There is a famous phrase, well known to many: “When America sneezes, the world catches a cold,” speaking to the interconnectedness of the global economy, which entails ripple effects as a consequence of major shifts. Not unlike the COVID-19 pandemic, the current inflationary cycle has taken on a life of its own.

In this blog entry, we offer suggestions as to what measures CEOs should envision to deal with the current inflationary cycle all the while preparing themselves for future challenges.

We focus mostly on one element of the current economic cycle characterised by significant turbulence—inflation; a symptom that has proven to be surprisingly “sticky” and which CEOs need to contend with for a few more quarters or years to come.

This notion of vision & preparation is captured in the title of this year’s Annual Global CEO Survey—’Winning today’s race while running tomorrow’s’—an annual flagship exercise in which thousands of chief executives of major companies around the world take part.

Don’t have time to read the whole blog entry? Then watch our “Blog in 1 minute” video for a quick summary of its main points:

Now in its 26th year, the survey’s objective is to identify key trends and patterns in the global economy that affect the important management decisions the leaders of the business establishment have to make.

On 16 January 2023, when this year’s results were released, there were some jaw-dropping statistics. “Nearly three quarters (73%) of CEOs believe global economic growth will decline over the next 12 months according to the survey, which polled 4,410 CEOs in 105 countries and territories in October and November 2022.”

“The bleak CEO outlook is the most pessimistic CEOs have been regarding global economic growth since PwC began asking this question 12 years ago and is a significant departure from the optimistic outlooks of 2021 and 2022, when more than two-thirds (76% and 77%, respectively) thought economic growth would improve.”

Inflation, macroeconomic volatility and geopolitical conflict are dominant concerns

The impact of the economic downturn is at the top of the mind for CEOs this year, with inflation (40%) and macroeconomic volatility (31%) leading the risks weighing on CEOs in the short-term —the next 12 months—as well as over the next five years. Close behind, 25% of CEOs also feel exposed to geopolitical conflict risks, whereas cyber risks (20%) and climate change (14%) have fallen in relative terms.

That is not to say that cybersecurity and climate change are no longer relevant to the risk assessment of CEOs, rather, it speaks to the topical and pressing nature of inflation and macroeconomic volatility. For instance, analyses conducted by PwC’s Global AWM & ESG Market Research Centre show that Luxembourg CEOs from the financial centre view cybersecurity as a highly pressing concern, more so than their counterparts in other financial centres.

The enormous sentiment shift and the shifting priorities of our global client base beggar the question: how did things change so quickly?

Let’s go back to the famous sneeze and cold phrase. In the context in which it was spoken, it meant that because of America’s dominance, if something affected the US be it good or bad, it would have a knock-on effect for the rest of the world (remember Lehman Brothers?). But what the phrase in general terms means, is that if a powerful nation tips the apple-cart, it affects the rest of the world, be it for good or bad.

Do you know where this phrase comes from? Ironically, according to Culture Trip (and many other sources), it originally related to France. The first person to use the phrase was the aristocratic Prussian diplomat Klemens Wenzel Fürst von Metternich. Metternich was a diplomat during the Napoleonic era who is widely considered to be one of the most important statesmen and strategists of his time.

He is widely credited through his “balance of power” politics to have prevented war in the time of peace that came to be known as the “Age of Metternich” during which European powers managed to avoid engaging in wars that had plagued them throughout the 17th and 18th centuries. Unsurprisingly for the Napoleonic era, Metternich’s phrase was actually “when France sneezes, the whole of Europe catches a cold.”

Well, welcome to the age of *“polycrisis”, a concept that gained new life at the 2023 World Economic Forum, describing the interplay between the COVID-19 pandemic, the war in Ukraine and the energy, cost-of-living and climate crises.

Because now, in our interconnected global/glocal world, from whoever is sneezing, we all risk getting infected, and sneezes can occur for different reasons and from different points of origin. Just as the world started to emerge from the pandemic, we found ourselves amid war, post-pandemic disruptions to international trade as well as soaring food and fuel costs.

This means that events like COVID and the Ukraine invasion hit economies globally and start to make life more of a struggle for your hypothetical “average Joe”, John Q. Public – who we will rename Jean Q. Ëffentlech as he lives in Luxembourg.

Jean has a good job in Luxembourg. He and his partner, who hails from Lisbon, have been living together for about five years, saving to buy a house. But after suffering periods of isolation and home working during the pandemic, they feel an urge to travel back to Jean’s partner’s country of origin, lie on a beach and socialise with their friends, hosting dinner parties and going out to nightclubs.

