Can you imagine what would be like to have wholesale insurance using blockchain? We take a look at those unique features of blockchain that are likely to create new organisational and operational opportunities for the insurance sector. Here are the three main areas where blockchain could be a game-changer:

Know Your Customer and Anti-Money Laundering checks;

Claims Management.

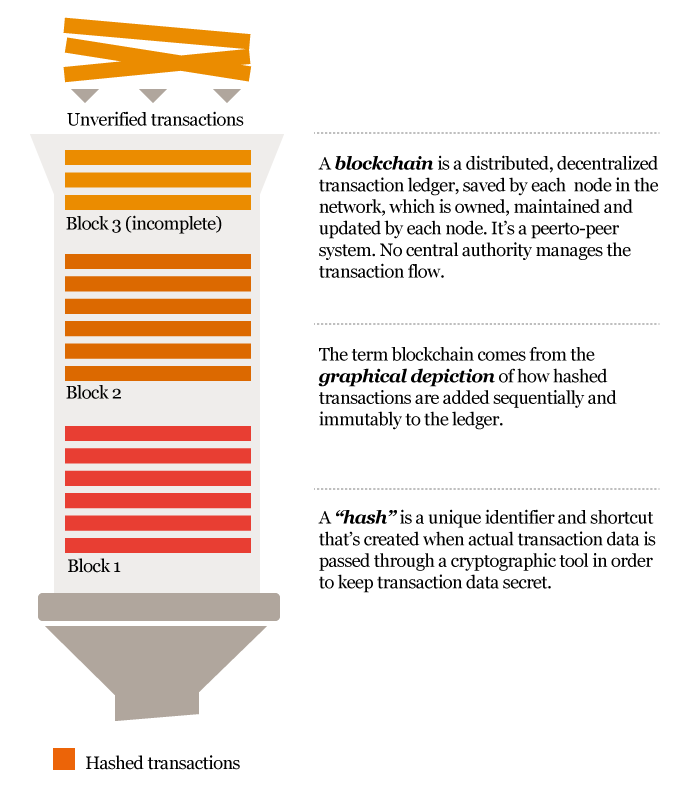

How blockchain works

Placement and contract lifecycle documentation

Potential benefits: reduced processing cost and time; instant availability of accurate current information; legal certainty.

Wholesale insurance contracts demand the storage of great volumes of ancillary files or electronic ‘real life’ documents throughout the placement process. In addition, as each participant has to check them at every stage of the interaction and even several times within the deal’s lifecycle, the process becomes heavy and time-consuming.

Using a blockchain to store all contract-related documents or appendices shared between brokers and underwriters, as well as reinsurers and claims agents, would guarantee that every reference is consistent and therefore remove the need to check the same file over and over again. It could also accelerate the use of structured and semi-structured electronic documents rather than scanned paper, hence fewer costs and errors.

Blockchain could be available for other wholesale insurance stakeholders (e.g. regulators, tax authorities, etc.), which would simplify reporting.

Know Your Customer and Anti-Money Laundering (KYC/AML) checks

Potential benefits: reduced processing cost and time; insurance of time-critical transactions; improve privacy and data protection; reduce reputational risk from delayed payments of claims.

Brokers, insurers and reinsurers have to perform KYC/AML checks, sanction screening and identify the ultimate beneficial ownership for all of their counterparties – legal entities and individuals.

If a client works with a broker who deals with multiple underwriters, a single transaction can involve several participants. They all have to do KYC/AML verification along the chain, which multiplies efforts for the same task and adds to cost and delays.

A blockchain-based certified file transfer utility could help reduce these costs significantly. The blockchain records the client’s personal documents, as well as the evidence of validation by each player in the insurance life cycle. All documents on the blockchain are encrypted and keys belong to the client. This solves a set of regulatory issues around privacy and data protection. The client can then provide blockchain entries together with an appropriate subset of keys to their next business partner, and the latter can rely on the validation done by the bureau without delay. As a result, stakeholders would spend less time on KYC/AML checks and less money.

Claims management

Potential benefits: reduce costs and time; legal certainty; reduce reputational risk from mishandling claims.

When a claim is made on a policy, each underwriter involved wants to keep receiving information on the progress. Usually, there’s one claims broker coordinating the process. However, there could be multiple underwriters pursuing their own process and therefore generating additional costs for themselves and the client.

A blockchain could incorporate all documents created in the claims process and make them available to all underwriters, as well as to the client broker and claims broker. This would enable more underwriters to accept the claims process without actively participating, as they would be able to monitor and review them. It would also reduce errors, avoid duplication of communication and, therefore, limit administrative expenses for the claims broker.

What we think

Matt Moran, Insurance Leader

For blockchain to become reality in the wholesale insurance industry in Luxembourg, stakeholders have to closely collaborate and analyse potential uses. We know insurance has been a slow adopter of new technologies compared to other financial sectors, but the efficiency gains flourished by process automation make some place for new approaches. Global insurers and reinsurers increasingly like the idea of tamper-proof record-keeping, the replacement of a central authority with decentralised processes and smart contracts.

Gregory Weber, FinTech Leader

With the large back-office cost savings and transparency gains that blockchain can provide, it is imperative that wholesale insurance stakeholders understand the potential impact of this technology on their activities. 77% of the respondents to our 2017 Global FinTech Survey expect to adopt blockchain as part of their systems or processes by 2020. So, blockchain will rapidly become a common element found in business processes.