The world becomes more connected. The digital economy comes of age through mobile technology, cloud computing, business intelligence and real time reporting. So, we see an increasing number of tax authorities and businesses around the world adopting or reforming their VAT compliance systems thanks to technological developments. We examined how VAT has spread all over the world and how technology can help businesses to comply.

VAT – the predominant consumption tax in the world

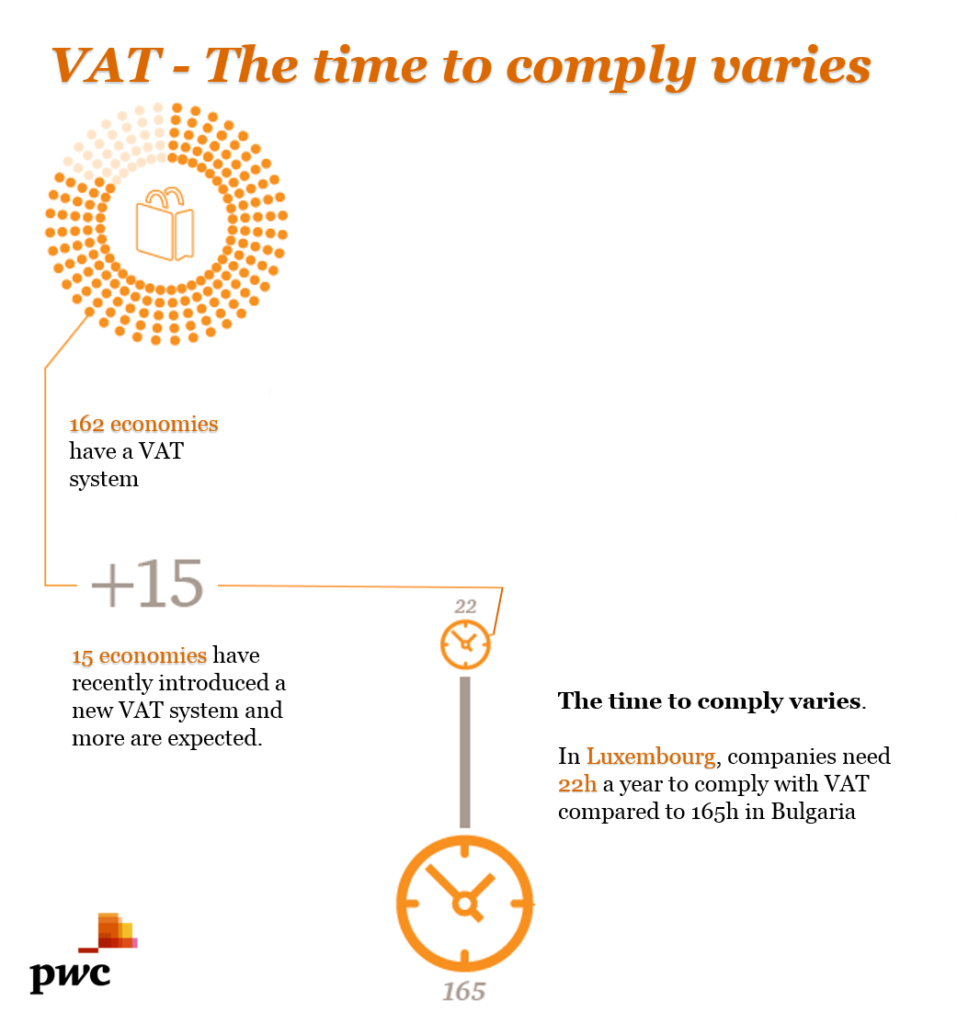

VAT is the most widespread form of consumption tax around the world with 162 economies having such a system. And, it continues to mainstream with more countries, including India and the Gulf States, introducing such systems within the next couple of years. The trend may be influenced by recent falls in corporate income tax as a percentage of governments’ total tax revenues. The resulting shift from direct to indirect tax brings fresh challenges for both governments and businesses. Indeed, each needing to adapt to make sure they have the right systems and resources available to comply with VAT requirements.

Stéphane Rinkin, VAT partner

The United Arab Emirates is the latest economy to implement VAT at the rate of 5% on 1 January 2018. It will help these governments to deliver on long-standing plans for economic diversification away from oil. It will also help them to deliver social and economic programmes. As VAT has immediate effects on consumer behaviour, it offers opportunities for companies to plan strategically.

How technology affect VAT compliance

VAT currently exists in several different forms across the world and has been implemented and reported on in different ways. This means that the administrative compliance burden varies hugely between countries. This can make it costly and time consuming for businesses to comply with the local requirements in the various countries in which they operate.

Tax authorities are increasingly implementing electronic reporting systems, including “realtime” transaction reporting systems. They are also requiring the use of electronic platforms to gather their financial data. Case in point: Luxembourg tax payers need to file their periodical and annual VAT returns on the eCDF platform. They may also need to provide structured electronic files for audit (files known as “FAIA” in Luxembourg).

So, businesses need to be familiar with an ever greater range of data collection solutions to manage the collection and payment of this tax as reporting obligations increase.

Frédéric Wersand, VAT Leader

We expect these trends to become more pronounced in the future. Indeed, governments increasingly use indirect taxation on consumption as a cost effective and more certain way to raise revenues. The advent of technological developments such as blockchain may allow tax authorities in the future to meet objectives that go beyond revenue-raising. This is due to the ability to deliver real-time, reliable information to a wide group of people. It also creates a system where taxpayers and tax authorities have equal confidence in the veracity of the data collected. Tax authorities in several countries see Blockchain as the next technology to collect tax information and identify risk patterns.

Today businesses have to contemplate verifying the accuracy of the VAT treatment of transactions as a real-time activity. This can move the compliance burden away from the completion and filing of returns to other parts of the process.

Greater efficiency and lower levels of fraud are driven not only by investment by governments in new digital systems, but also by updated accounting systems.

22 hours a year to comply with VAT in Luxembourg

According to The impact on business and howtechnologycan help, it takes roughly 106 hours for companies in the world to comply with VAT. A decade ago, it took them nearly 130 hours. This decrease is due to the implementation, expansion and improvement of online systems and of business IT solutions.

In the EU, VAT compliance generally takes longer if additional documents have to be filed with the VAT return. Indeed, extra records have to be maintained, additional analysis has to be performed, or separate VAT registers kept. The burden imposed by such requirements can be reduced if tasks can be automated using software which is trusted by taxpayers and tax authorities.

In Luxembourg, the survey shows that VAT return preparation activities (e.g. gathering accounting information for analysis and calculation of the tax liability) take just 16 hours on average (with differences based on the type of activities carried on by the taxpayer).

The level of trust that a business has in its software or systems may also affect the compliance approach.

According to The impact on business and how technology can help, it takes roughly 106 hours for companies in the world to comply with VAT. A decade ago, it took them nearly 130 hours. This decrease is due to the implementation, expansion and improvement of online systems and of business IT solutions.

According to The impact on business and how technology can help, it takes roughly 106 hours for companies in the world to comply with VAT. A decade ago, it took them nearly 130 hours. This decrease is due to the implementation, expansion and improvement of online systems and of business IT solutions.