Securitisation wants to polish its reputation, but the task is arduous and takes time.

Over the past few years, securitisation has become one of the funding and risk transfer methods that banks and other capital market players prefer. It also has the blessing of the European Commission in the context of the Capital Market Union. However, the hardest years of the global financial crisis at the end of the previous decade did a disservice to this sometimes complex financing structure.

To many, yet, the word “securitisation” reawakens the crisis ghost, one of the first hauntings of the XXI century. Is it, nevertheless, fair to blame it as the main cause of the crisis?

Securitisation has fought back. The Luxembourg securitisation market continues to grow steadily despite the general economic downturn and the (still) struggling reputation of its products. Indeed, Luxembourg securitisation vehicles are used in many structures in Asset Management, Private Equity or Real Estate so as to optimise investors’ benefits.

Both an attractive legal framework and legal environment have a lot to do with it. Earlier this year, we released the Securitisation PwC Market Survey 2020, an exercise in better understanding the underlying characteristics of the Luxembourg securitisation market. This article revisits the main conclusions of the survey and attempts to shed light on the near future under the current crisis triggered by the COVID-19 pandemic.

Decomplexing securitisation

Let’s revisit what securitisation is. Or, better yet, let’s explain it in such a way that every reader gets it clearly. We are aware it isn’t that easy to explain.

Securitisation is the process of converting an asset – loans, receivables, funds, stocks, bonds, mortgages and even car leases, credit card debt obligations and business loans – or a group of them, into a marketable security (a financial instrument that has monetary value and can be traded).

For banks (and other organisations such as credit unions) to fund themselves, they use deposits (yours or ours, for instance), raise debt on global capital markets and take advantage of securitisation. Yes, the latter allows them to raise funds by securitising their portfolio of loans.

The conversion occurs when banks or other so-called originators sell their portfolio (or “pool”) of loans to a special purpose vehicle (SPV). The SPV is usually an orphan entity created only for the purpose of isolating financial risk. When a portfolio of assets is securitised, liquidity is created in the market, which is positive. The SPV, in turn, has to raise the funds to be able to purchase the loans by issuing debt securities to investors.

Commonly, the securitised assets are divided into different “tranches” according to the investment risk tolerance of the different types of investors, and sold separately. For instance, pension funds could buy low-risk securities and hedge funds may purchase more risky ones.

Although any type of asset can be securitised, the most common have periodic and predictable cash flows, for instance, residential mortgages, whose irresponsible handling in the US was blamed for triggering the global financial crisis between 2007 and 2010. We revisit this matter later on.

The repayments from the portfolio of loans – a large majority of securitisations are amortised – determines the performance of the debt securities. The amount borrowed to buy, for instance, a property, is paid back gradually over the specified term of the loan.

Securitisation is a flexible, efficient and lower-cost way of raising capital. In Luxembourg, securitisation undertakings are governed by the Law of 22 March 2004.

Remember this!

When securitising an asset, its cash flows are transferred to third-party investors.

• All types of investors can use securitisation. The Luxembourg Securitisation Law does not limit the type of investors able to invest into a securitisation vehicle (SV).

• A Luxembourg securitisation vehicle can take the form of a fund or a company. The vast majority, however, are created as a company.

• The law defines securitisation vehicles as entities which carry out securitisation in its entirety or participate in such a transaction by assuming all or part of the securitised risks (the acquisition entities) or by issuing securities for the purpose of the financing thereof (the issuing entities).

• Securitisation funds have to be managed by a management company registered in Luxembourg.

For a full overview of securitisation in Luxembourg and the relevant regulation, visit this website.

Give a dog a bad [Securitisation] name and hang it”

Some time ago, the prestigious magazine, Time, published a list of the “25 People to Blame for the Financial Crisis”. To the main title, the publisher added this provoking sentence: “The good intentions, bad managers and greed behind the meltdown”. Among the names listed, and in a surprising 5th position, is the American consumers! Could we extend that to the rest of the world’s consumers? Certainly!

More than 10 years ago, in the United States, banks were granting a seizable number of the —today infamous—subprime mortgages, a type of loan granted to people with poor credit scores. This greatly affected the mortgage industry by 2008 because the borrowers finally couldn’t afford the loans.

In fact, the global financial crisis started as a US subprime crisis (mortgage and auto-loan markets) before it evolved into a global liquidity crisis and consequent recession.

To cover the demand for mortgage-backed securities, many of these subprime loans—most of them mortgages—were pulled together into securitisation vehicles and sold through secondary markets. When lenders couldn’t repay, banks, mutual funds, pension funds, insurance companies, and corporations who owned these securities suffered massive losses.

The securitisation vehicles that owned the subprime loans failed, causing a banking crisis that spread all over the world. The rest is history.

Which kind of risks are securitisable

In short, securitisation is a risk-transfer strategy. A bank or others transfer the ownership of loan portfolios to third-parties, in exchange for a lump-sum payment instead of installments.

