top 3 main drivers to invest in ESG are risk management (41%), corporate values (41%) and risk-adjusted returns (35%)

This drawback can be attributed to the lasting perception that the PE market players’ focus on the profitability of potential investments, isn’t congruent or even incompatible with ESG. And the wrong idea that ESG produces negative effects on performance have further served to reinforce this perception.

The presence of small-scale boutique-like players in the PE industry (be it portfolio companies or the PE firms themselves) has also served to hinder a further ESG uptake, as these players traditionally lack the appetite and ability to absorb the high(er) costs necessary to integrate ESG within their investment or economic activities.

What our data-driven analysis told us about ESG performance and Private Equity

We have organised this part twofold: the first one helps us to understand how consumers perceive PE’s performance related to ESG. To do that, we studied which pillar of ESG is more discussed or drives more consumer attention, the ESG matters (or subtopics) PEs address or share content online and we determined the Net Sentiment Score. The latter is the result of subtracting the percentage of negative online brand-related mentions from the percentage of positive online brand-related mentions associated with ESG.

In the ESG acronym, which echo is stronger?

The environment, the societal aspect, governance… is there any component that echoes louder in the ESG acronym?

That’s a room-for-debate question and it’s highly subjective, however, as other organisations, PE players are influenced by the context around them, clients’ drivers and any other regulatory development that forces them to prioritise one or more of the components.

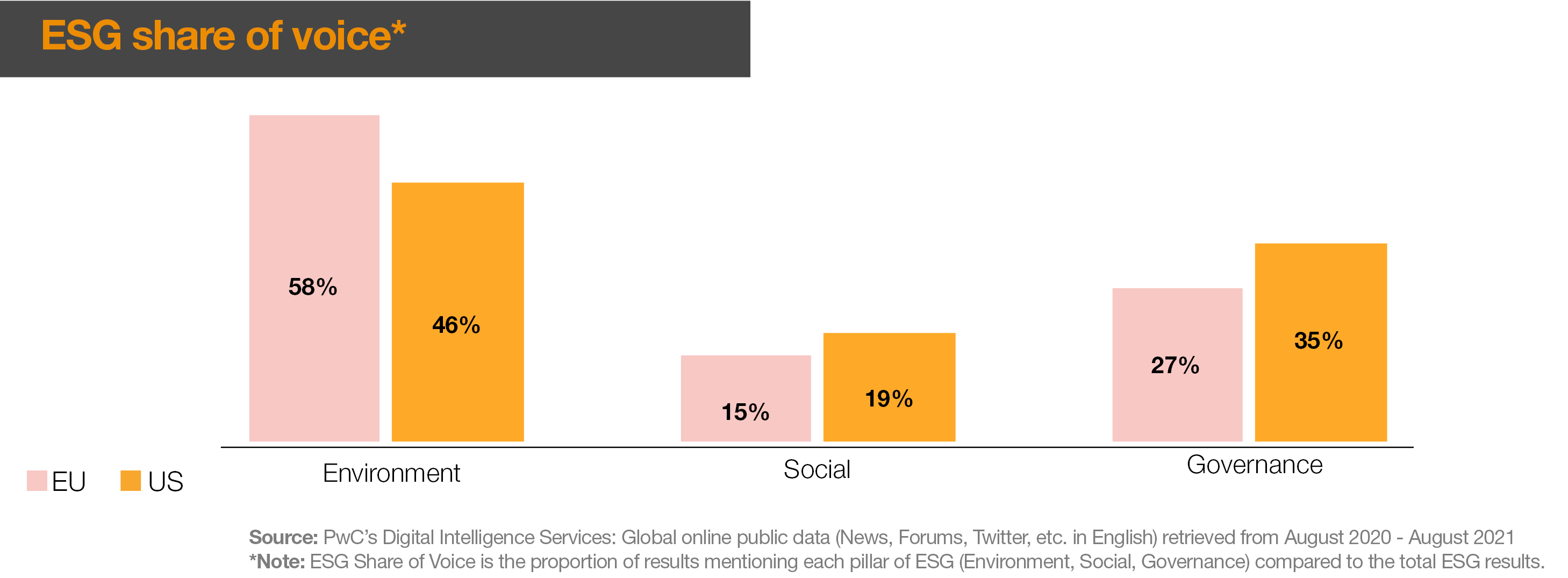

See Exhibit 1, which shows how the E seems to be more discussed at consumer level with regards to how EU-based and US-based PEs are taking action on the different ESG pillars.

