Have you heard about the growing focus of the Luxembourg tax authorities (LTAs) on the value added tax (VAT) and transfer pricing (TP) positions of Luxembourg’s taxpayers?

In fact, the global trend is for tax authorities to require more and more information about the local and cross-border intragroup transactions to analyse them for tax purposes. To do so, and similar to the close cooperation of tax experts specialised in different areas of taxes, certain authorities intend to—or already— enhance their common interactions in this area.

Don’t have time to read the whole blog entry? Then watch our “Blog in 1 minute” video for a quick summary of its main points:

To facilitate this, an amendment to the law about the inter-administrative cooperation of the authorities (19 December 2008) was submitted on 17 August 2021. Even if the draft bill #7872 hasn’t been voted on yet, we can assume the VAT authorities are looking forward to implementing it for one simple reason: they’ve mentioned it in their 2021 annual report as one of the most significant events of the year.

As a result, there could be an increase in the number of cross-tax audits in Luxembourg over the coming years. This probably raises several questions in your mind: what could be the cross implications of VAT and TP in the case of a tax audit? What are the possibilities for the LTAs to cooperate with each other? What do I need to know in terms of managing a tax audit?

Don’t sweat, we’ve got you covered. In this blog, we go through these questions to make sure you are ready to brace the possible changes. But first, we revisit some essential VAT and TP concepts and how the two are —sometimes apparently— connected.

A refresh on VAT and TP concepts

Let’s start with a refresh on Transfer Pricing. In the case of independent parties, each party acts as a separate and independent business while determining the significant terms and conditions of the transactions they are entering into, including the price.

As such, the price applied is commonly considered to be arm’s length for tax purposes, as it should reflect the market conditions and the endeavours of each party to represent its own best interests.

Intra-group transactions can be a different story though. When looking at transactions between companies belonging to the same group, the interests of the group may prevail over those of the stand-alone companies. This may result in different prices in intra-group transactions from those that independent undertakings would have applied in similar circumstances.

In view of this, the internationally acceptable framework is to apply the arm’s length principle to related-party transactions (that is, the OECD TP Guidelines), to ensure multinationals and their members apply market conformant prices as they would if transacting with third parties.

Meanwhile, VAT, as an indirect tax, normally flows through businesses so that it is the final consumer —not the business (with exceptions of players in the financial sector)— who bears the VAT burden. In principle, VAT should be charged on all supplies, including intercompany flows (with several special cases as exempt transactions or transactions within a VAT group).

Thus, regardless of whether the supply of services or goods takes place between related or completely independent parties, usually both local and cross-border transactions should be subject to VAT in the same way as long as the country where the supply takes place has a VAT system. This means the application of TP concepts could have significant overlaps with the application of VAT rules when it comes to intragroup transactions.

Now it’s time to examine several common points and differences that could be relevant considering the future cross audits.

Connections between VAT and TP

First connection: TP adjustments

Based on our experience, TP adjustments have been regularly audited by both the TP and VAT authorities. They can be either applied by the taxpayer, as a year-end adjustment when the tested profitability isn’t aligned with the taxpayer’s TP policy, or requested by the LTA, when they challenge the intercompany prices applied by the taxpayer.

But how can TP adjustments impact VAT? The VAT Expert Group at EU level has summarised the different VAT treatments in its non-binding material (Working Paper 923 taxud.c.1(2016)1280928 – 28.02.2017). The TP adjustment can be treated as either a consideration given in exchange for a supply of goods or services already supplied or a new supply of services or goods, or can be disregarded for VAT purposes. Hence, it’s crucial to analyse them on a case-by-case basis.

Second “apparent” connection: Article 80 of the EU VAT Directive

You may ask yourself, ”Where do I find the TP provisions in the VAT legislation?” Article 80 was introduced into Luxembourg VAT Law in 2018. When reading it for the first time, you may think there is a real TP provision in the VAT law. However, as you will see below, even if there is an apparent connection, there are some differences between TP and VAT rules too.

Personal subject

At a first glance, VAT and TP may seem quite similar, however the scope of the Article 80 provision has a much broader personal subject as it even includes a relationship having family ties or other close personal ties, whereas TP only focuses on the relationship between the companies.

Definitions to be used for TP and VAT purposes: arm’s length principle vs open market value)

The taxable amount should be adjusted whenever one needs to ensure that the related party transactions don’t trigger undue VAT benefits, which wouldn’t happen for transactions between third parties in the first place.

