Yes, we are moving more and more towards a cashless society. But what does that mean for banks?

Underneath the shift to cashless lies a larger, more profound change. Not only are traditional ways of paying for goods and services — including the humble paper check and analogue invoices — set for radical transformation, but the entire infrastructure of payments is being reshaped, with new business models emerging.

Understanding today’s payments’ landscape…

Don’t have time to read the whole blog entry? Then watch our “Blog in 1 minute” video for a quick summary of its main points:

Whirlpools of change—technological developments and a changing regulatory environment, not to mention shifts in consumer habits, the rise of disruptors and current geopolitical tensions—swirl around the financial services industry. Consumers want it now, they want it simple and at their convenience; this is revolutionary and evolutionary change.

Given the key role digitisation plays in the financial lives of more and more of the world’s population, electronic payments are a big part of this transformational push as we move towards a cashless society. For banks, this will require evolving swiftly and sufficiently enough to respond to this reshaping of the payments world.

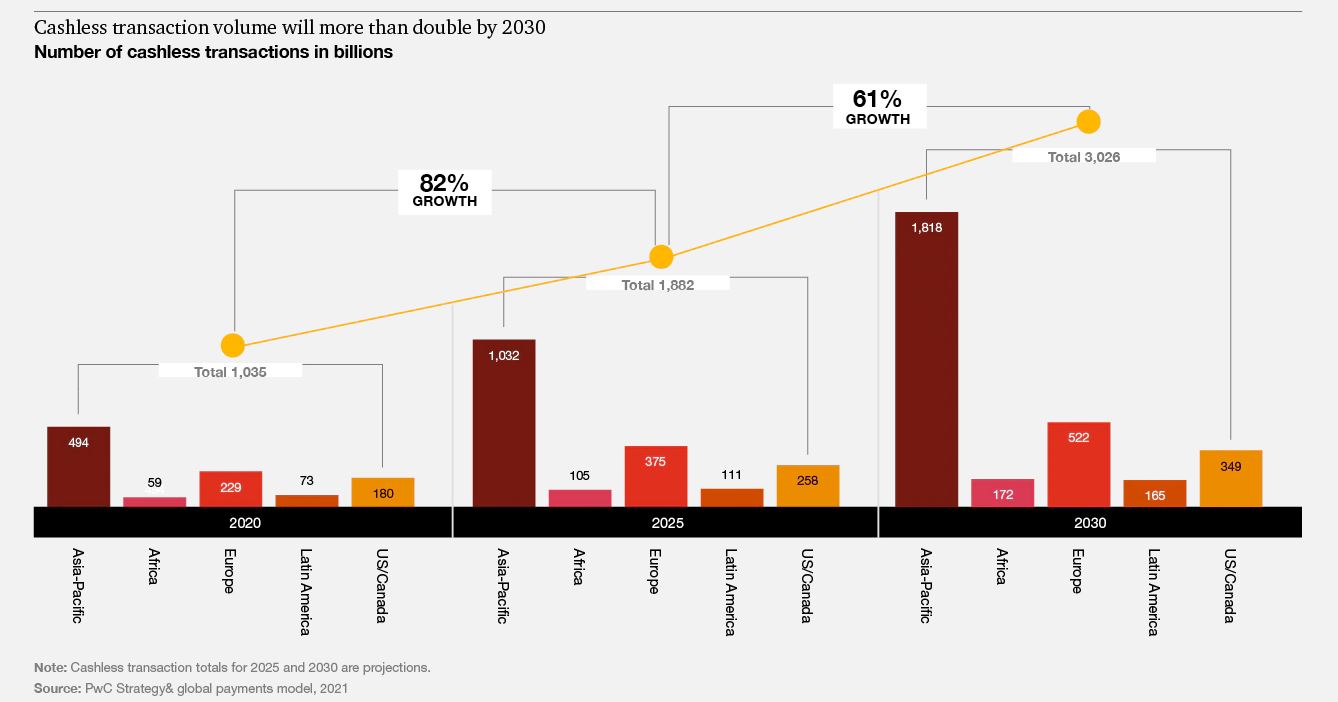

“Global Cashless payment volumes will almost triple by 2030”

Click to enlarge | Source: PwC Strategy& global payments model, 2021

In a recently published PwC survey, which focussed on the payments industry and the key trends — Payments 2025 & beyond, navigating the payments matrix and charting a course amid evolution and revolution — the extent of this sea change is clearly evident in the responses.

How the banking industry responds to these trends will define how successful it is in the coming years and its impact on society overall. The results from the respondents were very revealing as to which direction the future of payments is heading.

42% see an increase in global cashless payment volumes

89% agreed that the shift towards e-commerce would continue to increase

90% of banks’ useful customer data comes from payments

42% felt strongly that there would be an acceleration of cross-border, cross-currency instant and B2B payments

86% agreed that traditional payments providers will collaborate with fintechs and technology providers as one of their main sources of innovation

The challenge that banks have to overcome is the fact that payments are now embedded in the real world economy. As business and customers’ needs evolve, the payments ecosystem has to be agile and innovative.

This will require a “reshaping” involving two parallel trends: an evolution of the front- and back-end parts of the payment system like Swift GPI; and a revolution involving huge structural changes to the payment mix and ecosystem (emergence of so-called “buy now, pay later” offerings; cryptocurrencies; and central bank digital currencies).

Both evolution and revolution are sweeping the globe, but in different ways and at different paces, creating a complex payments matrix. Many organisations are trying to figure out where to play —and win— in that matrix.

