This is more than an insurance story chock-a-block with buzzwords. They are there of course — data, artificial intelligence, customer experience— you will find them all, but combined in such a way that you’ll be willing to give them another chance, the one they deserve if we stopped overusing them.

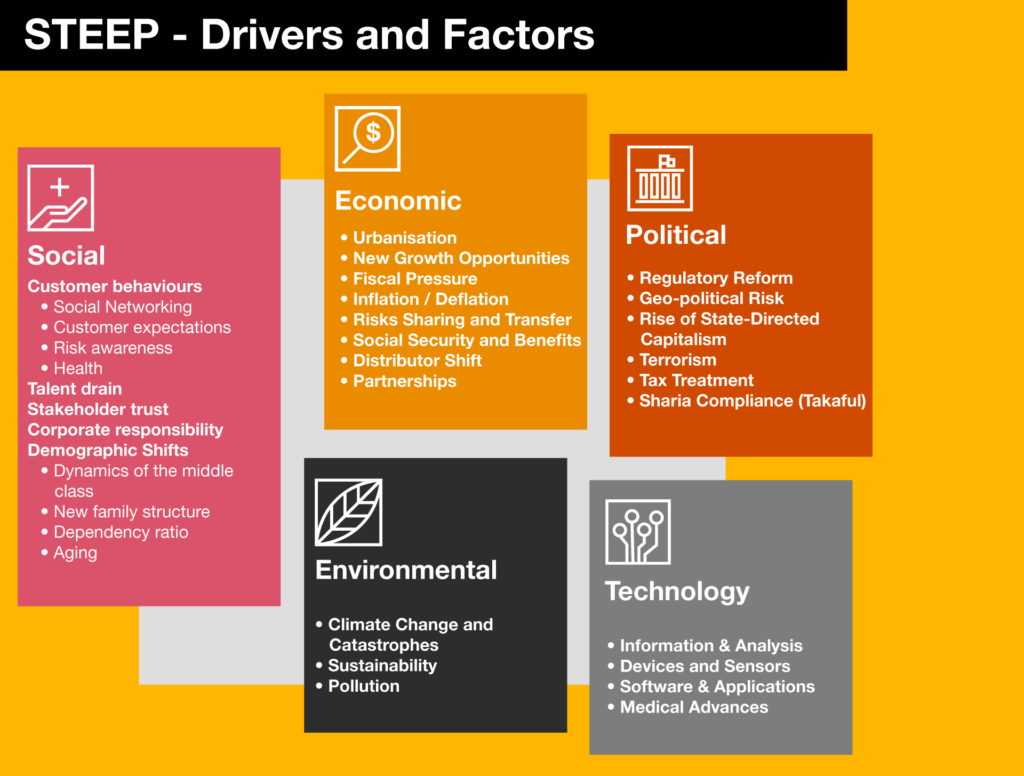

Five years ago, we released “Insurance 2020 and beyond: necessity is the mother of reinvention”, a mindful exercise to review some of the perspectives in the insurance industry we had originally put forward in 2012. Yes, the previous decade was done and dusted but the echoes of the financial crisis were very present in businesses, governments and people’s lives. Following a STEEP Analysis, our 2012 “Insurance 2020, turning Change into opportunity” evaluated the external forces that we thought were going to shape the insurance industry. Our goal was for organisations to assess the implications of the social, economic, environmental, political and technological trends and to determine their strategies needed to respond accordingly.

