Today, the entire banking sector represents half of Luxembourg’s financial services market. However, between 2010 and 2020, the number of banks operating in Luxembourg decreased from 147 to 128, which translated into a decline in net results from EUR 3.8mn to EUR 3m.

Yet, when looking at the corporate banking sector, we see a different picture. According to Luxembourg for Finance (LFF), this segment experienced an exponential increase in value from EUR 1.3bn in 2011 to EUR 3.4bn in 2018.

Don’t have time to read the whole blog entry? Then watch our “Blog in 1 minute” video for a quick summary of its main points:

This growth shows — and as mentioned in a previous blog — that Luxembourg is in a privileged position to be a major player in the corporate banking market. Hence, no wonder we like to say this sector is the hidden jewel of Luxembourg’s banking industry.

Needless to mention, jewels are precious and can be difficult to find. That’s why rarity and notoriety are usually two characteristics that lend value to gemstones. When you find one, you may not grasp its worth until you ask the gemologist to evaluate it in depth. That was exactly the case with corporate banking.

While the Luxembourg banking industry has been aware of all its potential, it has taken more than 50 years for it to notice the scarcity of studies about what is considered one of its most important segments. The developments, challenges, and opportunities of the past few years made this lack of information all the more prominent and urgent to address.

As with any gemstone, if you want to use it to make jewellery or other adornments, you need first to cut and polish it. And so to do that conducting a survey became imperative.

This blog entry examines the main results of the Corporate Banking Survey 2022, a collaboration between PwC Luxembourg and the Association des Banques et Banquiers Luxembourg, with the support of the Commission de Surveillance du Secteur Financier (CSSF) and Luxembourg for Finance (LFF).

The survey takes a closer look at the state of the corporate banking segment with the aim to find out more about the market itself, and its current and future opportunities and challenges, as well as to map out a clear path for enhancing Luxembourg’s competitiveness in this banking segment.

A strong and profitable sector

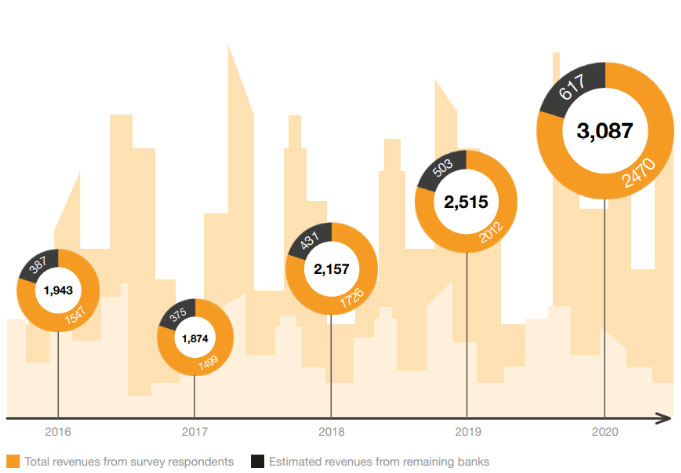

According to the latest numbers, corporate banks in Luxembourg attained around EUR 3bn in revenues as of end-2020. The major contributors to growth were financing products and interest-based business. Moreover, multinational companies remain central to banks’ business, and non-financial institutions represent a key client segment.

The total corporate banking revenues from survey’s respondents hit almost EUR 2.5bn as of end-2020. Taking into account that they represent about 80% of the entire corporate banking market in Luxembourg, it’s possible to extrapolate total revenues for the entire corporate banking sector — approximately EUR 3bn, 59% more than in 2016.

This figure comprises 27% of total revenues for Luxembourg’s banking sector, which reached EUR 11.1bn in the same period, and exceeded the private banking sector revenues, which stood at EUR 2.2bn in 2020.