On top of those, other macro trends play a role in the payment ecosystem transformation. To name some of them, we can list the trending embedded finance concept, the emerging SuperApps for digital natives, and from a corporate point of view, the move towards treasury on demand.

So payments are evolving, expectations from the buy side are also evolving and new players are entering the game. Did we mention that today, payments represent a key source of profitability and an amazing source of interactions with clients as well as useful data for our banks?

Banks have a long history with payments —indeed, they were a main source of income and a main competency. This source of activity, however, has been eroded in recent years by the rise of payment giants and rising fintechs, who can offer a wider range of services, such as installments, financial products, rewards or other services.

The way to pay now needs to appeal to the changing behaviour of the customer who wants convenience, and the advantage to the payment company is that in the digital age it gains in the use of data and its monetisation.

In addition, regulatory initiatives such as the 2nd Payment services (PSD 2) have further advanced the digital transformation of payments by enhancing consumer data protection and payment security, while the emergence of smart technologies stand to completely upturn how banks serve their corporate and institutional clients in a B2B payments sphere.

Preparing for tomorrow…

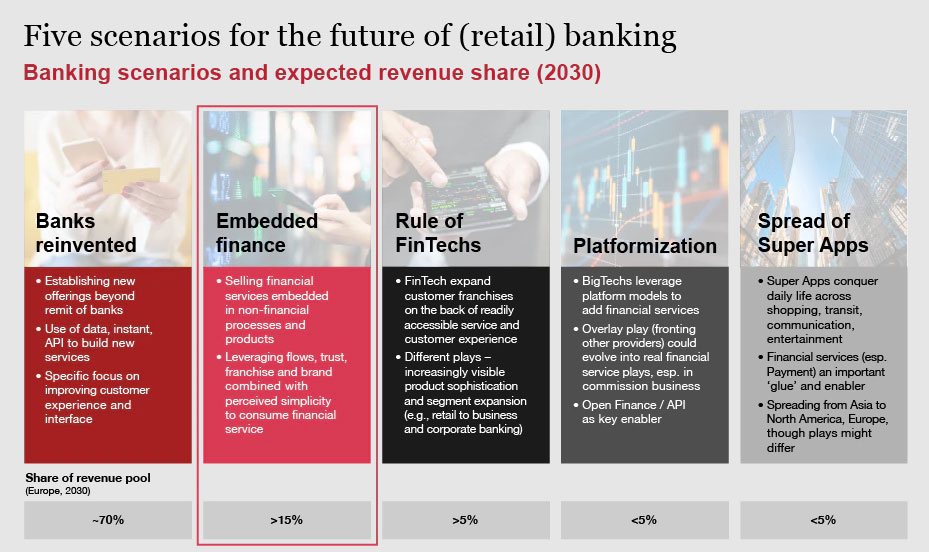

In a recent Strategy& article entitled, 2022 Retail Banking Monitor: Repositioning for embedded finance, they explain five scenarios for the future of (retail) banking, with a priority placed on embedded finance. Making the latter an integral part of the user experience is just one of the challenges banks (in this case retail) will have to prepare for.

Click to enlarge| Source: https://www.strategyand.pwc.com/de/en/industries/financial-services/embedded-finance.html

Using a structured way to think about organisation, operating platform and overall business is certainly helpful. At PwC, as part of our Future of Industries project, we determined the four key categories and areas of focus to consider when preparing for tomorrow: Repairing the damage, Rethinking the organisation, Reconfiguring the business and operating platform, and Reporting the results.

Using this methodology, banks can plan for success by taking the following actions to determine their gaps and priorities:

Repair

Banks want to prevent credit risks, provide payment holidays when necessary to secure future cash collection and, to some extent, adjust pricing of some services.

Limiting free offerings (cash withdrawals, checking accounts) and reducing remote service costs (through enhanced customer self-service options for example) have to be considered as well.

Rethink

They may consider whether it’s worth competing at all (especially if a midsize bank), given global player dominance in some aspects.

The value of their data and the role they can play with the open banking landscape may be a differentiating factor. Combining the data from banks with the power of tech companies could lead to a fantastic customer experience —let’s mention cash forecasting, for example.

Collaboration with (Fin)tech and / or other banks is clearly a key theme to rethink.

Reconfigure

They may wish to expand into new offerings, including ‘buy now, pay later,’ cryptocurrencies and central bank digital currencies, for example. Or one more time partner to build joint offerings with nontraditional players (fintechs, big tech).

Banks need to work with business customers to help them integrate payments into their services directly. This will help them deal with a world in which increasingly multifunctional digital wallets and super-apps are proliferating. Bill payments and request-to-pay or instant cross-border offerings could provide opportunities for some larger banks.

Report

In a world where transparency and trust are key pillars of business relationships, banks want to inform customers of the benefits of payment solutions to their businesses and wider society. They should as well report on future roles for payment services inside the bank. More broadly, they should ensure a clear strategy and a clear communication around that strategy.

Last words

We need to acknowledge that it’s pretty much impossible to list all challenges and opportunities banks are facing around payments in an article, so let’s be humble; these are just a few lines to initiate the debate for the latest ones. Because, of course, banks have started the journey and some are even really well advanced in this exercise, but… As they say in French, “Il y a encore du pain sur la planche” (But there is still more to do).

What we think

Philippe Förster, Partner at PwC Luxembourg, IFRS, Treasury & Payment institutions

To survive and thrive amid these changing market dynamics, banks must accelerate their digitisation journeys, with modern technology capabilities. Collaboration is probably key.