Building public trust is a priority for companies and the industries they are part of, to increase their resilience in a world where technological advancements are caffeine and confidence is an anxiolytic that balances things out.

Clear communication around tax is one way to be trustworthy.

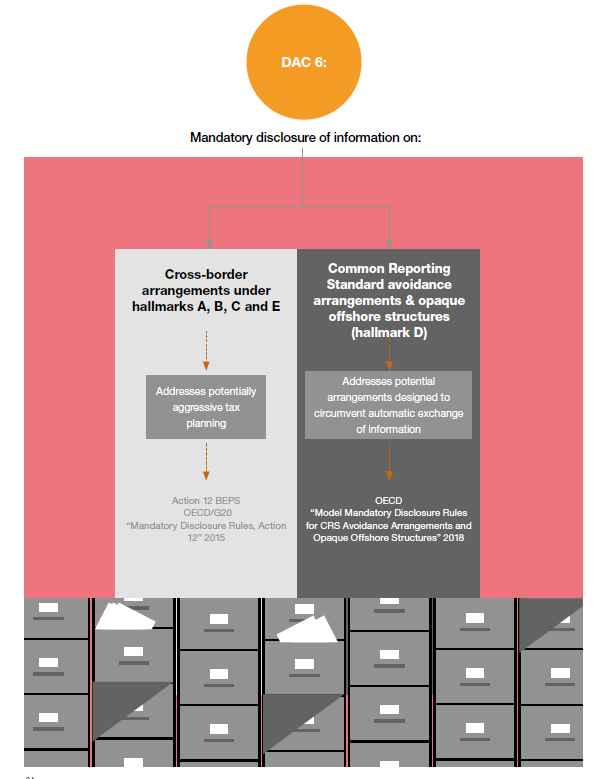

Following MiFID IIand the push for financial markets to become more transparent, improve investor protection, standardise practices and restore confidence in the investment industry, the EU is introducing an additional level of transparency to detect potentially aggressive tax arrangements. The 6th Directive on Administrative Cooperation (DAC6), an amendment to Directive 2011/16/EU, aims to do precisely that.

DAC6 aims at transparency and fairness in taxation linked to cross-border tax arrangements.

Adopted on 25 May 2018 by the Economic and Financial Affairs Council (ECOFIN), the directive demands tax intermediaries for a detailed reporting on a broad range of “cross-border tax arrangements.” Reporting is needed if the arrangements contain at least one “hallmark”.

DAC6 applies to cross-border tax arrangements. It concerns either more than one EU country or an EU country and a non-EU country. The term”arrangement” is meant to have a broad meaning and may also include a series of arrangements.

Hallmarks are specific characteristics or features of cross-border arrangements that might present an indication of a potential risk of tax avoidance.

To comply with DAC6, each EU member must introduce compulsory disclosure rules for cross-border arrangements in its national law. Failing to comply with DAC6 could mean facing significant sanctions under local law, and reputational risks for businesses, individuals and intermediaries.

DAC6 doesn’t leave room for taking action later. While the mandatory reporting starts in 2020, the directive asks for reporting on transactions that happen during the period right after being adopted, namely as of 25 June 2018.

DAC 6 will affect many EU companies and multinationals, especially intermediaries — law firms, financial institutions and other advisors. However, individual taxpayers will be affected too.

In this article, we explore this new directive and what it implicates and give two tips for businesses to kick off their preparations.

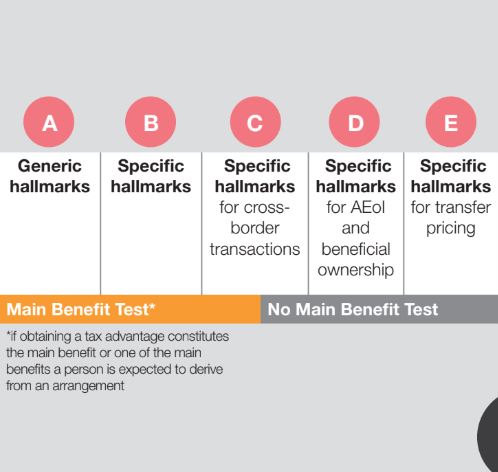

DAC6’s hallmarks in simple words

As we mentioned above, the occurrence of at least one hallmark will trigger reporting on cross-border arrangements.

Hallmarks, according to the directive, fall into the five categories the figure below depicts.

