Digital banking can give a boost to bank’s bottom line. When transactions are done on a mobile app instead of in a branch, they can be dramatically cheaper. They can also generate more revenue from clients who manage their money with a smartphone, tablet, or PC. But not all banks are prepared for a full digital transformation. We’ve identified three options for banks looking to start the transition. Which is best for your bank?

Which digital transformation is right for your bank?

How do clients connect with banks? The answer may be more troubling than you’d expect—and this could have real implications for your strategy. If you’re a banking executive, you’ll need new ways to attract this growing segment of “omni-digital” clients. Increasingly tech savvy, these clients gravitate toward lower fees, convenience, and ease-of-use.

So you want to become even more digital. To compete, you should drastically alter your cost structure and improve your offerings. Moving away from traditional hardware-based IT and embracing cloud-based technologies can help. But how do you figure out which digital transformation is “just right” for your organisation?

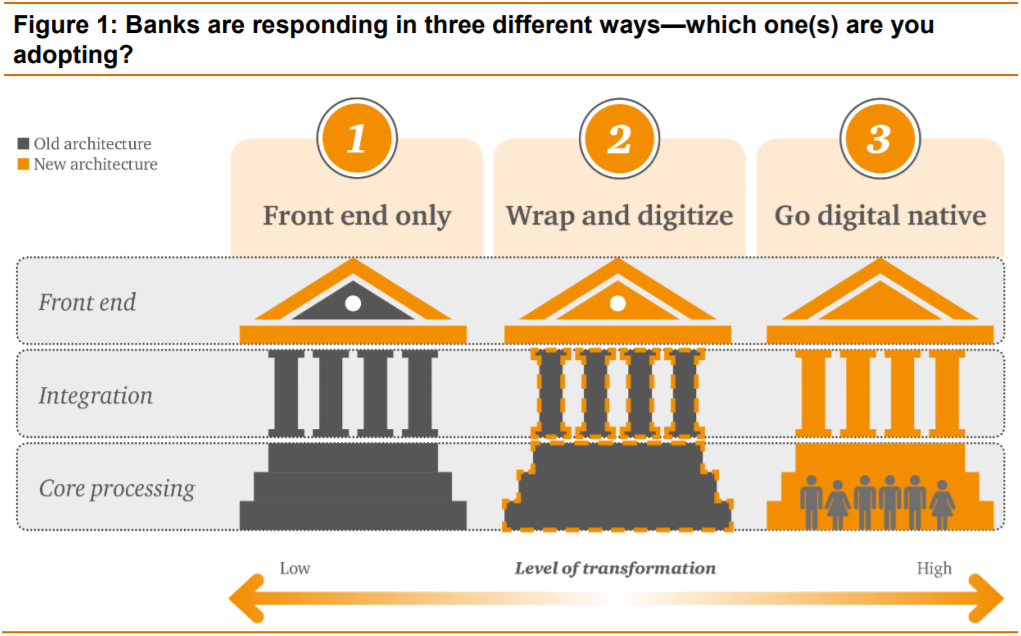

Broadly speaking, there are three options for banks looking to start a digital transformation. Here they are:

1. Digitise front-end only

The simplest approach is to modify the front end only, focusing on the primary ways a customer interacts with a bank, e.g. website and app. Mostly a cosmetic fix, the bank designs an appealing mobile app and web interface but keeps the organisation’s workflows, culture, and back-end infrastructure intact.

For an organisation that needs a quick win, it’s certainly the fastest route. In fact, this approach may be a quick interim step for banks that have real client-facing issues. It’s a solid stop on the road of transformation, but for most banks, it won’t be the destination.

After the initial fix, clients may see their bank becoming more digital. Behind the scenes, though, the bank remains limited in what it can deliver. Clients might be able to apply for a credit card using a mobile app. But without integration of back-end systems and no fundamental change to the operating model, the experience will be not be significantly different than what clients had before. In other words, the front end promises what the back end can’t deliver.

Fixing the front end might help reduce customer churn. Unfortunately, the gains may not last if the back-end can’t meet or exceed customer expectations—and quickly, too. In fact, costs could increase if you have to add employees to maintain the new digital front end or assign an additional IT team to design and build solutions to fulfil customer requests.

In the long run, digitising the front end without making additional investments could cost more than sticking with the status quo. Still, it’s a starting point for banks facing budget or organisational constraints that make a more extensive transformation difficult.

2. Wrap and digitise

With the wrap and digitise approach, you fix the front end and go one step further, gradually replacing legacy infrastructure with digital technology, integrating the middle and back offices along the way.