All risks related to the holding of movable or immovable assets, as well as those risks resulting from obligations embarked upon by third parties or inherent to all or part of their activities may serve for securitisation purposes.

Hence, it’s possible to securitise assets such as shares, loans, subordinated or non-subordinated bonds, risks linked to claims (commercial and other), movable and immovable property (whether tangible or not), and ultimately any type of assets that have a real value or a future income.

The Securitisation Market Survey

By mid-May 2020, there were 1,288 securitisation vehicles representing around 7,000 compartments in Luxembourg, showing that the country remains a prime location for securitisation transactions in Europe.

Because securitisation vehicles aren’t legal forms per se, they have to be incorporated as a securitisation company or under the form of a securitisation fund managed by a management company that represents it before third parties.

The number of securitisation vehicles itself isn’t representative of the extent of securitisation transactions in Luxembourg. With the specificity of the Luxembourg Securitisation Law, allowing for the creation of compartments (ring-fenced subdivision of the securitisation undertaking), it is possible to have several securitisation transactions within one legal entity. This key characteristic is cost-efficient and can be set relatively quickly. In our PwC Market Survey 2020, Luxembourg market participants confirmed that the vast majority (76%) of the observed vehicles have multiple compartments, with around 10% having more than 50 active compartments.

Let’s have a look at key results of our Market Survey.

Servicing securitisation vehicles requires specific expertise and critical mass. To be economically viable, we observe that a securitisation needs to have total assets (sum of all compartments) of EUR 50-100M.

Most investors in securitisation vehicles are institutional. Banks and insurance companies/pension funds represent 60% of the investor base. This matches historical and European trends. The survey also revealed that there are 3% retail investors which we assumed to be engaged in the CSSF-supervised vehicles. In addition, we can see around one third of the money coming from family offices or private equity houses, i.e. more from the alternative investment side than from large financial institutions.

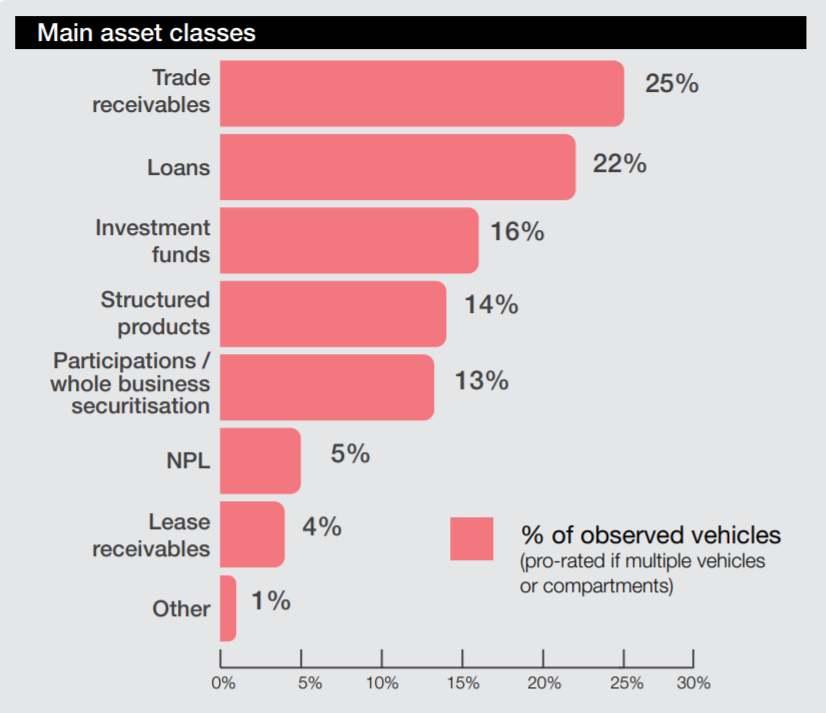

In terms of asset classes, about 29% of the vehicles described by our participants securitise trade or lease receivables. Another 27% focus on loan securitisation (incl. non-performing loans). Those more classic securitisations are complemented by typical Luxembourg products, namely investment fund and participation repackages (30%) as well as so-called structured products (14%). From our observation, most of the structured products issue on a regular basis and promise the performance of an index or basket to its noteholders which are often retail clients. Per se, they are often supervised by the CSSF.

The first key selling point for Luxembourg remains the dedicated securitisation law which is robust and flexible at the same time. An amendment of law, which is said to bring more flexibility, would probably be perceived even more positively. The second key element of Luxembourg is the legal possibility to create compartments and having key concepts like segregation of assets and limited recourse fixed in law and applicable on compartment level. Despite all discussions in Luxembourg and the world, tax is not the key driver to set-up a securitisation vehicle as per our survey.

Unfortunately, according to the respondents, the main obstacle to setting up a securitisation vehicle in Luxembourg is the still ongoing uncertainty about the interpretation of the interest limitation rules introduced in the Luxembourg tax law in 2019. All capital market participants are eagerly waiting for clarity from the Luxembourg tax authorities.