Insurance industry: Back to the future

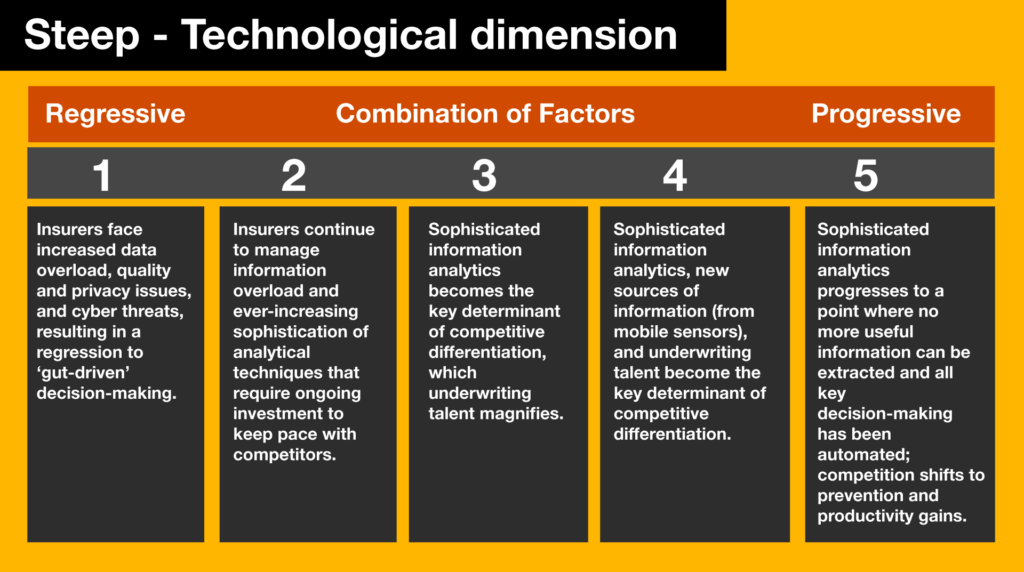

In this article, we revisit the technology aspect of the STEEP analysis, where we envisaged possible regressive and progressive scenarios.

About the most progressive scenarios, we stated:

Sophisticated, information analytics, new sources of information (from mobile sensors), and underwriting talent become the key determinant of competitive differentiation.

And we went one step further:

Sophisticated analytics progresses to a point where no more useful information can be extracted and all key decision-making has been automated; competition shifts to prevention and productivity gains.

An agile scrutiny of the current state of the insurance industry—putting online trends, content, conversations with experts, conferences and team discussions all together—tells us we’re living the first scenario. To some, and that can be valid too, current technology trends within the insurance industry are somewhere between scenario one and scenario two.

Something caught our attention when reviewing the two aforementioned publications. Neither “fintech”, nor “insurtech” or “regtech” were mentioned in the nearly 50 written pages. It wasn’t a conscious act of exclusion or lack of oversight but technologies behind fintech were only taking off. And this was only a short time ago.

We are all riding the rollercoaster of digital and, in tech terms, eight years can be raised to the power of 3. Because, and we likely agree on this, most technological advances that have experienced great acceleration in the last decade are linked to bytes and algorithms, and tons of data.

As contemporary witnesses with the advantage of being able to see how technology is evolving now—artificial intelligence, the internet of things, quantum computing, distributed ledgers, etc.—in this article we take the 2012 scenarios to outline a path towards what’s to come in the near future in the insurance industry.

Before digging in, we can’t lie, if you have your buzzword-bingo cards at the ready you will probably be yelling “BINGO” before you get to the end of the article. But here, we give buzzwords the meaning they started out with. So, let’s get started!

The insurance future in one sentence

What the future of the insurance industry looks like is contained in exactly 9 words or 54 letters:

The ability to provide digital, flexible and “personalised” products.

Nothing cabalistic about it. Simply common sense, a logical consequence of what’s surrounding us. To that we can add a second explanatory idea:

Commonly, it will take the shape of platforms, emulating those that have helped the world’s most valuable companies arise and succeed.

Personalisation translated, for instance, into user-friendly platforms, needs to be fed by a source that we can consider the glucose of the digital revolution: data. When data is missing, personalisation, in the way we are used to experiencing it in this century, is difficult to achieve.

It’s data that algorithms are addicted to. And it’s an algorithm, or a set of them, that power artificial intelligence in a computing system, or a platform. And it’s several computing systems that make artificial neural networks and deep learning possible.

One of the turning-point factors that’s demanding an urgent technology-driven change in the insurance industry, is the amount of information available and the systems that can process it, analyse it and make decisions. And most certainly, a growing number of clients, both on the retail and corporate sides, are asking for an experience that resembles the one Amazon or Netflix have gotten almost everyone used to.

There is another turning-point that has also to do with large amounts of data that will soon ask policy makers to rethink insurance: autonomous artifacts and in particular, autonomous vehicles.

Is it data or big data that feeds most of the digital technology?

Once upon a time, big data was smaller than what it is now. Currently, 1 petabyte (10¹⁵) of data is considered as big data. But 30 years ago, even 5GB could have fitted in the definition.

Therefore, strictly speaking, what we considered big data today will be just data, let’s say, in five years time. The definition of big data will evolve as the need to feed complex systems with very large amounts of data—smart cities, for instance—will grow.