In this case, EU-based PEs (58%) are several percentage points ahead of their US-based peers (46%). The fact that the EU has one of the world’s most advanced environmental sets of standards and the 2021’s European Green Deal—in which the 27 countries of the bloc have pledged to reduce emissions by at least 55% by 2030 compared to 1990 levels—could be a triggering factor for the current E preponderance.

Exhibit 1: ESG Share of voice (click to enlarge)

Nevertheless, let’s agree on one fact: adopting ESG is more than ticking the right ESG boxes, but to grasp the real opportunities. The E preponderance could change soon or last longer depending on the socio-political context.

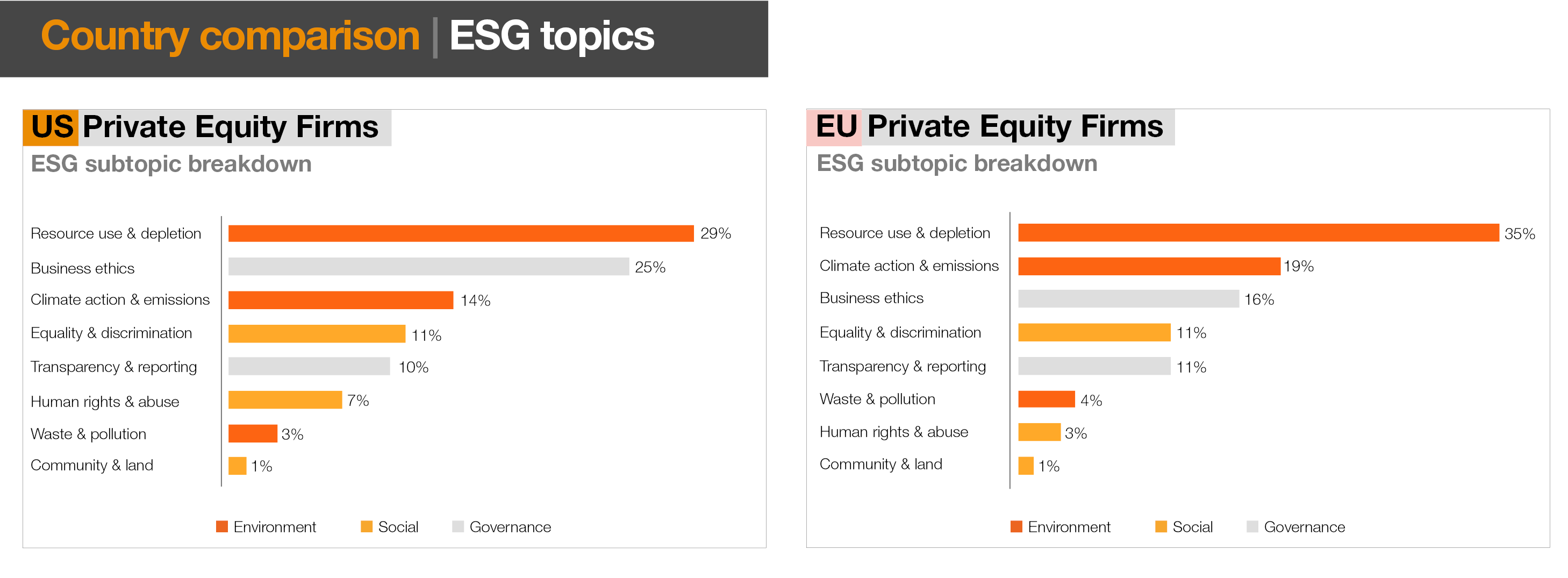

The most discussed ESG-related matters for Private Equity firms

Digging more deeply into the ESG subtopics, environmental-related matters logically rank higher. In both cases, resource use and depletion is the most discussed. But while in the EU the climate actions matter occupies the second position, it’s business ethics that comes second in the US podium.