COVID-19 related crisis: impact on securitisation

Latest estimations highlight that the COVID-19 pandemic could result in one of the most severe crises in modern history. We estimate it will impact on:

Valuation of assets in general

Loans and receivables payment capabilities of individuals and businesses.

Treatment of government-permitted loan payment deferrals.

Services issues for non-performing loans or trade receivables structures

Margin calls under derivatives

Future amendments to transaction documents as a response to the crisis.

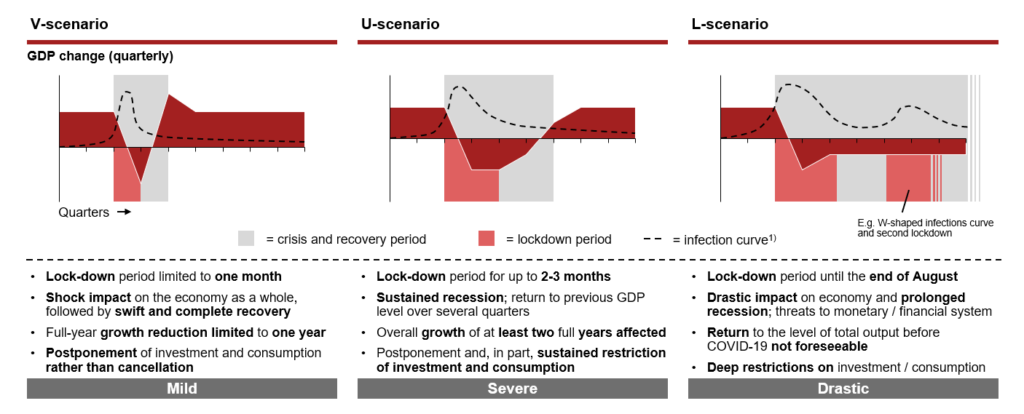

PwC’s Strategy& has run a scenario-analysis exercise to assess COVID-19 impact. It follows a Mild (V), Severe (U) and Drastic (L) rationale, based on the length of lockdown periods and their impact on investment and consumption.

COVID-19 scenarios – Economic foundation of the bank impact assessment;

At this point, most of the world is living in the U-scenario. Many industries have been severely impacted already by COVID-19, posing challenges for banks, particularly around asset quality.

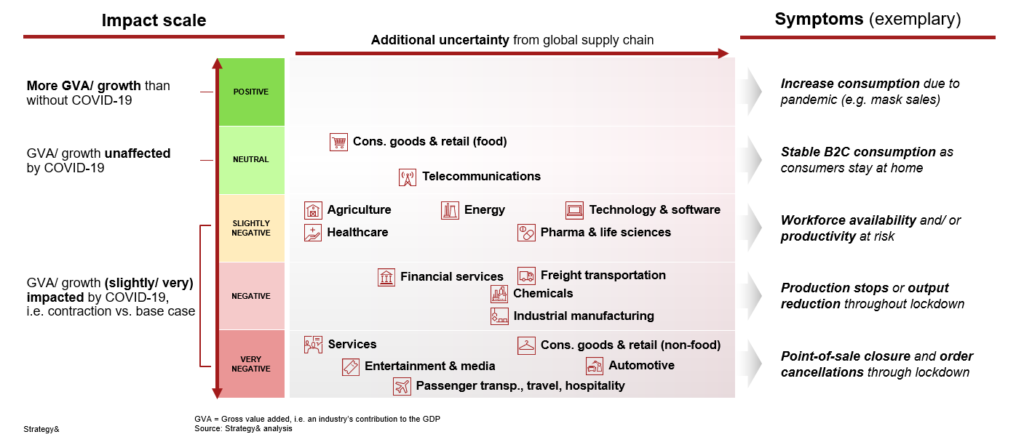

There have been disturbances to international supply chains causing medium-term production risk on top of severe demand contraction. Some non-essential services are facing longer-lasting lockdown restrictions (for instance professional services, in-person services, entertainment and media). Also, there is risk of workforce unavailability for manufacturing.

The impact on financial services as well as automotive, industrial manufacturing or services will be considerable. To assess industry recovery, our Strategy& colleagues used quantitative data from the 2007-08 global financial crisis and considered qualitative characteristics of each analysed industry. Although most industries will recover to pre COVID-19 crisis levels, the speed will vary. In the case of financial services, it will be “average” and will depend on loan portfolios and government support measures for clients.

What we think

Holger von Keutz, Securitisation Leader at PwC Luxembourg

Securitisation is an important technique to facilitating economic growth. What can greatly influence these advantages is undoubtedly a better understanding of this financial practice and, in general, of the structured finance and capital markets industry. It’s necessary to emphasise both the benefits and the potential pitfalls of securitisation, as well as to develop and quickly implement ideas for the future direction of the industry together.