When it comes to profit margins, there’s a similar growth path, with corporate banking profits increasing by 37%, from EUR 832.4mn in 2016 to hit EUR 1.1bn in 2020. It’s undeniable that, due to the customarily large scale of corporate banking activities, this segment can effortlessly be considered a key contributor to banks’ overall earnings as well as to the Grand Duchy’s economic growth and employment rates.

A bright future for corporate banks

The study revealed that corporate banks in Luxembourg are optimistic about the(ir) future. This positive outlook stems from their confidence after having secured consistent revenue and profit growth in the past — mainly through their financing solutions.

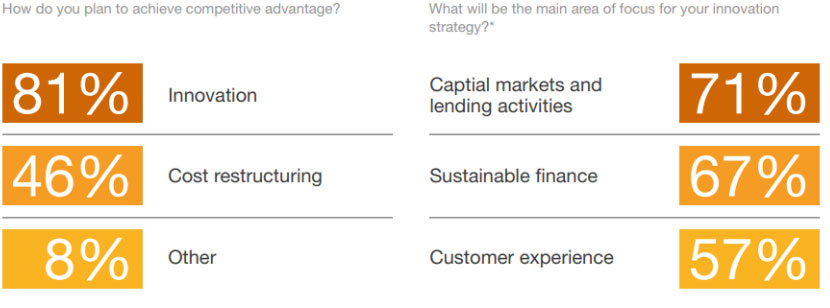

Moreover, there is a growing recognition that innovation and digital transformation are key elements corporate banks can’t overlook. In particular, the sector understands the opportunities that investing in innovation can bring. The survey shows that 81% of them are prioritising this matter as a greater means to achieve competitive advantages than cost structuring (46%) in the coming years.

Yes, without question, the COVID-19 crisis contributed to accelerating this paradigm shift, but it also mirrors banks’ eagerness to make the necessary changes to adapt to consumers’ evolving needs.

When it comes to which area they plan to focus their innovative efforts, the majority answered their capital markets and lending business (71%), which makes sense given the importance of financing products in their corporate banking business.

Corporate Banks’ strategy for achieving competitive advantage

Source: ABBL Corporate Banking Survey Results

These results show that many banks are ready for— if not already undergoing—a full transformation journey that has sustainability, digitalisation, and acquiring the right talent at the centre. This transformation is key to seize all the opportunities to the fullest and, indeed, to create a bright future for corporate banks.

Deploying banks’ transformation journey

As aforementioned, corporate banks are increasingly leaning towards innovation, foreseeing challenges to their efforts and taking steps to mitigate them. In light of this, they have identified three key matters as critical to their transformation journey in the coming years: sustainable finance, technology and attracting the right talent. Let’s explore each of them.

1. Sustainable Finance

Sustainable finance solutions have been on the rise globally with recent societal and market changes, and this trend is expected to continue, driven mainly by client demand and regulation.

Corporate banks are responding to this demand both by financing clients’ sustainability initiatives and ensuring that funds are committed towards meeting the set sustainability goals.

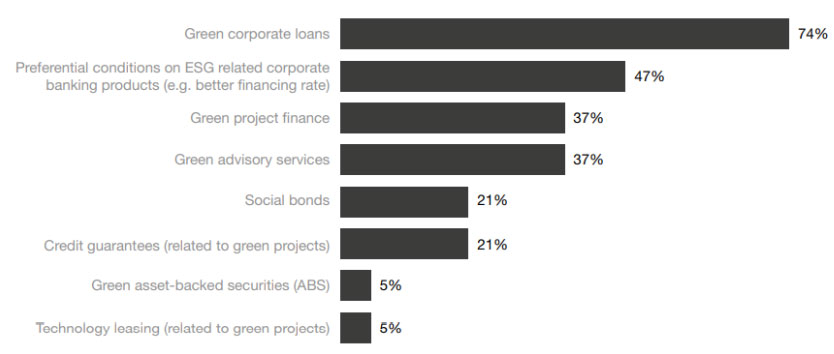

Since financing is a central part of corporate banks’ activities, it’s not surprising that green corporate loans (74%), green project finance (37%), and social bonds (21%) are regarded as part of the top products and services offered by the survey’s respondents.