But at the exact same time, their hard-earned savings are beginning to be eroded on multiple fronts. Their electricity bill has gone up, flights are more expensive (with less available services), cocktails are now 14 euros in town—rather than 10 euros on average pre-pandemic—and refuelling their car is no longer a trivial endeavour.

To make matters worse, the landlord intends to raise Jean’s rent, meaning he and his partner have less money for saving, and even worse, interest rates have gone up, so borrowing money for a mortgage will cost even more, all the while housing prices have skyrocketed.

When prices start to rise, it’s the people with the least money who get squeezed the hardest. As Bloomberg put it, The Inflation Crisis Pulls European Countries Into a Food Fight, even as inflation is starting to ease a bit, “…the upward pressure on food prices remains firmly in place. That means a large chunk of household spending, the weekly supermarket trip, is rapidly getting more and more expensive.”

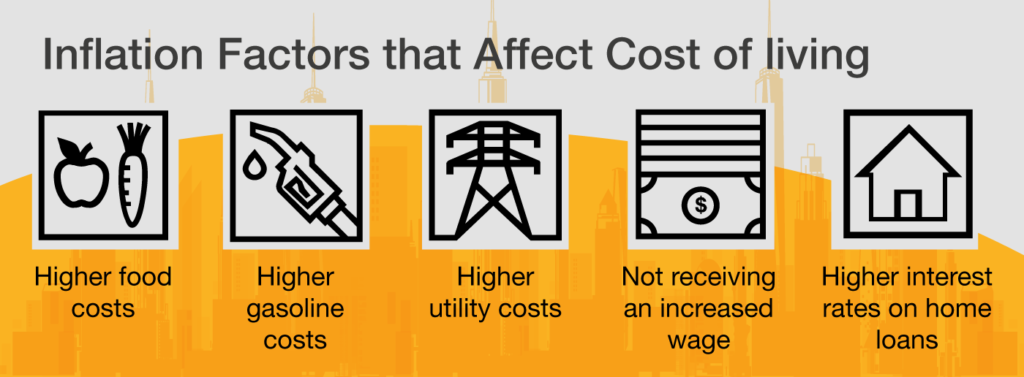

You have probably felt the crunch, but even if you personally haven’t, inflationary pressures are having far-ranging impacts on the average consumer and as a result, on almost every aspect of the growth factors driving our economies. Rising prices hit the middle-class hard, and the lower-paid even harder. Higher food, gasoline, and utility costs mean less money for savings or discretionary spending – not to mention investment.

To compensate, consumers buy less, switch to cheaper substitutes, or look harder for bargains. Maybe they won’t take a flight this year. Maybe they’ll rent for five more years or find a cheaper country to live in. Maybe they won’t go out for dinners or buy that new car; that is presuming they could even get their hands on the one they fancy as supply chain disruptions linked to microchips, which car manufacturers have become highly reliant upon, continue to delay deliveries. All of the above affects businesses and slows down the economy – it’s as simple as that.

How is the “inflation virus” spreading?

What are the main reasons for the current inflationary fever? Rising expenses lead to inflation, meaning consumers get less for their money. There is always some inflation, but not at the dizzying degrees seen in the last year. Recent research1 highlights the self-reinforcing effects of inflation and cautions that the monetary policy response to an out-of-control inflationary cycle needs to be swift and forceful2. Keeping this in mind, we list some top reasons for inflation globally below.

1. High demand

Following the pandemic, there was a resurgence in demand off the back of increased household savings and wealth. Just like our Jean Q. Ëffentlech, people were bristling to travel again, eat out, socialise with friends and shop. They wanted to buy new cars, remodel their homes, move and build.

This demand led to a lot of spending once the lockdown ended. Prices rise when there is scarcity and/or high demand for products or services. A corporation will seek to pass on the rising cost of raw materials, labour, or shipping costs to its customers. Companies will also charge more if they discover that customers are willingto pay more due to scarcity. We have observed all of the above materialise – 80% of respondents to our CEO survey indicated that they are, or are considering, raising prices on their products and services.

2. Supply chain disruption & China’s zero COVID policy

At the same time that consumer appetite spiked dramatically, there was a scarcity of all varieties of commodities due to pandemic-induced disruptions to international trade and to supply chains, which were exacerbated by the stringent 0-COVID policy in place for extended periods of time in the PRC (People’s Republic of China).