According to the 2021 Global Business Ethics Survey, ~1 in 5 U.S. employees were in workplaces with a strong ethical culture in 2020 compared with 1 in 10 in 2000. Ethical Culture Strength, the survey states, remains high. However, in the U.S. and globally, ~8 in 10 employees reported misconduct also in the same year. Business ethics seems to generate much attention and COVID-19 might have only propelled that.

In both locations, transparency and reporting only occupies the fifth position.

Exhibit 2. Country comparison, ESG topics (click image to enlarge)

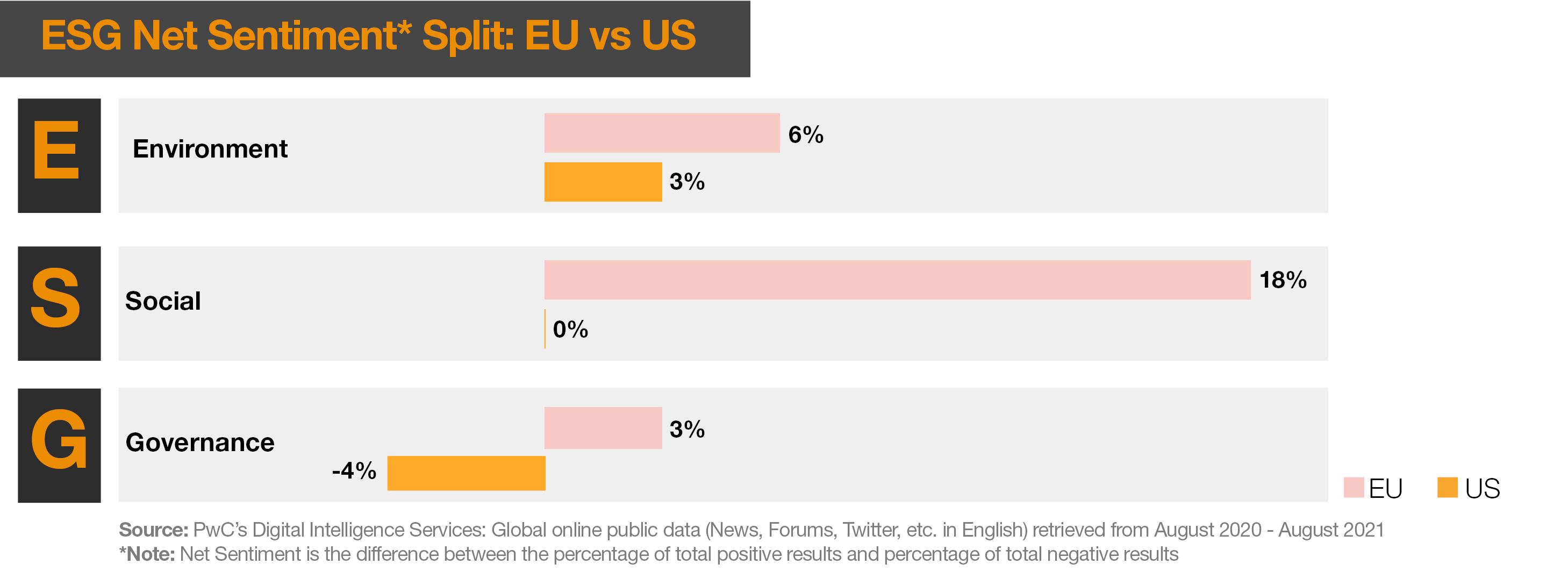

Exhibit 3. ESG Net Sentiment Split: EU vs US (Click image to enlarge)

Governance is the only pillar whose net sentiment score is negative, which can be interpreted as consumers being unsatisfied with the way PEs are addressing the pillar. This calls for the latter to take a closer look at why governance is being negatively perceived and if it’s misleading communication or the lack of it influencing the sentiment.