Therefore, as the sustainability and ESG landscape evolves, corporate banks need to continue to adapt their product and service offerings, as well as strategies for financing and additional funding, to meet the needs of corporations who are more and more moving towards a more sustainable way of doing business and who want to play a role in the EU’s low carbon transition agenda.

Types of ESG products and services offered to clients

Source: ABBL Corporate Banking Survey Results

2. Embracing technology

The COVID-19 crisis has emphasised the power of technology to transform banks’ operations and customer engagement. These technological changes led to an increased demand from bank clients’ for efficient and customised corporate banking services that best serve their needs.

Thus, banks are progressively realising the need to focus on technology that can transform their clients’ experience, striving for real-time monitoring of cash-flows or enhanced flexibility following changes within the banking landscape.

According to respondents, KYC (56%), process efficiency (56%), data storage privacy (52%), and AML (48%), are the areas that will be mainly impacted by technologies.

Moreover, for areas like KYC, that are heavily data-driven, a wider adoption of technological tools becomes a must for efficient data processing and analysis. Emerging technologies such as blockchain and Distributed Ledger Technology (DLT) can help, for instance, with process efficiency, data storage and AML.

Despite the unanimity on the need for technological transformation, there seems to be a discrepancy between banks’ recognition and use of fintech. While 70% believe that collaborating with FinTech companies would be a future requirement for corporate banking businesses, only 37% currently collaborate with a FinTech company – even though the acknowledged benefits of such partnerships.

3. A new type of corporate banker

The digital and societal shifts impacting the banking sector have made it clear that a new type of corporate banker is needed as the sector evolves— one that’s technically skilled and also digitally savvy.

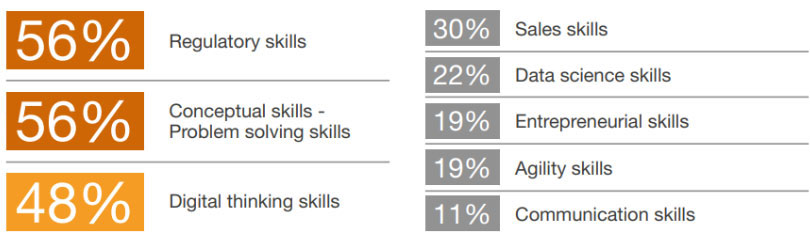

To be more concrete, the survey’s respondents identified regulatory skills (56%), conceptual skills (56%) and digital thinking skills (48%) as the most imperative skills needed to boost Luxembourg’s corporate banking competitiveness.

Essential Skills/Competencies to remain competitive in Corporate Banking

Source: ABBL Corporate Banking Survey Results

These results aren’t surprising. Data breaches are becoming ever-present and privacy concerns are escalating, and, as a result, regulatory and compliance requirements are becoming more restrictive. Additionally, upcoming ESG regulations are introducing a further layer of complexity. Thus, bankers need to be up to date in their operations and management in terms of compliance.

Digital thinking skills would also help corporate bankers better understand their business in the context of accelerated technological development. This means recruiting more or partnering with tech specialists, allowing corporate banks to focus on their core business activities while boosting the technological capacities that ease their operations.

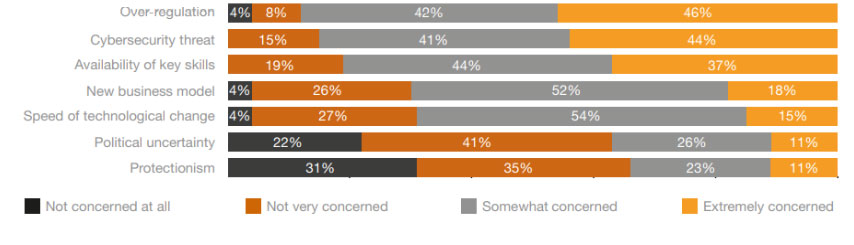

Main challenges for Corporate Banks

Despite their huge growth prospects, corporate banks in Luxembourg face a number of challenges that pose a barrier to the country’s attractiveness to other EU and non-EU banks. We now take a closer look at the three main challenges pointed out by respondents: overregulation, cybersecurity threats and the availability of key skills.

