We bet that got your attention. But being connected to money laundering in any way is not the kind of attention that individuals, businesses and— arguably more importantly — financial centres like Luxembourg want. At all.

There was a funny post on social media a few months back: “#Blockchain is such a sexy topic, that if you shout the word out loud in Luxembourg, people will come from afar and throw money at you.” The words #moneylaundering have the exact opposite effect, sending people heading for the hills due to the workload that is needed for compliance. The stink surrounding dirty money has grown, but at the same time, the laundering process in order to clean it has evolved and become more sophisticated. And these days, if the name of an individual, organisation or a state becomes linked to illegal financial activity, or even the hint of illegal financial activity, they can be irretrievably tainted and branded as corrupt. The recent European-based scandals score very high on the international charts for money laundering and have just increased the pressure significantly.

No one wants that. Reputation is everything. Clients, the people who work for you and society at large have to trust you. The days of pillage are over.

A trip down money laundering lane

Of course financial crime doesn’t just mean money laundering. The term ‘financial crime’ covers a wide range of criminal offences, which are generally international in nature.

It is an increasing concern for all financial institutions, and it is developing together rapidly and equally together with technology. Financial crime affects the largest global organisations but also the smallest companies and partnerships. Preventing and detecting Financial Crime has become one of their biggest challenges, the impact of which extends well beyond monetary losses to reputation and brand, employee morale, business relations, as well as regulatory censure.

Cybercrime and Financial Crime are increasingly converging and are often committed via the Internet and have a major impact on the international banking and financial sectors–both official and alternative.

We have touched on the broader range of financial crime before in The Blog as well as Digital Trust. For the purpose of this article however, we will mostly focus on money laundering.

One of the oldest rackets on the planet

One thing is clear, money laundering is hard to squash — it’s been around for 2,000 years (and for all we know, Neanderthals were laundering rocks).

…2000 years ago, Chinese merchants cycled money through various businesses and complex financial transactions to hide it from government bureaucrats, who sought to garnish the income.

The term”money laundering” itself is believed to have originated in the 1900s with gangsters like Al Capone, who is said to have bought and used laundromats to funnel dirty money (from activities like bootlegging and prostitution) through the laundromats and then mixed the cash with legitimate business income. In that way, Capone and other gangsters were able to hide the money from law authorities.

It wasn’t until later in the 20th century when law enforcement tied the terms “money” and “laundering” together – partly to identify gang members, drug dealers, Mafia kingpins and other criminal elements who disguised the source of cash earned illegally, and laundered that cash into legitimate and legal funds.

In February 2019, Věra Jourová, Commissioner for Justice, Consumers and Gender Equality, European Commission said: “We have established the strongest anti-money laundering standards in the world, but we have to make sure that dirty money from other countries does not find its way to our financial system. Dirty money is the lifeblood of organised crime and terrorism. I invite the countries listed to remedy their deficiencies swiftly.”

So, you can see what we are all up against.

How big is the problem?

Big. Huge! The estimated amount of money laundered globally in one year is 2 – 5% of global GDP, or $800 billion ( $2 trillion in current US dollars), according to the UNODC (The United Nations Office on Drugs and Crime). Though the margin between those figures is huge, even the lower estimate underlines the seriousness of the problem governments have pledged to address.

Numerous scandals that have rocked the world have not only placed a dark cloud of mistrust over individual companies but the financial industry as a whole.

Times have changed. Social media has put massive pressure (for the good) on individuals, companies and countries to play fair. Or else. And the Financial Action Task Force (The FATF) (and more on them in a bit), helps to ensure that this is happening by evaluating countries to very high standards and making those ratings public in the spirit of transparency but also to motivate countries to follow regulations and monitor and squash illegal activity. Because for a country to be truly competitive in the global financial world, it has to value and maintain a solid reputation, based on compliance with the standards defined by FATF.

That said, we all know that financial crime and specifically money laundering still exists. Some people claim it is a tide that cannot be turned. But that is exactly why it has to be fought. Hard.

