In late 2009 and for the next few years, the atmosphere was heavy in number 175, rue de la Loi, in Brussels. Heads of State and Ministers of Finance were gathering quite frequently in this building—that is, the Council of the European Union—and staying there until late in the night (or sometimes until early in the morning). All because they were at a loss.

You see, those were the sombre days of the European debt crisis, which was, in technical terms, caused by a balance-of-payments crisis. In layman’s words, several eurozone member states—namely, Greece, Italy, Portugal, Ireland, Spain, and Cyprus—suddenly stopped receiving foreign capital, and since they had significant deficits and were dependent on foreign lending…well, disaster struck.

These countries were unable to repay or refinance their government debt or to bail out over-indebted banks. Moreover, their inability to resort to devaluation—that is, reductions in the value of the national currency—because of the shared currency, the Euro, made matters worse.

Don’t have time to read the whole blog entry? Then watch our “Blog in 1 minute” video for a quick summary of its main points:

The intricate causes of the crisis varied from country to country, so we will spare you the details because your time is precious and we don’t want to stir up too much the painful memories of that dark period in the European Union’s history.

But we do want to mention, for a good reason, that back then there was a lack of fiscal policy coordination among eurozone member states that contributed to imbalanced capital flows. Additionally, financial regulatory centralisation among eurozone states was missing, which made supervising large groups in a centralised, cross-border way, difficult.

The silver lining when such a crisis strikes is that, hopefully, one can learn from one’s mistakes. This leads us to the subject of this blog entry: the European Central Bank (ECB) priorities. First, we explain what these priorities and the Single Supervisory Mechanism are, and give you the context behind them.Then, wedeep dive into each of the priorities for 2023-2025, and finally, share with you some of the results for the 2022 Supervisory Review and Evaluation Process.

The European Central Bank priorities in a nutshell

After the 2008 financial and economic crisis, and as a result of it, the European Central Bank, headquartered in Frankfurt, Germany, created the Single Supervisory Mechanism (SSM), a supranational mechanism of banking supervision for Europe.

Through this mechanism, the ECB works with national supervisors (called “National Competent Authorities” or NCAs) to ensure the safety and soundness of the European banking system, and that banks can perform their crucial role in supporting the real economy.

To do so, at the end of every year, the ECB defines a number of supervisory priorities to determine its focus for the three years ahead. These priorities are based on what it considers to be the key risks and vulnerabilities that supervised institutions face given the economic, regulatory and supervisory landscape at a given period.

As part of its supervisory practices, the ECB assesses the risks banks face and checks that they are equipped to properly manage those risks. This is called the Supervisory Review and Evaluation Process, or SREP—we will talk about it later, so stick with us!

Note: There’s a difference between a regulator and a supervisor. The former sets the rules, while the latter makes sure they are enforced, and thus there’s a segregation of duties.In some countries or fields, the two roles are combined but no longer in banking.

The ECB priorities and Luxembourg

As of the writing of this blog, there are five banks headquartered in Luxembourg, which the ECB directly supervises: Spuerkeess, JP Morgan, Quintet, RBC Investor services and Banque Internationale à Luxembourg (BIL).

However, there are a total of 124 banks in the Grand Duchy. So, what about the other 119 banks? Well, for about half of them, they are supervised by the Commission de Surveillance du Secteur Financier (CSSF), the public institution that supervises the professionals and products of the Luxembourg financial sector but under the ECB’s single rule book nonetheless.

As for the subsidiaries of a large bank, such as BGL BNP Paribas Luxembourg, ING Luxembourg, and Société Générale Luxembourg, they belong to groups that are massive and therefore are under Frankfurt’s direct supervision as well.

To sum up, large banks and their subsidiaries are under the ECB’s supervision, while the CSSF focuses on smaller banks. What’s important to note is that both the ECB and the CSSF apply the same rulebook.

However, there’s some room for flexibility. Some banks in Luxembourg are rather small, employing for instance 25 to 30 people, and so, as a principle of proportionality, the CSSF can adjust the timeline and the level of exigence or ‘intensity’ as opposed to the ECB, which will be quite demanding of large banks.

Another note: the rulebook we mentioned is also known as the single rulebook as it applies to the more than 5,000 banks in the eurozone.