Source: ABBL Corporate Banking Survey Results

1. Overregulation

This was cited as the most common threat to corporate banks, with 88% of respondents voicing concerns about it. That said, overregulation is a two-sided coin for corporate banks.

On one hand, the increase in compliance, restructuring, and implementation costs harm profitability, especially since the fallout from externalising these costs to clients is often greater. Moreover, with the rise of fintech and non-bank start-ups as viable alternatives to traditional financial services, overregulation, by acting as a barrier to potential banking innovation, is decreasing banks’ competitiveness with these companies.

On the other hand, some of the regulations that are rendered at an EU level provide opportunities that banks can explore to be more efficient in implementation. The EU Securitisation Regulation of 2017, which set out a framework for simple, transparent and standardised securitisation within the EU, is a good example.

Thus, Luxembourg can establish itself as a “global hub” by striking a balance when it comes to regulations. This balance would ensure that banks’ clients are fully protected—a crucial point that makes Luxembourg attractive for clients — without totally pushing the cost limits of the banks.

2. Cybersecurity

Considered as a key concern by 85% of respondents, this firmly suggests that the Grand Duchy’s progress in this area —in terms of cybersecurity infrastructure and the presence of a thriving ecosystem that leverages collaboration between public and private sector to create cybersecurity solutions —isn’t yet adequate to cover the financial sector’s need. A stronger collaboration between banks and tech/cybersecurity firms could help in this regard.

3. Key skills

The lack of key skills ranked as a key concern for 81% of respondents, meaning conversely that only 19% of respondents regarded Luxembourg’s human capital to be of any strategic advantage to the financial centre. These difficulties are linked to the costs of finding and retaining the people with the right skill sets to meet the demand for specialised competencies.

In light of this, banks need to examine their current hiring, training and upskilling policies to find out which aspects can be improved or expanded. Likewise, they should consider integrating these policies within the core of their workforce strategy.

Final thoughts

The Corporate Banking Survey was a much needed exercise that confirms Luxembourg indeed retains a truly international corporate banking landscape, and has a unique network of corporate banks from different countries, serving both local and international companies in both the financial and non-financial sectors.

Another key finding is that while Luxembourg’s regulatory ecosystem strongly positions it as a global hub, some overregulation and cybersecurity challenges need to be tackled if the country is to continue to attract and maintain more global players in corporate banking.

Lastly, the results clearly highlight the need for greater innovation, and emphasise how banks, but also government and regulatory bodies have a role to play in driving this transition within the corporate banking landscape. Materialising it could lead to increased operational efficiency, new products and services, and boost Luxembourg’s competitiveness as a global hub for one of the most profitable banking segments.

Through the survey, we were able to identify a number of structural challenges that still hinder corporate banks in Luxembourg despite their immense growth prospects – overregulation, cybersecurity threats, the availability of key skills and the ability to innovate. Now, it’s time to address them to maintain, and even increase, the country’s attractiveness to other EU and non-EU banks.

Daniel Theobald, Senior Manager, Banking Advisory at PwC Luxembourg

The knowledge gained through this study provides a very good overview. In the meantime, however, the framework conditions for banks have changed significantly again. How will the probable rising interest rates, which initially produced a long-awaited and positive effect in connection with soaring inflation, the severely battered global supply chains, and the dispute between Russia and Ukraine, affect the business of banks in Luxembourg? These are already the next challenges to be overcome. But here, too, the jewel of Luxembourg will find the answers.