Can we win the war against money-laundering?

It takes a huge commitment enforced by regulations and constantly improving and adapting procedures.

What can you do? Risk awareness is a crucial point to start with. Well you can do really special things like invite an international guest, already known in the context of the movie “The Infiltrator”: former DEA undercover agent Robert Mazur, to come and speak to a large group of professionals in Luxembourg. Which is exactly what our Forensic Services and Financial Crime Leader, Michael Weis did. And more than once. Mazur was given undercover training and spent more than a year constructing a sophisticated front with real businesses to clean money for Pablo Escobar and his infamous cartel. He has made a second career out of sharing his views on the latest international money laundering scandals and on how an ever increasing regulatory landscape is coping with this.

Inviting such a personality has a three fold benefit: he is well known and an incredible speaker so it draws a big crowd in to an anti-money laundering event thereby heightening awareness, it shows that a company like ours is deadly serious about the reputation of the Luxembourg financial centre and helping our clients to cope with tightening regulations. We are taking an active role in fighting financial crime, and, let’s face it, it brings one of the world’s experts on money laundering to speak. Want to know what activities to look out for and where the risks are. Trust us, Robert Mazur knows..(the third benefit!).

The threat is real

Money laundering and terrorist financing are a threat to global security, integrity of the financial system and sustainable growth. Laws to combat money laundering and the financing of terrorism are designed to prevent the financial market from being misused for these purposes. These are very serious problems, particularly when you consider the state of geopolitics on our planet at the moment.

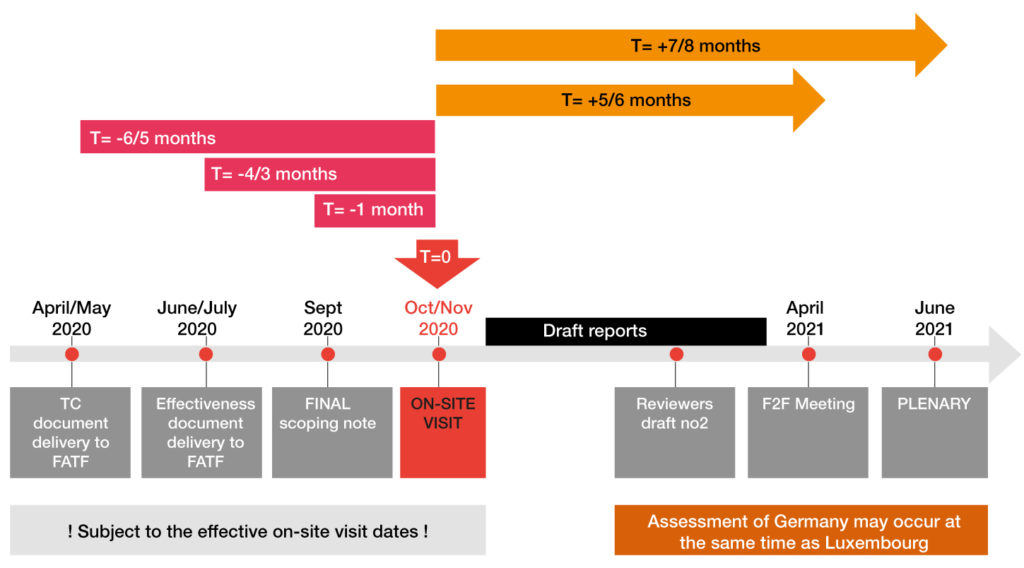

As mentioned above, the leading global organisation trying to help fight financial crime is the Financial Action Task Force ( FATF). Due the disruption to business and social activities caused by the COVID-19-related crisis, the Financial Action Task Force (FATF) and regional FATF-type organisations have postponed the Luxembourg evaluation to October 2021. When the FATF does comes to town, a country, and a selection of its institutions, has to demonstrate the existence of, and adherence too, very high standards as well as government regulations.