Close-up view to the US-based Private Equity firms and ESG performance

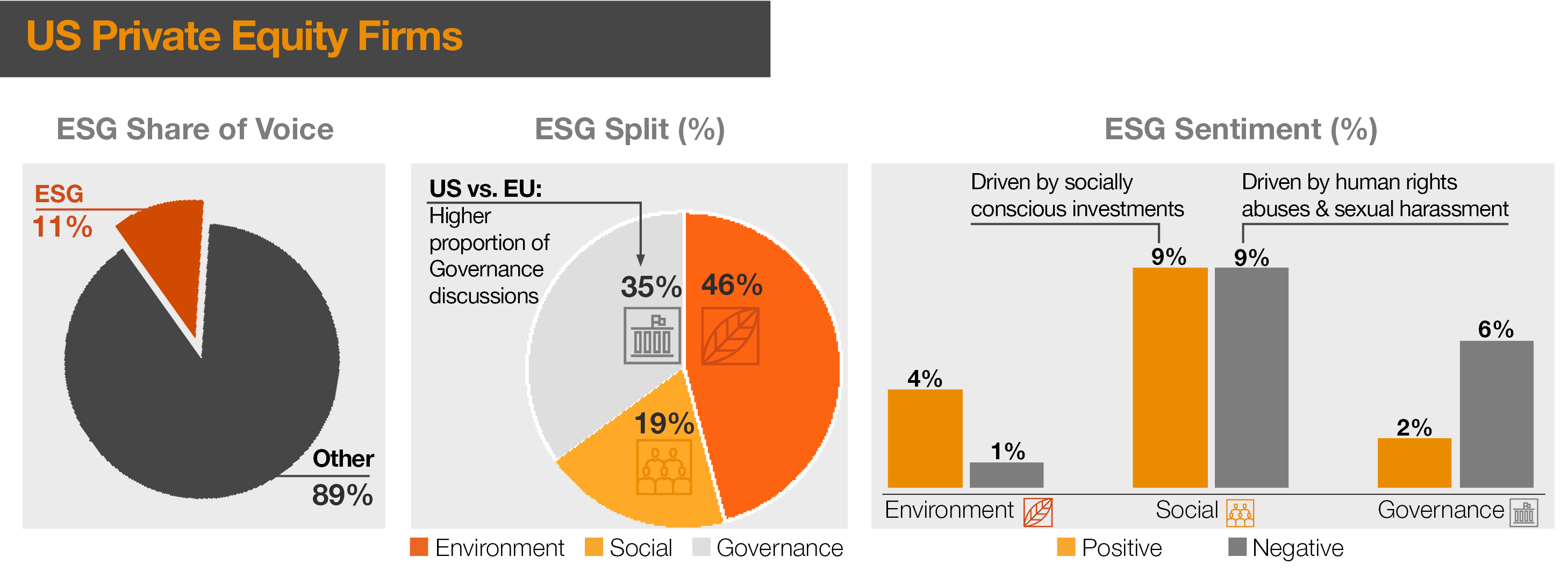

The US Case

ESG’s slice of the total conversations that US consumers carry out is 11%.

Positive sentiment around the social pillar is strongly linked to conscious investments. On the opposite site of the coin, negative sentiment is driven by conversations around human right abuse and sexual harassment

Only the pillar Governance has a negative net sentiment score (-4%)

In the US, consumers seem to pay more attention to ethical and criminal factors.

Exhibit 4. US Private Equity Firms (Click image to enlarge)