The reason(s) behind the ECB priorities

We told you we didn’t want to waste your time, so here we go, straight to the point: the ECB priorities ensure that banks are moving fast enough in key areas for financial stability. Hence, to be clear, the ECB doesn’t have a political role, but a financial stability one. “Sure, but what’s the difference?” you ask.

To clarify what we mean, let’s take the example of the EU taxonomy. The financial sector is a big supplier of funds to many different industries. Hence, the European Commission and the European Parliament would like the banking sector to have a key role in redirecting EU funds to sustainable investments.

And so, they capitalise on other organisations, such as the ECB, to drive banks into that direction. That’s the political will.

However, these organisations don’t fall for it. Instead, they usually reply that that’s not really their role. They can’t actually push banks to invest in green if that’s not what they want. Rather, their role is to look at how these banks manage the risk associated with their choices and ensure their stability and robustness, i.e. that they are aware of the risks they are taking by investing into activities that may go against the political view and therefore potentially more exposed to credit or liquidity risks (imagine investing in a security that nobody wants to buy from you in a few years’ time).

Deep diving into the 2023-2025 ECB priorities

In December 2022, the ECB published the priorities for 2023 to 2025. They are a little different from the 2022-2024 ones, but there is still an overlap. In fact, let’s say it’s an evolution rather than a revolution. This is mostly due to the change of geopolitical environment with the war in Russia and the Covid crisis gently coming to an end.

Below, we deep dive into the three supervisory priorities and the corresponding vulnerabilities banks in Luxembourg are expected to address over the coming years.

As part of the process, the ECB will perform targeted activities to assess, monitor and follow up on the identified vulnerabilities. Each vulnerability is associated with its overarching risk category.

Priority 1. Strengthening resilience to meet immediate micro financial and geopolitical shocks.

Given the current uncertain environment we live in, it’s fundamental that the banking sector remains resilient and that banks focus on the impact of external shocks on their businesses. Note that the geopolitical risks are a new component of the priorities and it’s mainly due to the war in Ukraine.

Click here to expand or collapse for more details

1.1 Shortcomings in Credit Risk management

Identify and mitigate any build-up of risks in exposures to more vulnerable sectors, remedy structural deficiencies in credit risk management cycle, from loan origination to risk mitigation and monitoring, and address in a timely manner any deviations from regulatory requirements and supervisory expectations.

Check out the video to learn in more detail about the credit risk management frameworks:

1.2 Diversification of funding sources and deficiencies in funding plans

Expected diversification of funding structures, especially regarding less stable funding sources, through sound and credible multi-year funding plans, taking into account changing funding conditions. While these priorities were published in December, they were a bit visionary when looking at the current turmoil in the banking sector on both sides of the Atlantic.

This priority is about the need for banks to keep a strong focus on working on structural challenges and risks stemming from the digitalisation of their services. The goal is to make sure their business models remain resilient and sustainable.

Click here to expand or collapse for more details

1.1 Deficiencies in digital transformation strategies

Develop and execute sound digital transformation plans through adequate arrangements (for instance, business strategy, risk management, among others) to strengthen their business model sustainability and mitigate risks related to the use of innovative technologies. This has not only an impact on banks’ ability to attract and retain their customers, but also to reduce their costs while increasing their ability to meet the ever-increasing regulatory compliance expectations.

1.2 Deficiencies in Operational Resilience frameworks

Develop robust outsourcing risk arrangements as well as IT security and cyber resilience frameworks while ensuring adherence to the relevant regulatory requirements and supervisory expectations. This has been a source of concern for authorities for the last 10+ years and is showing no signs of going away.

Check out the video to learn in more detail about operational risk:

1.3 Risk data aggregation and reporting

Address long-lasting deficiencies and have adequate and efficient risk data aggregation and reporting frameworks in place. This is about banks’ ability to quickly respond to changes in their environment and the current Silicon Valley Bank (SVB) would be a very good case in point. For example, how long does it take you to assess your exposure to SVB or any other name with which level of certainty?

1.4 Management bodies’ functioning and steering capabilities – NEW

Develop and implement sound remedial action plans to address material deficiencies in the functioning of management bodies and adhere to supervisory expectations.

This is a new component of the ECB priorities that mainly concerns the board of directors. More precisely, whether they are equipped to make decisions, trained, and knowledgeable about what is being done in their banks.