If you are wondering whether TP concepts should be used for VAT purposes as well in such cases, the answer is no. That’s because the Luxembourg VAT legislation —in line with the EU VAT Directive— has its own understanding of what the market value is to determine the taxable amount for related party transactions —that is, the open market value.

It’s important to note that, in comparison with the market value commonly applied for TP purposes, the notion of the open market value under the VAT legislation is much more restrictive in time and space.

Specifically when it comes to TP, the arm’s length price or compensation (range) reported in TP documentation is, in many cases, determined based on a sample covering a period of several years and including data of third parties in other jurisdictions. However, the VAT legislation (VATL) states that circumstances are only comparable if they come from the same country and the same period as the date of supply.

As a consequence, if the market value of a transaction should be established for both corporate tax and VAT purposes, taxpayers may reach different results. Moreover, in the absence of comparable circumstances, the VATL sets a “minimum” open market value, pricing as taxable basis similarly to the free of charge transactions.

It was also the final conclusion of the Jupiter case in the UK, where the tax authority declared that a cost-based TP method may result in the same valuation when comparing the price of a supply to the price of a similar transaction between unconnected parties following the arm’s length principles; however, the arm’s length and VAT open market value are different concepts. Hence, arm’s length valuations have no relevance for VAT purposes where there is no directly comparable actual transaction.

VAT adjustment is limited to specific cases

The taxable basis adjustments to the open market value for VAT purposes aims to avoid VAT loss for Member States in specific situations between related parties where the price of a supply of goods or services has been overestimated or underestimated.

For example, where a bank, established in Luxembourg, purchases IT services from another entity of the group, VAT should apply on the agreed price. However, the Luxembourg State budget would be harmed if the price would be lower than transactions carried out by non-related prices; so, in this case, the taxable basis should be adjusted to the open market value for VAT purposes.

Others

Moreover, the accurate delineation of intercompany arrangements when it comes to TP and the applied TP methods can have VAT impacts as well. For instance, if the tax authority challenges the latter and modifies the prices, the VAT basis should be amended as well.

Recent experiences regarding the local tax audits from both VAT and TP sides

For the time being, we haven’t yet seen actual cross audits launched jointly by tax authorities in Luxembourg. However, this could soon change given the draft bill’s implementation. In fact, we are aware of instances where the Luxembourg VAT authorities required the TP documentation to get the full picture on the audited group, including the intra-group transactions. In other cases, they used the TP documentation to challenge the price applied on services between related parties and claim additional VAT on this basis.

As you can see, TP and VAT have several connection points and it’s crucial to determine the relevant tax consequences given their specific characteristics. While the same tax authority —even the same tax unit—carries out the tax audit for all or more taxes in some EU countries, in Luxembourg, different tax authorities initiate tax audits on corporate tax (including TP) and VAT.

The table below highlights some of the recent trends we noticed regarding the audits for both VAT and TP.

Focus audit areas

TP

VAT

Availability of TP documentation supporting the arm’s length nature of the remuneration applied to intercompany transactions

VIES reconciliation (“VAT Information Exchange System”)

Compliance with the Luxembourg 2017 TP Circular, that is, equity at risk, arm’s length remuneration and substance

Reconciliation between the data reported in the VAT returns and booked in the annual accounts

Arm’s length nature of the interest rates

The recovery right of holding companies

Consistency across intercompany agreements, financial statements, tax returns, and actual conduct of the parties