Depicting the old and new insurance players in 14 bullet points

When one reads about the old times of financial services, a certain contemporary attitude perceivable between lines that saddles with the blame of inaction, of resistance to change. Whilst there is a certain responsibility for not having paid enough attention to what clients and markets have been asking for—such as renewed, smooth and digitalised experiences, more attention to sustainability, amongst others—the financial services industry hasn’t walked along smooth paths in the last 10 years.

First, there was the 2008 financial crisis. Next, the complexity of the regulatory measurements that followed. Then, the technology revolution that reached new heights, and then, the uncertainty—political and economical—that is being felt nowadays even stronger than before. That’s what’s clearly reflected on this year’s CEO Survey.

Grosso modo, a classic insurer:

Offers a full range of products, and stability,

Follows slow processes, frequently non-digitised,

Organises the business in disconnected silos where data isn’t accessible across the organisation and the technology approach isn’t orchestrated,

Embraces digital commonly using the Digitise-front-end-only Model, for instance, by putting together an app for the end user to interact with the business.

Contrasting that reality, aninsurtech – a subset of fintech:

Offers a limited set of products in an agile and personalised manner. To an insurtech business, one-size-doesn’t-fit-all.

Collects and analyses customer data to run behavioral analysis and propose tailored solutions to clients (customer intelligence). The data mostly comes from internet-enabled devices—chatbots, smartphone apps and wearables,

Follows a startup-like way of working, with fast decision making, agile processes, and the trial-and-error mindset,

Empowers customers to take control of their insurance

Many illustrate the classic insurer-insurtech coexistence as conflictive, like a winner-takes-all affair. Doubtlessly, there will be extinction and evolution in both traditional insurers and insurtechs, but the opportunities that teaming up bring can make them stronger and give them a chance to remain and thrive in this accelerate-or-fade present where deceleration doesn’t seem to have a chance any time soon.

That takes us to imagining a future with incumtechs—please allow us to use this neologism for the sake of comprehension. It is, simply put, traditional insurance companies embracing digital in the broadest sense, but also insurtechs becoming mature, in the context of a regulatory framework that has taken into account the nuances that technological advancements bring out.

An insurance incumtech, therefore:

Is primarily technology and data-driven. This, as a consequence, helps it bring about highly specialised products and reduce risks.

Calls, necessarily, for a commitment to customer centricity which, in turn, has compelled them to go un-siloed.

Has adopted agile as a philosophy and uses one or more of its methodologies (Scrum, Kanban, etc). However, other traditional approaches to project management such as waterfall aren’t left behind and are purposely used when necessary.

Uses machine learning—an application of artificial intelligence, to manage and reduce risks and create customised policies. This is powered by the use of historical data.

Takes advantage of platforms to interact with clients. For instance, it uses chatbots, automated claim handling, live video chats for guided damage reports, augmented reality for client education, etc.

Has embraced the power of neural networks for fraud detection.

Artificial neural networks in insurance

Fraud techniques are ever-evolving. Criminals are first movers when it comes to adopting new technologies or testing new tactics to commit fraud. They want their trace to be untraceable so patterns they follow are non-linear and more and more sophisticated.

Artificial neural network applications are proving to be valuable allies to detect fraud. This advanced form of artificial intelligence—a computational model based on the structure and functions of biological neural networks— is adaptive and able to learn from non-linear behavioral patterns to predict future conducts. They are extremely fast, and decision-making happens in real time.

The legacy shells

Technology isn’t the answer to the insurance industry’s crusade of this century. It’s only the means. If you have gone down the road until now, you know that the most difficult battles are faceless, the ones we fight against ourselves.

Insurers have no stronger enemy than the legacy shells than want to remain unbreakable. That reluctance is understandable after all, because, when learnt ways of doing things—organisational, operational, model-related, financial-related, etc. go away—a part of us fades with them.

Far from being only technological, the insurance industry also wants decision-making, execution, working practices and talent development to be different, so it can speak the same language of the new generations and accelerate at a similar speed the present does.

New insurance models, using customer intelligence, are changing the relationship with clients. Policies are becoming more flexible, products resonate better with consumer needs, interactions are becoming seamless and more fluid. The old, sometimes monumental insurance branch has taken the shape of a simple, graceful and hierarchy-free platform or mobile app.

You, as a client, are enjoying this new insurance too.

By the way, we have used them all.

Artificial beyond the buzz, won’t you please give them another chance?

What we think

In another 9 words from our Insurance Industry Leader, it’s all about:

Matt Moran, Partner & Insurance Industry Leader at PwC Luxembourg

Lowering the cost-to-serve whilst enhancing customer experience. Partnering together advances this mission.