Wrap and digitise improves customer experience more than the front-end-only approach because of improved infrastructure and organisation. A bank undergoing this type of transition will look different in the following ways:

Many banks form business transformation groups internally or bring in external partners.

Employees might be transitioned to higher-value roles in new centres of excellence, as this conversion eliminates the need for certain manual tasks.

The biggest drawback that banks find in this approach is that it’s a long process. Because wrap and digitise focuses on individual improvements, it can take some time before the full scope of the bank’s processes has been overhauled. Still, this is a great option for banks that need to take a more gradual approach. They can test out an individual IT improvement and show benefits quickly once they go live. Frequently, this can be a cost-effective approach. It can be a much easier sell to leadership, too, avoiding some of the political conflict that a full-blown transformation can often introduce.

3. Go digital native

Some banks choose to go all in. They create a digital native bank that uses a fully digital customer interface and back end. This strategy can deliver significant cost savings as well as the ability for the bank to adapt quickly when change comes.

These banks generally start as minimally viable banks (MVBs) offering just a handful of products. A basic retail bank, for example, might focus on deposits, payments, or lending. This approach to digital transformation is poised for explosive growth with the rise of challenger banks, start-ups that directly challenge the products and services of traditional financial institutions.

Reducing costs is one reason to go digital native. But the main reason banks decide to go digital native is that it makes them much, much more agile. It lets them adapt to rapidly changing customer tastes, and it lets them test and iterate rather than commit and hope. The digital core and open architecture also allow flexible approaches for partnering with third parties to offer a range of products and services. It’s now possible to set up a fully functional, digital native bank using third-party architecture in the cloud. Using modern infrastructure, you can quickly tailor product and service offerings, such as new account types or advisory services, as well as change pricing when necessary.

Under this model, your clients are likely to have a drastically different banking experience, and one that most will find more appealing:

They will have seamless experiences that are designed based on their needs instead of having a bank trying to sell them products.

Banking processes such as opening accounts and signing up for offerings will be much less time consuming and more convenient based on individual preferences. Your clients will be able to use the channel of their choice to conduct their business.

You’ll be able to tailor products to your clients’ needs on the fly. This is almost impossible to do with legacy systems.

If this is so attractive, why don’t we see more of it? Usually it comes down to perceptions of expense. Many financial institutions think it’s costly and time consuming to launch a fully digital bank, though this doesn’t have to be the case. Using cloud technology, it’s now possible to launch a digital native bank in months and at far less expense than ever before. And the options aren’t mutually exclusive: you can combine this with the wrap and digitise approach, with clients gradually transitioned away from the legacy system toward the digital bank.

Digital banks won’t bypass the regulatory environment in the United States. US regulators expect new entrants to meet the same reporting and consumer protection standards as incumbents. But the agile design of digital banks could help them stay ahead of a changing regulatory landscape, adapting as necessary.

Launching a digital native bank requires a new way of thinking. It’s a radically different operating model that calls for smaller, less siloed middle-office and back-end teams. It also emphasizes buying or partnering with vendors rather than building technology solutions.

How to choose your digital strategy?

Many banks have started down the path to digital transformation. But these efforts are often ad hoc and fail to yield the expected improvement in profitability. To increase the odds of success, we recommend you to refine your long-term organisational strategy and define the endpoint before you get started. Only then you can decide which digital transformation strategy is just right for your bank. A good first step is to consider questions like:

What do we want to be known for?

Which consumer segments are we targeting?

What are our core capabilities and how can a digital strategy strengthen them?

Once you’ve examined the options, consider the trade-offs and potential conflicts associated with each model, keeping in mind factors like organisational strategy and culture, existing technology, cost pressure, and risk appetite.

We’re summarising this in the following graph:

What we think

Roxane Haas, Banking Leader

Digital banking can give a swift kick to your bank’s bottom line. When done on a mobile app instead of inside a branch, the cost of a typical transaction shrinks dramatically. You can also generate more revenue from clients who manage their money with a smartphone, tablet, or PC. These omni-digital consumers using self-service channels tend to buy more financial service products beyond savings, borrowing, or investments than their counterparts visiting a bank branch. The upshot: omni-digital consumers are less expensive to serve and generate higher customer lifetime value.

Patrice Witz, Digital Leader

Banks that don’t move in this direction may quickly find themselves on the wrong side of a relentless demographic shift. Increasingly, the most attractive customer segments by age and net worth expect a seamless experience from their financial institutions. Whichever option you choose, pause from time to time to make sure that your plan remains aligned to your long-term strategy and that you’re using the right options based on your core capabilities and available technology. If not, make the appropriate adjustments and keep going. The important thing is that you get started.”