Recharge of costs

TP adjustments

Evolution of the VAT audits

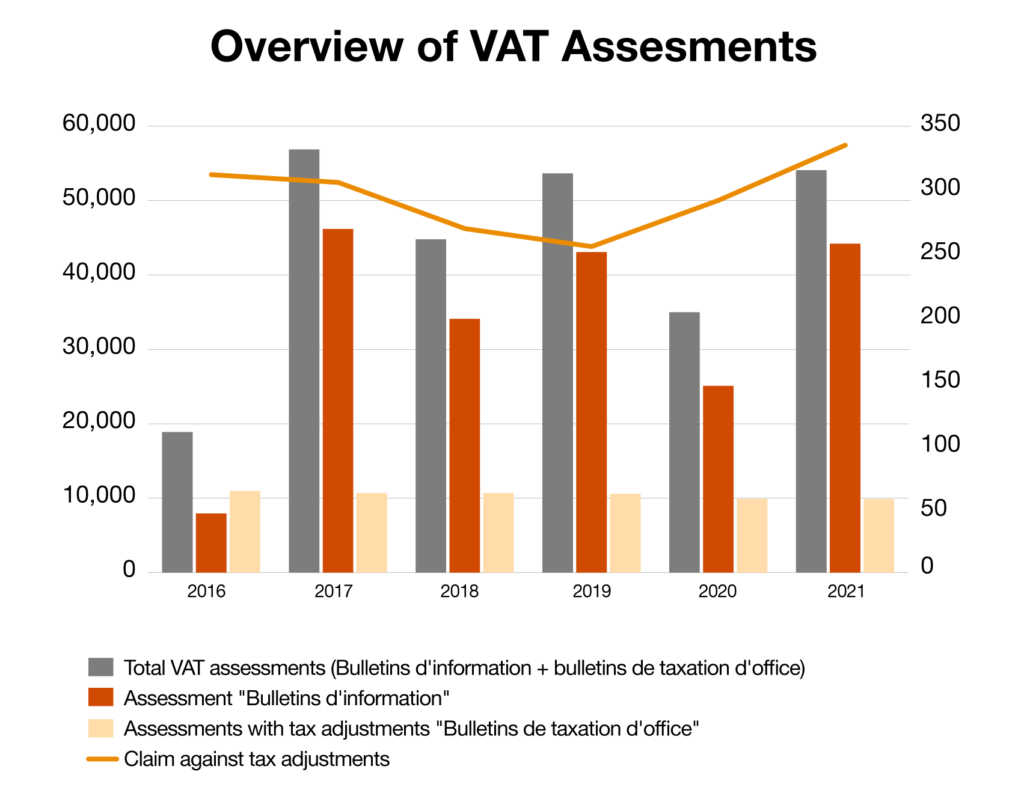

According to the 2021 annual report of VAT authorities—plus the fact that the VAT budget revenue and the number of registered taxpayers are constantly increasing in Luxembourg—the number of VAT audits is growing again after a short break during the first COVID-19 wave.

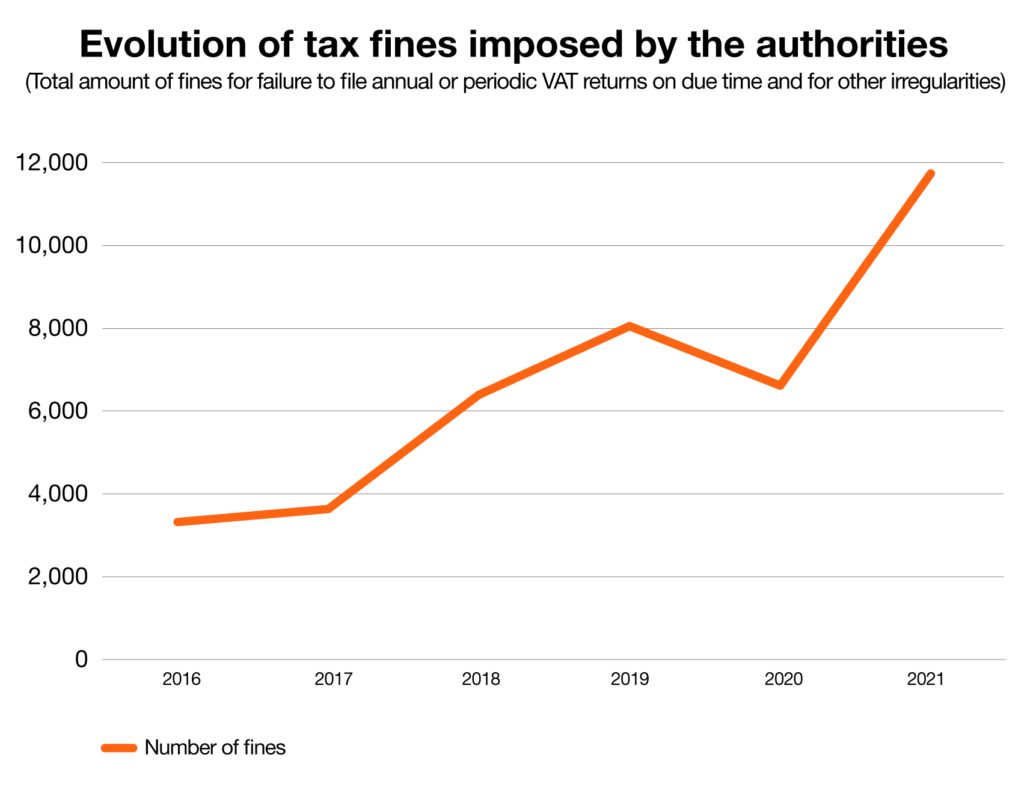

Authorities issue about 10,000 VAT assessments with adjustments each year. You can also see below that the amount of fines the VAT authorities imposed in 2021 increased significantly compared to the previous year.