FATF is the global standard-setter in the fight against money laundering and terrorist financing. With their new focus on effectiveness, the assessment of Luxembourg, and its actors in the financial sector, will become more intrusive. They will not only speak to the CSSF, FIU or government officials but possibly also to YOU. To avoid bad surprises, CSSF will have a very close look at AML compliance before FATF visits and you better anticipate that now. – Michael Weis, Partner, Forensic Services and Financial Crime Leader, PwC Luxembourg.

The FATF will come to Luxembourg for a technical visit to assess the country’s legal and regulatory set up, and to conduct on-site effectiveness visits on a representative sample of market players. They don’t joke around and absolutely everything has to be in order and available, with documentation in the correct FATF vocabulary with all the “t”s crossed and a dot on every “i”.

There is a mutual evaluation process, which is very thorough and intensive. In a single round of evaluations, the FATF assesses over 40 jurisdictions (other jurisdictions in the global network are assessed by the the FATF-style Regional Bodies, the The International Monetary Fund (IMF) and the World Bank). Each assessment takes 14 months for the team to complete. The FATF Plenary discusses and adopts two mutual evaluation reports at each of its three annual Plenary meetings. This means that each assessment cycle takes 7 to 8 years to complete.

This upcoming FATF visit is the 4th round of mutual evaluations.

Through its nine FATF-Style Regional Bodies (FSRBs), the FATF brings together a global network of 205 jurisdictions that have each committed at the highest political level, to implementing the FATF Recommendations. The The FATF and FSRBs conduct peer reviews on an ongoing basis to assess how effectively their respective members’ AML/CFT measures work in practice, and how well they have implemented the technical requirements of the FATF Recommendations.

On their website there is a table that provides an up-to-date overview of the ratings that assessed countries obtained for effectiveness and technical compliance (last updated on 17 April 2019). These should be read in conjunction with the detailed mutual evaluation reports, which are available on the same website.

Forewarned is forearmed

As part of the regulators focus on AML, one can expect a lot of AML-dedicated onsite visits of the Commission de Surveillance du Secteur Financier (CSSF). They will check very deliberately the compliance status with AML regulations and they will certainly leverage on the intelligence garnered from the AML questionnaires that everyone had to answer to be ready (or still has to). This is likely NOT going to be a breezy summer day’s walk in the park, especially considering all of the new requirements such as the:

So remember, forewarned is forearmed. Do your homework and make sure you are ready. Because this visit is just the aperitif. In 2020, FATF will come again to visit some sample representatives from the industries. And this visit they will assess the effectiveness of the existing anti-money laundering regime and grill people – i.e. quite likely some of you dear readers – on your AML awareness, your knowledge and your implemented approach.

Anyone preparing for the visit should absolutely make sure:

You have a very good knowledge of the recommendations, methodology and assessment procedure (This is key for the interviewees)

You have a high quality of drafting of the reports on TC (Technical Compliance) & effectiveness

You ensure there is a high availability of staff during the onsite visit

You are aware that external events may impact the mutual evaluation

It is a lot of preparation and a lot of work but it is all for very good reasons. Let’s make this the year of AML.

What we think

Birgit Goldak, Partner, Risk Assurance Services at PwC Luxembourg

In Luxembourg, as a major financial centre, the majority of financial institutions are subject to Anti-Money Laundering/Combating the Financing of Terrorism (AML/CTF) regulations at both the local and international levels. 2019 is a year where Anti Money Laundering is a big topic on the global table and it is not without its challenges with different legislative and regulatory changes. The transposition of the 4th and 5th AML Directives, in line with the concentration of international efforts to fight money laundering and the financing of terrorism, will keep compliance officers busy for some time. Last but not least the upcoming visit of the FATF to assess Luxembourg puts AML once more in the spotlight. It takes enormous preparation in advance and companies need to have everything in order for the assessment from start to finish can take up to 18 months and it is an exhaustive and exacting process.