Corporate banking is growing in importance to not only Luxembourg’s economy but also to ensure a successful future for the banking sector. Corporate banks need to differentiate themselves and generate real value and that translates into responding to increasing challenges such as cost discipline, related to end-to-end process streamlining, for example, and adapting to disruptive technologies such as artificial intelligence, cloud computing and data analytics.

The growing demand for digital transformation in the banking industry has been slowly changing the way banks function and operate. As the COVID-19 crisis and its aftermath continue to influence the global economy and all markets, the need for this transformation has accelerated at a pace never seen before.

To succeed in the post-pandemic world, businesses need a supportive and reliable banking environment, one that offers not only a secure and transparent relationship but also a wide range of services, tailored to both business and shareholders’ needs. They need to reinvent the experience throughout the entire customer journey and develop business models that better fit the specific needs of their corporate clients. Do the digital capabilities need to be recalibrated? Is the product offering the right one to support the clients’ futures?

In this article, we go for a broad overview of what is corporate banking, the opportunities and challenges that come with the development of this specialised division of a commercial bank, and how Luxembourg is in a privileged position to be a major player in the corporate banking market.

How do we define corporate banking?

To put it simply, corporate banking is a custom-tailored banking and financing services for corporations. It involves all the services that can be extended on a financial level to businesses (from large corporations to SMEs) to facilitate daily tasks and activities and, therefore, help them accomplish short- and long-term goals.

Corporate banks services offer an array of secure and timely services to support corporate financial requirements. Public institutions and governments can also benefit from this type of banking.

Credit, such as loan operations and related credit products that are usually part of the largest share of profits for commercial banks.

Treasury services, used to manage working capital requirements—the amount of money needed to finance the gap between disbursements such as payments to suppliers and receipts (payments from customers).

Fixed asset requirement financing, through which banks can facilitate loans and lease agreements.

Employer services, providing an array of healthcare and retirement plans.

Commercial services, like asset management, cash flow management, investments, securities and equities management, risk management, payments, and trade finance.

With this array of services, banks are in an enviable position of providing efficient and end-to-end solutions for corporations to be better equipped to reach goals and respond to client needs.

At the same time, corporate banking is important for the economy because it fuels profit.

Indeed, corporate banking might just become one of the highest sources of profits for banks. This is due to the fact that banks work with corporates with large working capital. Corporate banking provides large sums of money at a higher rate of interest compared to regular loans.

What are the opportunities and challenges of corporate banking?

Corporate banking players have the potential to offer a handful of key services to corporate customers and differentiate themselves from the competition, from reinventing customer experience by means of a balanced mix of digital and in-person services to developing new business models that answer internal and stakeholders’ needs.

How? For example, by finding the right balance between in-person interactions and accessible, intuitive and purposeful online tools so account managers can concentrate on the essentials; or by going mobile, allowing customers to access several critical services without having to call or interact directly with a bank.

Much as in other industries, corporate banking customers are looking for efficiency and convenience, searching for experiences similar to those offered by retail websites like Amazon and Netflix, a trend that only grew in 2020 due to the global pandemic.

Keeping up with technological and digital developments is crucial for banks that don’t want to be left behind in the market, particularly in the current and post-pandemic world. Slowness in introducing new digital technologies and adopting them (for clients, back-office, front-office, etc) remains one of the main challenges for corporate banks.

The demand for personalised and tailored services is growing among banks’ clients. And while most retail banks, both in Luxembourg and Europe, are in the process of implementing new technologies –such as facial and voice recognition, bots, artificial intelligence– and expanding their digital presence, corporate banks are still struggling to keep up. Many still rely on manual processes, calls and emails alone to interact with clients, and they still gather documents cumbersomely.

Corporate banks have to deal with not only a large portfolio of services but also with the growing need for tailored solutions for individual corporate customers. The process of client identity verification (KYC), preventing money laundering, complying with local and European regulations, performing credit analysis and credit risk management, these are all highly complex processes. And the cost of failure includes compliance breaches and the loss of key clients to the competition.

The slowness in the adoption of digital technologies might be even more costly in the long-term. To go about it, corporate banks in Luxembourg need to do more than just create and implement a new user interface or a new digital tool. They need to re-think and re-invent their customer journey, focusing on solving their clients’ key pain points, and helping them overcome internal challenges. They’ll also need to support these journeys by optimising their business processes from end to end, integrating digital tools throughout.

Simply put, corporate banks will need to go beyond the surface and become more active in helping customers overcome internal challenges.

Additional pressure with COVID-19

The global pandemic has set new challenges for all industries, both in Luxembourg and in Europe. Corporate banking isn’t the exception. Boosted by the COVID-19 crisis, previous challenges became more urgent to solve andnew ones came into play, mainly when it comes to:

The existing business model and if it’s robust enough to withstand the post-health crisis.

How portfolios should shift in terms of sustainability, clients’ interests and needs, and industries to serve.

Recalibrating the banks’ digital transformation efforts to support the overarching goals.

Whether the current product offering supports the future.

The possible strategic pathways that open up in light of the COVID-19 crisis.

The banks’ fund basis going forward.

How banks can support their teams in this transition.