This increased the costs of raw materials, manufactured goods, and transportation, with affected businesses facing the painful choice of (partially) eating the costs or risking to lose out on prospective customers.

3. War in Ukraine

By impeding commerce in natural gas, oil, and grains, Russia’s aggression in Ukraine in February exacerbated the above-mentioned issues. Wheat, a mainstay in much of the world, has risen in price, as have the prices of natural gas, petroleum and many other commodities which are essential to the heating and cooling of homes, to the production of the synthetic fertilisers much of the world relies on to maintain crop yields or to fuel the global logistics chains which make international commerce possible.

As a first-order effect, this means that if wages do not keep pace, many people will be unable to commute to work, eat enough, or put up the thermostat in the autumn and winter. As a second-order effect, however, we risk entering into a perilous wage-price spiral.

Luxembourg CEOs told us how they feel….but what’s next?

This brings us to the local context. How can Luxembourg prepare to ensure that its economy is stable and sustainable? Here we envision sustainability in the fundamental sense of the word— –the ability for something to be maintained at a certain rate or level—that could very well be the key to taking on the crises to come.

Economic sustainability and stability will not only improve the life of Jean Q. Ëffentlech and his partner, it could enable them buy a house and to commit to our country in the long run, all the while incentivising more people from abroad to come to Luxembourg and contribute to the development of our economy by reducing the well-known talent shortage (read our blog A meaningful career journey takes more than just money which takes a very holistic look at this topic).

The 2023 edition of our Luxembourg CEO survey sought to provide insights on how business leaders are bracing for this new world with the increasingly interconnected macroeconomic, geopolitical and environmental challenges and threats, and how the Grand Duchy’s economy will be shaped in the near future. It’s worth giving the report a deep dive, but we can summarise the key take-aways for you as follows:

Sentiment has essentially flipped over the two-year period spanning the economic revival following the most acute phase of the COVID-19 pandemic to the late-2022 period of our current survey, characterised by major geopolitical and macroeconomic upheaval.

Inflation, macroeconomic volatility, and cybersecurity are among the key threats looming on Luxembourg CEOs’ horizons. Cybersecurity continues to be a pressing concern for our financial services (FS) heavy sample.

Structural imbalances in the Luxembourgish economy are starting to weigh heavily on CEOs’ minds, with FS respondents particularly worried about the long-term viability of their local operations.

Against the backdrop of their awareness of long-term challenges, Luxembourg CEOs are investing in resilience and transformation, leveraging existing USPs and moving into new (sustainable) areas of business.

Talent is a key issue in most countries but is seen as a bigger challenge in Luxembourg and more needs to be done by the public and the private sector to attract and retain critical talent in order to succeed.

Given such dramatic macroeconomic and geopolitical developments, it was unsurprising to see that Luxembourg CEOs are by and large uncertain and uneasy about the near future, with 78% expecting global economic growth to decline in the coming year, mirroring the views of their global counterparts.

Likewise, inflation and macroeconomic volatility are the key threats looming on Luxembourg CEOs’ horizons, with 41% and 34% seeing inflation as a key threat in the next 12 months and five years respectively, the highest figures among all threat categories. Responding to a separate question, 2/3rds of Luxembourg respondents indicate that increased costs are a “significant challenge” to their local operation.

Despite a difficult year marred by a confluence of crises, Luxembourg has held strong. In September, the Tripartite Coordination Committee—a core pillar of the Grand Duchy’s political and economic stability—formalised a landmark package to provide stability and meaningful support to households and businesses struggling with the cost-of-living crisis while supporting the green transition.

Public finances remain on a very strong footing, characterised by one of the lowest debt-to-GDP ratios in Europe, while leading credit ratings agencies continue to confer the coveted Triple-A on Luxembourg.

Alas, even if Luxembourg is proving to be resilient, the same cannot be said for the rest of the world. It would be no exaggeration to say that the global economy is entering a new era. Gone are the days of ‘free trade’ and multilateral cooperation that characterised the post-Cold War era. The decade of ultra-low interest rates that materialised following the Global Financial Crisis is also no more.

Today, in this proposed era of “polycrisis”, be it environmental crises triggered by ever-worsening climate change and extreme weather events, to societal crises driven by increased polarisation, socio-economic inequalities and involuntary migrations, our world is increasingly fragmented and fragile and has to be viewed through this new lens.