Check out the video to learn in more detail about the priorities reflecting changes in risk drivers and the outcome of the 2022 SREP:

Priority 3. Stepping up efforts in addressing climate change

It’s clear that climate change can no longer be considered only as a long-term or emerging risk as its impact is already palpable and is expected to increase substantially in the coming years. Hence, it’s more and more urgent for banks to address the challenges and grasp the opportunities of climate transition and adaptation.

Click here to expand or collapse for more details

Material exposures to physical and transition risk drivers

Adequately incorporate climate-related and environmental (C&E) risks within the business strategy and governance and risk management frameworks to mitigate and disclose such risks, aligning practices with current regulatory requirements and supervisory expectations.

Check out the video to learn in more detail about the exposure to climate-related and environmental risks:

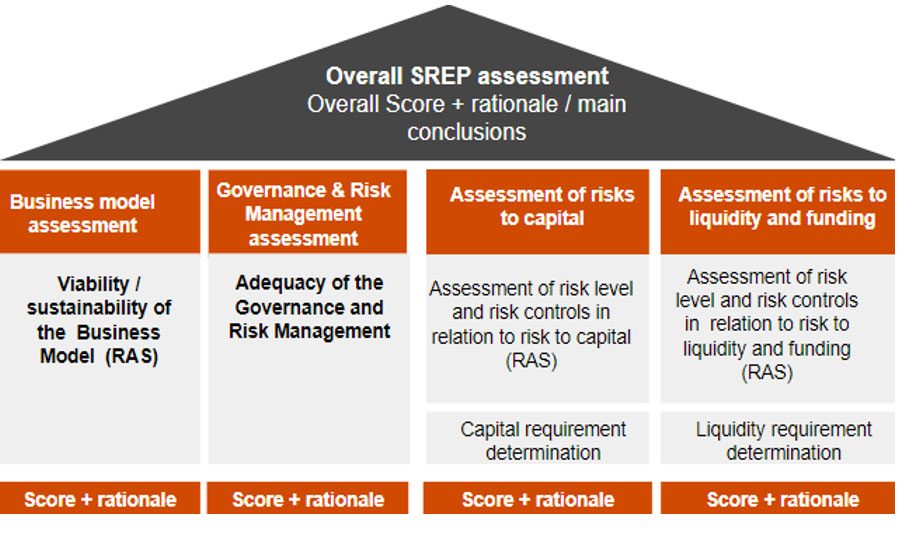

A look into the Supervisory Review and Evaluation Process (SREP)

The ECB performs the SREP on an ongoing basis to assess the risks banks are facing and whether they adopt the adequate risk management measures to tackle those risks efficiently.

In other words—and probably, less technical—its purpose is to assess how safe and sound the banks are individually. It looks beyond the identified priorities (which is kind of a separate exercise) to check how robust banks are on four pillars: business model, capital, liquidity & funding, as well as internal governance.

Banks receive an individual score for each of these pillars, as well as an overall SREP score. The result of that scoring will have an impact on how much more capital or liquidity the banks must hold, which, in turn, can have an impact on return on equity, for instance.

On a yearly basis, the ECB publishes aggregated (and anonymous) SREP results, while banks receive letters with their individual results. Think of it as a kind of school report if you like.

The 2022 SREP results

The aggregated SREP results for 2022 were released in January 2023 and can be found on the Banking Supervision webpage. Otherwise, you can keep reading this blog as we share the key messages and figures for the 119 banks in Luxembourg.

