The European Parliament has approved the new Regulatory Technical Standards for PRIIPs in early April. Whether you are an insurer, banker, asset manager or third party, you fall within their scope. With these new standards, you can now start the PRIIPs process, as the guidelines clearly identify the items to include in the Key Information Document. Here are a few facts you need to know to start your compliance journey.

Understand PRIIPS

The Packaged Retail Investment Product (PRIIPs) regulation is a piece of legislation that aims to improve the quality of information provided to consumers. It introduces a standardised fact sheet, known as a Key Information Document (KID). This document presents the main features of an investment product in a simple and accessible manner. Thanks to the KID, European consumers will be able to compare the potential risks and rewards of investment products, funds and investment-linked insurance policies.

Any finance industry player (e.g. asset managers, bankers and insurers) who manufactures financial products (e.g. investment funds, life-insurance products, structured products and derivatives) and sell them to retail clients are on the radar.

Here’s a non-exhaustive list of products that fall within the scope of PRIIPS:

Investment funds;

Life insurance-based investment products;

Retail structured securities;

Structured term deposits;

Derivatives;

Convertible bonds and other structured securities with embedded derivatives;

Pension products and annuities not recognised in the national law.

Feed your KID

You’ll need to create the KID before giving the PRIIPs to retail investors. You can provide investors with KIDs on paper or via a website. The regulation is clear that, when selling PRIIPs face-to-face, paper should be the default option.

Each KID must include:

a prescribed explanatory statement concerning the purpose of the KID;

information concerning the manufacturer and its regulator;

a comprehension alert for complex products, including derivatives and structured products governed by the current Markets in Financial Instruments Directive (MiFID) regime;

a section headed ‘What is this product?’, setting out information describing the PRIIPs, including type, objectives, target consumer, details of any insurance benefits and term;

a section headed ‘What are the risks and what could I get in return?’, setting out the risk-reward profile of the product using prescribed information;

a section headed ‘What happens if the PRIIPs manufacturer is unable to pay out?’, containing details of guarantee schemes or other covers;

a section headed ‘What are the costs?’;

a section headed ‘How long should I hold it and can I take money out early?’, containing details of recommended holding periods and the consequences of cashing in early;

complaint redress information;

a section headed ‘Other relevant information’, detailing other information documents required from the investor.

Our view

Benjamin Gauthier, partner

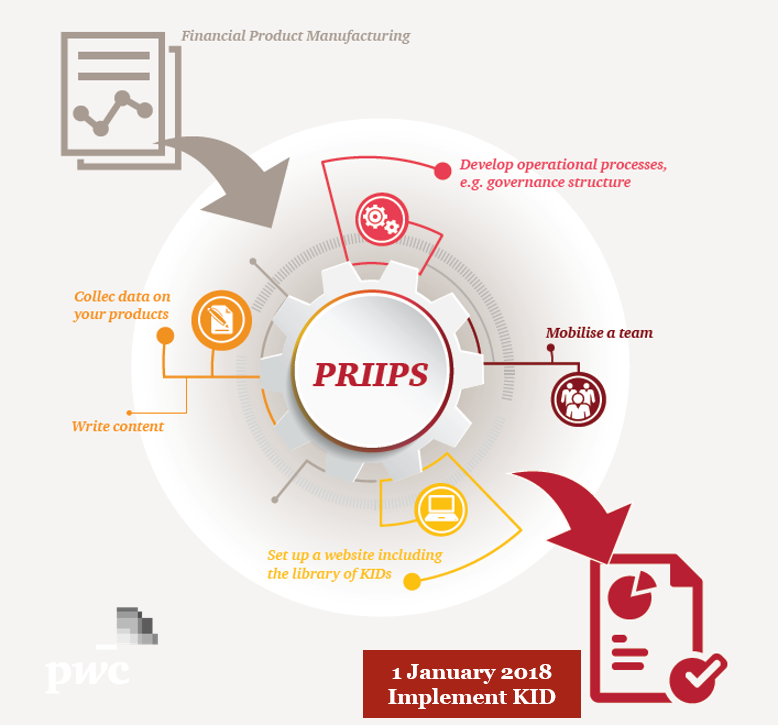

Now that the Parliament has validated the RTS, players need to identify the products that fall within the scope of PRIIPs. Don’t underestimate this step as it might be more complex than it seems. The KID includes descriptive product information, risk and performance metrics, details of costs, etc. As a result, the content can’t be the result of a single person or a single team, but rather different sources. And this might be quite challenging.

Additionally, the deadline for issuing KIDs will correspond to the MiFID deadline and, later, IDD – the equivalent of MiFID for insurers.

Finally, the RTS have some inaccuracies in the implementation of the rules. These points should be clarified in the step 3 (documentation production), but at this stage we have little information.

Many players might see the KID as an additional regulatory requirement. Yet, complying with it will be necessary to distribute products after 1 January 2018. Therefore, players should take their journey quickly.

To know more about PRIIPS, take a look at thispage.

simple and accessible manner. Thanks to the KID, European consumers will be able to compare the potential risks and rewards of investment products, funds and investment-linked insurance policies.

simple and accessible manner. Thanks to the KID, European consumers will be able to compare the potential risks and rewards of investment products, funds and investment-linked insurance policies.