So what we need to do is look at this period of economic uncertainty and inflation and think of longer-term solutions so that we are not just treating the symptom(s). Ultimately, the conclusion is that this moment of uncertainty should not be a cause for despair, but rather a springboard to usher in a new way of thinking among leaders like Luxembourg CEOs, rooted in wider stakeholder collaboration which should lead to wider stakeholder benefit.

For example, ESG (Environmental, Social and Governance) presents a pivotal opportunity for CEOs in the financial and non-financial sectors to create value, attract investments and talented professionals, push the country’s green transition, and ultimately contribute to Luxembourg’s long-term socio-economic development. And if you cannot see the connection, just think of the reliance we still have on fossil fuels, and what a pivotal role energy has on our rising cost-of- living at the moment.

Simultaneously, today’s investments in technological transformation, upskilling and cybersecurity pave the way for tomorrow’s productivity gains and continued attractiveness of product offerings to customers. Luxembourg CEOs are bracing for the future by investing in priority areas and, given Luxembourg’s status as a pioneer in sustainable finance, stand in a strong position to decarbonise their activities and embark on a green transition.

As cliché as it sounds, there is opportunity to be found in crisis

As was highlighted in the previous edition of the CEO survey, there is significant untapped potential for businesses to more fully align with ESG principles and to innovate products and services that put sustainability front and centre. Furthermore, more fully aligning their businesses with sustainability goals could conceivably help leaders ease some of the aforementioned talent attraction and retention issues they are facing in Luxembourg.

Indeed, there is a growing expectation from young professionals that employers “walk the talk” in terms of sustainability, and hence firm-internal efforts to mitigate against climate-related risks, address societal issues or lead in areas of governance may lead to greater employee attraction and retention3. Although our CEO survey reveals that climate change and decarbonisation appear to be taking a back seat among Luxembourg CEOs’ priorities—which needs to be understood against the backdrop of the more pressing “polycrises” described earlier—as with digitalisation, there can be little doubt as to the long-term trajectory we need to embark on, speed bumps notwithstanding.

It would be an understatement to say that the transformations outlined above are complex and challenging. From the buy-in required within organisations and across functions to drive meaningful change in terms of digitalisation and sustainability alignment, to the difficulty of financing meaningful investments against the context of ongoing monetary tightening and inflationary pressures, there is a need for collaboration across the private and public sectors, but also with NGOs and stakeholders at large. Luxembourg respondents are particularly keen on doing so when it comes to sustainability-linked issues.

It goes without saying that this is an ongoing discussion as we all—both CEOs and we Jean Q. Ëffentlechs—weather through this storm and get over our collective infection. Disruption has become the norm, and a crisis is no longer a solitary event.

All this and more will be discussed at this year’s Journée de l’Economie 2023 under the theme of, ”The current geopolitical tsunami: How can Luxembourg’s and Europe’s economies stay stable and secure?” (We will be writing a blog post-event).

As Europe and Luxembourg weather a geopolitical tsunami, how can we ensure our economies stay stable and serene while upholding our values? Which levers can—and should—be used by governments and businesses today and in the near future? How can we ensure a sustainable future for Jean? These issues create concern for all citizens – regardless of their personal and professional situations, for organisations, companies and governments.

For Luxembourg, the proximity of decision-makers within the country, its multiculturalism and the inherently cross-border orientation of its businesses and a proven model for social dialogue leading to effective economic mitigating measures provide the Grand Duchy with a rather unique opportunity to implement the sort of collaborative efforts described above.

We believe that Luxembourg and its business leaders are provided with an opportunity to not only weather the storms of today but rather to seize the opportunity to invest, upskill and collaborate with a view on building the foundations for an ever more prosperous tomorrow. The unique structural selling propositions of Luxembourg remain for now, but it’s important that we work together on really delivering the Luxembourg value proposition and continuing to enhance what makes us great in an ever more competitive world if we want to remain successful.

Notes:

*The word polycrisis was first coined by the French theorist Edgar Morin, but has been since popularised by the historian Adam Tooze to describe the coming together of multiple crises. The word took on new importance at the 2023 World Economic Forum. You can read about it here.

**John Q. Public is a name for a hypothetical representative member of the general public, or the general public personified. The term John Q. Public was the name of a character created by Vaughn Shoemaker, an editorial cartoonist for the Chicago Daily News, in 1922.