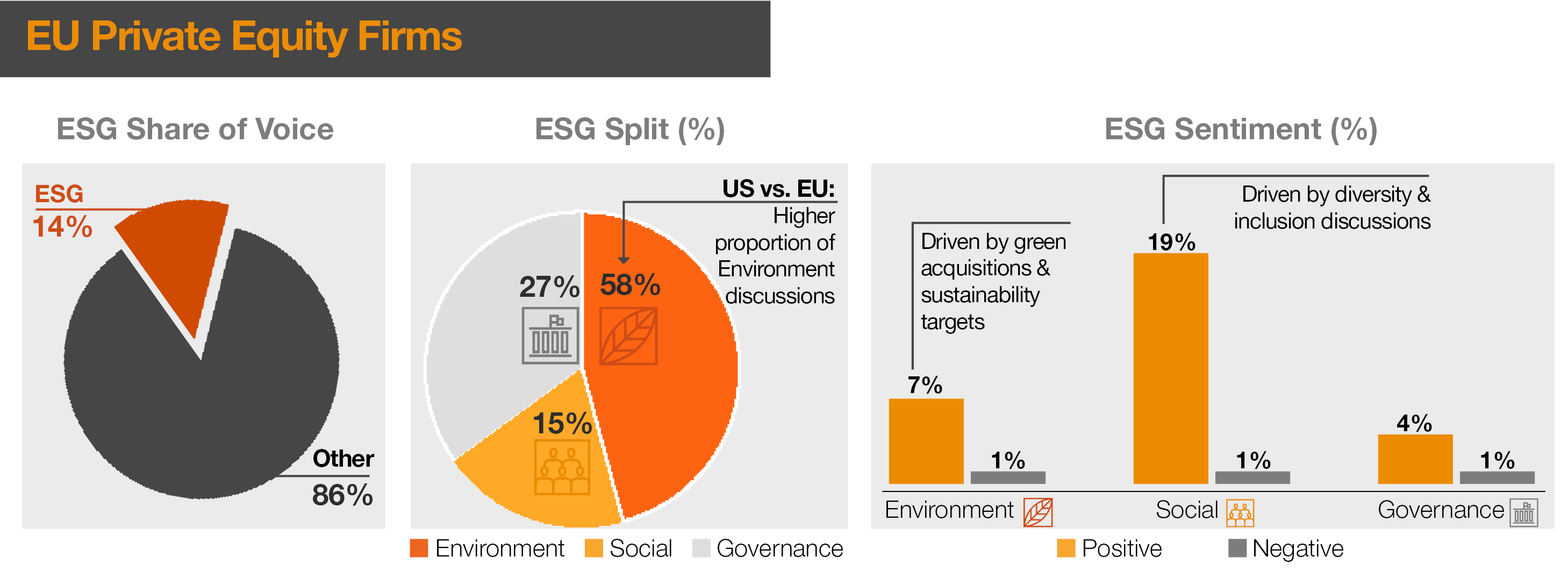

The EU Case

ESG’s slice of the total conversations that US consumers carry out is 11%.

Positive sentiment linked to the environmental pillar is related to green acquisitions and sustainability targets.

Positive sentiment linked to the social pillar is driven by diversity and inclusion discussions.

In the EU, consumers seem to pay more attention to energy and climate factors.

Exhibit 5. EU Private Equity Firms (Click image to enlarge)

Here are three takeaways when comparing these two charts:

ESG is discussed slightly more in the EU than in the US (14% vs 11% respectively)

Both US & EU private equity firms trigger most discussions around environment (US 46%, EU 58%)

Conversations around both the social and governance pillars for US PE firms outperform the EU competitors.

(It is important to note that the US mention sample size is 17 times larger than the EU mentions)

Final thoughts

This type of data-based exercises can ensure PE firms’ ongoing alignment with societal expectations and demands, facilitating the construction of a successful digital strategy and the process of taking a new product to the market. It also helps to construct custom-build indices to support performance assessments periodically.

Also, used as a management tool, this tracking market sentiment exercise can help PE firms assess how they’re making progress on executing their ESG strategy and how it resonates with wider market stakeholders.

ESG and, more broadly sustainability matters are far from being just window dressing. That’s everything but a bad sign because our Planet needs us all, with different stakeholders working in tandem. And investment companies, regardless of their type, have a role to play.

However, when building the reputations of organisations as socially and environmentally responsible, there are real risks at play because clients and overall consumers are taking a clear (and strong) stand on sustainability and advocating for it. They are more and more concerned and vocal.

Embracing ESG is challenging. It calls for both a mindset change in business but also resources, legal frameworks and governmental support. The good news is that ESG also brings opportunities to be seized.

Benedikt Jonas, Digital Intelligence Director at PwC Luxembourg

Getting an outside-in perspective on ESG-related reputation helps PE firms identify material risks stemming from the public opinion and public sentiment. This can also help them to guide investors’ ESG strategy and subsequent actions. On the other hand, identifying positive ESG market signals will help investors unlock new investment opportunities.

Kai Braun, Partner, Alternatives Advisory Leader at PwC Luxembourg

Measuring ESG performance with data analytics is a great way to start truly operationalising the sustainability agenda beyond the pure regulatory framework which most PE houses are currently in the process of implementing.