Source: PwC Luxembourg (based on the Luxembourg VAT authorities 2021 annual reports)

Along with the increase of tax audits as well as tax assessments and fines, the type of audits has shown a different picture too. The number of on-site audits fell in 2020 and this number stagnated in 2021 –the pandemic lockdowns could explain this trend. Meanwhile, the request of FAIA (Standard Audit File for Tax) could become a focus for VAT authorities as the goal would be the VAT audits’ progressive digitalisation.

In the case of audit, the LTA may request supporting TP documentation and legal agreements for any intra-group transactions. The key takeaway for VAT and TP is to be ready upfront to answer any request with the relevant TP policy and documentation.

International outcomes

We recently did a survey involving PwC’s offices around Europe to identify the trends in other countries, but also to find out what we could expect in Luxembourg.

The results show that joint TP and VAT audits are already being carried out in several countries such as Austria and Hungary. However, there are still many countries where this kind of audit isn’t common or doesn’t exist at all —for instance, Estonia, Ireland and Poland.

The former group confirmed that the TP and VAT auditors are working separately in different departments of the tax authorities. As for the latter, the TP and VAT inspectors are part of the same team and don’t have a particular specialisation.

Additionally, several countries highlighted that tax units specialised in a certain type of tax (for example, TP in Hungary) can support the tax inspectors during the tax audits if needed. Furthermore, in most countries, the information, including the documentation, are exchanged automatically between the TP and VAT inspectors, even if they are working in different departments of the tax authority —that’s the case, for instance, in Czech Republic.

Undoubtedly, TP adjustments seem to be the focus of the crossed audits —which is in line with the Luxembourg VAT authorities’ practice. The business substance is also an area of focus, for example, in Poland, particularly for VAT purposes. It’s clear that many overlapping areas mentioned before are already a focal point for the tax authorities in Europe.

When it comes to the required documents, we can say there’s a fairly homogeneous picture in Europe. Tax inspectors always focus on the TP policy when TP is audited. In the case of VAT audits, the VAT returns, agreements, invoices, credit/debit notes, transport documents, accounting data, and SAF-T file (if any) are required to support the applied VAT treatment to the transactions in almost all countries.

To sum up, the growing cooperation between the TP and VAT audit departments is a clear trend in Europe.

Key areas of focus to manage a tax audit

Given the intensifying desire of the Luxembourg authorities to impose fines, taxpayers should focus on identifying the correct and proper tax treatment supported by underlying documentation. In the case of the intra-group transactions, the combined and aligned analysis for TP and VAT purposes is key.

Omnia mutantur (“everything is changing”) —holds the ancient phrase. Who knows? In the future, new topics might become the focus during a combined tax audit or the standard areas might be audited with another method and from other points of view.

Thus, taxpayers, now and in the years to come, should be ready in case a tax audit won’t go as smoothly as it had before, including if a minor discrepancy could be more severely sanctioned. This is what we noticed when the VAT authorities applied recent fines.

All transactions should be carefully reviewed for tax purposes, particularly before introducing a new structure, a new activity or a new transaction; it’s worth thoroughly examining the tax issues. However, we also advise reviewing the tax treatment of standard transactions regularly, as the legal frameworks and the authorities’ practice also change. We believe that if a tax analysis is very deep and thorough and the applied tax treatment is properly documented, the tax position is valid.

Key takeaway

The evolution in regulations and the access to more data by tax authorities will increase the focus on tax audits. In light of the international trend, we expect the Luxembourg tax authorities to pursue a combined approach on VAT and TP as a next step. Based on our experience, it’s important to anticipate such a development and ensure an alignment of the VAT and TP in your tax policy that could mitigate adverse tax consequences.

Foreseeing the approach of more joint reviews by the tax authorities, we should ensure alignment and consistency between VAT and TP analysis and related documentation and reporting. Otherwise, we can easily face the challenge of the tax authorities during a tax audit.

Marc Rasch, Partner, Transfer Pricing, at PwC Luxembourg

During the first large wave of TP audits, we have noticed some interest of the tax authorities in the VAT side. So, it’s expected that the increasing focus by the Luxembourg tax authorities on transfer pricing will in due course be expanded to a cooperation with the VAT authorities. Hence, a further alignment of your tax policy considering both VAT and TP together will be key.