In order to deal with these challenges, corporate banks will need to tick a few boxes in key areas early on.

Winning through the crisis requires achievements in key areas early on

In Luxembourg, the situation for banks has been rocky, to say the least, during last year. According to the latest CSSF report, the banking sector’s annual result (profit and loss account of credit institutions) fell by 18.1% due to the increase in the additions to provisions of 600 million euros, compared with 2019. These provisions are predominantly related to credit risk in the context of the COVID-19 pandemic, and mainly impact universal banks and banks specialising in corporate finance.

Corporate banking in Luxembourg

Give or take, the banking sector represents roughly half of Luxembourg’s financial sector.

The Grand-Duchy has the highest banking internationalisation rate in Europe, with 94% of banks being foreign, and more than one third being from outside the European Union.

Its strong and stable market and diversified ecosystem has made the establishment of new banks much easier, including seven of the largest Chinese banks and several UK banks and institutions that choose Luxembourg as a post-Brexit hub.

We can’t forget that Luxembourg is also taking full advantage of its unique strengths, mainly as a leader in innovative financial technologies, with a close collaboration between fintechs and financial institutions. In sustainable finance, the country is building up a leading positioning worldwide and hosting half of the global green bonds issued. It also gives room to an open and transparent dialogue between relevant market players (private, public and supervisory).

The Grand-Duchy is pushing the boundaries by exploring new and advanced solutions in the banking sector, and an innovative development of its corporate banking industry can be a promising opportunity to stand out in the European and international markets.

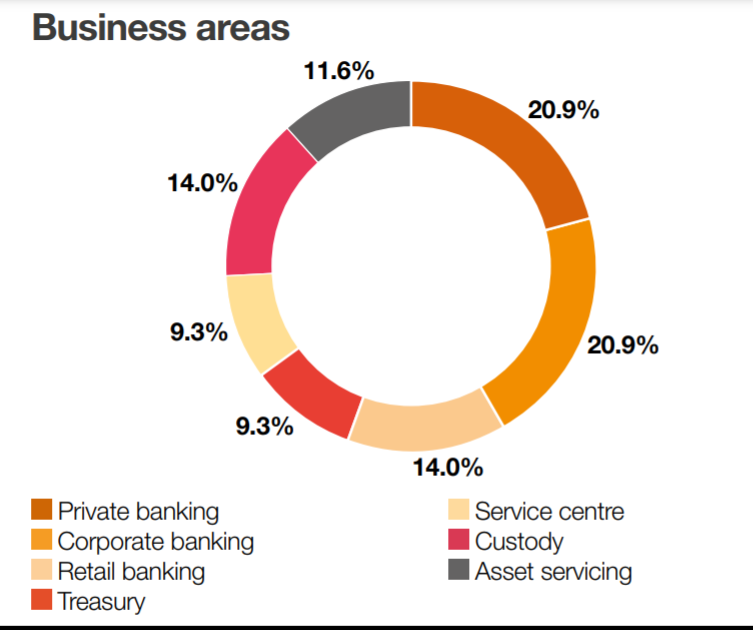

According to this Luxembourg Finance publication, corporate banking drove up its value added with an increase from EUR 1.3bn in 2011 to EUR 3.4bn in 2018. What instigates this growth is the attractiveness of the legal, regulatory and economic environment of Luxembourg. At the same time, corporate banking occupies second place, only overtaken by private banking in the Luxembourg banking business areas.

But for all its potential, there’s still much we don’t know about the full reality of corporate banking in Luxembourg. While the chart above depicts a clear view of the services corporate banks provide, the state of the market itself, its gains and pain points are still a mystery. Even so, there are opportunities and challenges in this niche market that is corporate banking.

In conclusion

Corporate banking can be the hidden jewel in Luxembourg’s financial industry. The country offers a unique stability, security and an international environment that pushes for the adaption of new banking business models and processes and even the creation of new ones to match the needs of both banks and customers alike.

However, there’s much to be discovered when it comes to corporate banking in Luxembourg. Most of the information available is focused on the services provided by corporate banks and not the state of the industry itself.

Conducting a corporate banking survey is the answer to finding out more about the subject in Luxembourg, a project that is already ongoing between PwC and other banking and supervisorinary institutions.

What we think

Daniel Theobald, Senior Manager, Banking Advisory at PwC Luxembourg

Although corporate banking has been around for a while, its full potential in locations such as Luxembourg is yet to be seen. To the strategic location of the country, one can add the extensive financial services expertise and the diversity of the country. This combo could propel Luxembourg as a corporate banking hub. But digitalisation, on the one hand, and customisation of services, on the other, are two of major endeavors Luxembourg’s banks offering corporate banking services are called to commit to. We need more information to draw a detailed map of corporate banking in the Grand Duchy so we can plan accordingly and more strategically. We’re working on that.

Jörg Ackermann, Partner at PwC Luxembourg

The global demand for corporate banking has only grown in recent years, and it will continue to do so. Luxembourg has all the potential to stand out in this banking niche, much like it has done when it comes to Sustainable Finance. A sound study on the state and trends of corporate banking in Luxembourg is a good place to start.