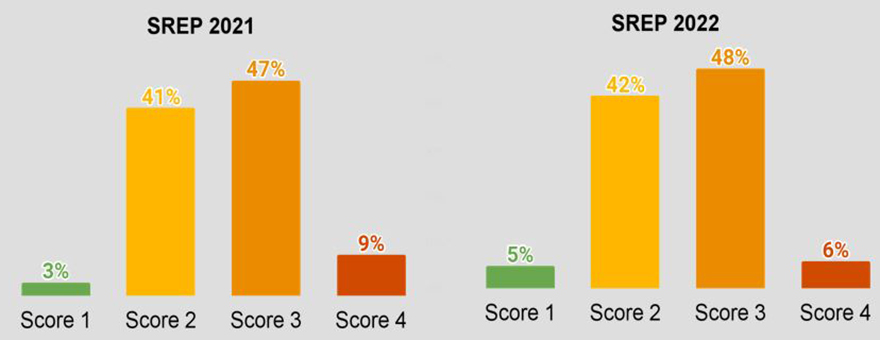

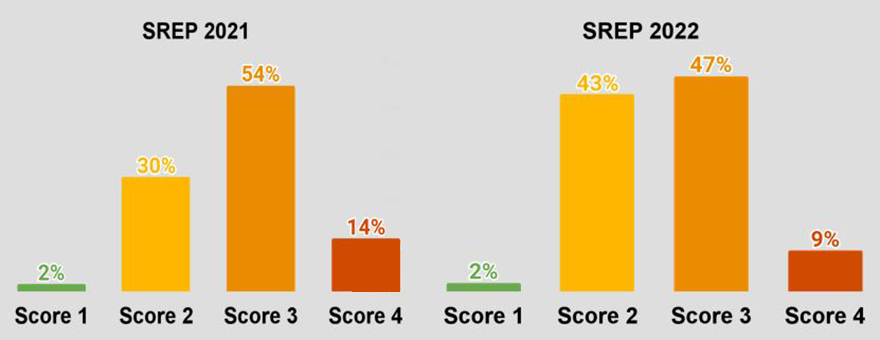

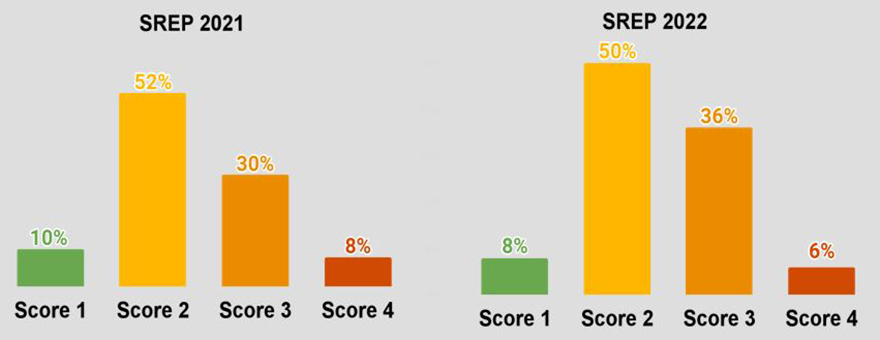

#1 The 2022 SREP overall scores are relatively stable compared to 2021, with a minor increase of banks with a score of three and decrease of banks with a score of four. In fact, 92% of banks kept the same score as the previous year.

Also note that no bank has gotten a score of one, which means most students get the “decent but can do better” remark in their school report, and some clearly get an official warning.

#2 About 95% of the banks have received qualitative measures (i.e. a request to recruit more experts in some dimensions, to boost their internal governance arrangements etc.) , and the overall number of measures increased by 14%.

#3 Key focus of qualitative measures: internal governance (28%, stable compared to 2021), credit risk (18%, improved), and capital adequacy (14%, stable).

#4 Key findings of the 2022 SREP are aligned with the 2023-2024 priorities.

Key results and risk drivers by SREP elements

Business model

Net interest income rise improved Return on Equity (ROE)

Long-standing issues, that is, high cost to income ratio, slow digitalisation

Climate risk management accounts for 23% of the qualitative measures and strategic plan update for 15%

Internal governance and risk management

Lack of effectiveness of the management body, including numbers of independent directors, collective suitability and weak challenging culture

Weak IT landscape impairing data aggregation and reporting capability

Improvements to management body accounts for 32% of qualitative measures, risk and control functions (40%) and data (9%)

Credit risk

Positive credit developments but stable score due to the uncertain macroeconomic environment;

Persisting risk controls deficiencies;

Focus on credit risk controls and processes

Capital adequacy

Capital position improved, scores remained stable (92% of SSM banks kept their score).

Concerns relating to some banks’ ability to produce reliable capital projections, with 35% of qualitative measures focussed on ICAAP capital planning, 20% on risk aggregation, 9% on stress test.

Diversified lenders are the weakest business model with about 70% score 3 and 4.

Visit our Banking web page and get in touch with the team to learn more.

ECB’s Single Supervisory Mechanism will celebrate its 10th anniversary in November 2024 and since its inception, it has changed the ball game completely in the Eurozone. The SSM has become one of the most respected supervisors in the world. This is why it is important to take note of both the ratings it assigns to banks and of its updated priorities. We hope this blog article has helped you make sense of it all.