However, hallmarks only trigger reporting obligations when an arrangement meets the main benefit test (MBT).

When the benefit a person may expect from an arrangement is a tax advantage, then the benefit test is satisfied and it’s subject to reporting.

Reporting through DAC6

According to DAC6, the reporting obligations apply only to EU-based tax intermediaries unless the reporting breaches any legal professional privilege in the country of residence. In the absence of an intermediary, the responsibility falls on the taxpayer.

Intermediaries need to report to the tax authorities in the country where they are resident any potentially aggressive tax planning arrangement with a cross-border element.

By means of the Common Communication Network (CCN) that the EU will set up later, the EU member state share information with the others.

Reporting is set to happen quarterly.

If the taxpayer develops the arrangement in-house, or is advised by a non-EU adviser, or if legal professional privilege applies, the taxpayer must notify the tax authorities directly.

What about Luxembourg?

In Luxembourg, as in every Member State, there will be work to be done for DAC6 Directive compliance once it’s transposed into local law.

The Grand Duchy is a leading financial centre in Europe and, more specifically acentre of excellence for fund distribution. In fact, 61% of authorisation for cross-border distribution around the globe comes from funds domiciled in Luxembourg. That calls for special attention to the DAC6 requirements as the cross-border element is nearly everywhere.

Because Luxembourg is yet to vote the law to implement DAC6, the impact on financial services and, more precisely, on tax intermediaries will be unveiled later. Even once transposed, only practical market experience, and additional guidelines, will shed light on the regulation compliance.

Luxembourg businesses want to invest time in understanding the DAC6 requirements and to assess as accurately as possible the administrative load for due diligence so they avoid any delay. It’s important to point out that financial penalties for non-compliance haven’t been defined by the Directive itself but will have to be set by every Member State. Uncertainty, for now, is an unavoidable companion on the path toward DAC6.

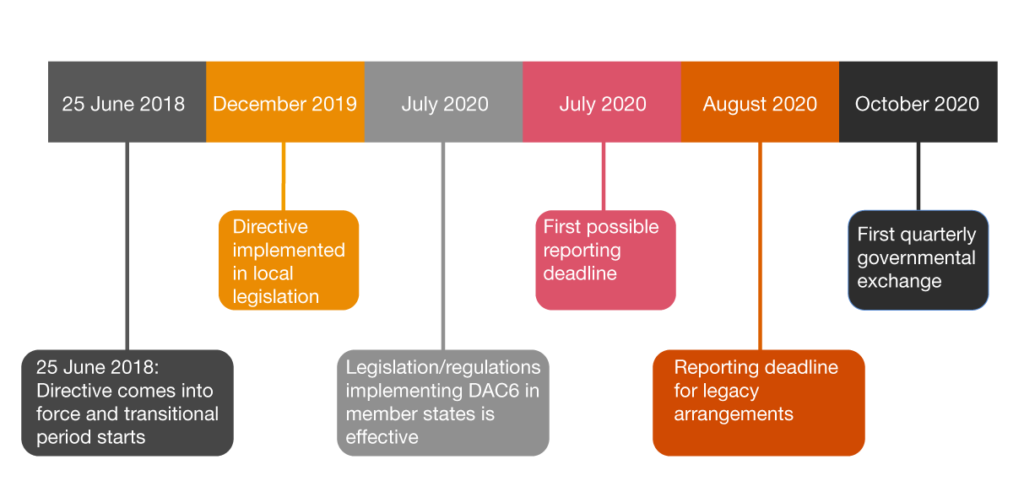

The DAC6 Timeline

The chronometer is running. As you might have noticed so far, there are quite a few details that need to be cleared out before the first reporting is made by 31 August 2020.

All the information collected by the local tax authorities on the use of arrangements will be automatically transferred to the tax authorities of all other EU Member States through a centralised database or the CCN. The exchange of information should take place within one month following the end of the quarter when the information was filed. Accordingly, the first information is to be exchanged by 31 October 2020.

DAC6 Timeline

What we think

Murielle Filipucci, Partner at PwC Luxembourg

Staying on the right side of any new regulation is absolutely crucial. In the case of DAC6, start by having a clear understanding of it to ensure compliance by the deadline. You need a well-thought plan to identify and report any cross-border tax arrangement that falls under the DAC6 scope. Make sure that the documentation of arrangements, including those dating back to June 2018, is done in an efficient manner. Aim at being compliant right from the start!