“To quota or not to quota” to accelerate women’s participation in boards and, in general, in leadership positions? To some, that’s the way to walk faster on the sometimes rocky path to achieving gender parity.

Like in all human-centred matters, when it comes to diversity matters nothing is black or white and realities are nuanced. For instance, the latest Luxembourg Fund Governance Survey 2020 shows an upward trend in the number of female board members compared with the 2018 survey but the under-representation of women on boards remains an issue in the Grand Duchy.

While Luxembourg (still) relies on organisations’ will and commitment to gender parity, setting up voluntary targets to be achieved over a certain time interval, other countries—Norway, Spain, or France, for instance—have made use of binding quotas to increase female hiring, boost female career development and secure the presence of women in decision-making positions.

And again, nuances must be recalled. Both approaches, which answer the political and social characteristics of each country, have shown to be effective. Ultimately, the flexibility to read contexts and find ways to address the obstructing points is what truly counts.

Also, let’s not forget that COVID-19 has hit the situation of families in Europe hard because of the need to combine house responsibilities, home schooling and work. However, women have been more impacted as they remain the main home caregivers, regardless of their hierarchical position in business.

In this article, we revisit statistics on women’s participation in corporate leadership in Luxembourg and in Europe based on in-house and third-party research and reflect on the path to achieve gender parity.

Women on Luxembourg’s boards according to research

Back in 2009, Luxembourg’s Corporate Code already recommended boards to have an appropriate representation of both genders. Since then, the country has made some progress.

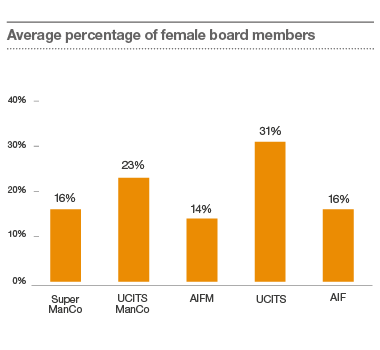

Over the past Fund Governance Surveys we’ve conducted together with ILA, we have observed that the number of female board members is following an ascending trend, from 14% in 2016, to 16% in 2018 and 22% in 2020.

Yet women still only make up barely a fifth of board members.

Gender equality could be part of the great list of chimeras that the world pursues. However, and although research shows divergent results on the effectiveness of diversity itself in the performance of boards—i.e. including diversity for the sake of it—it is clear to conclude that the culture of the board is what can affect how well diverse boards perform their duties and oversee their firms.

A diverse board is more likely to benefit from diverse thinking, which can stimulate the board’s creativity. That diverse thinking shouldn’t only be attributed to the fact that women are, by nature, different from men as John Gray gracefully describes in the book “Men Are from Mars, Women Are from Venus”. That would be, honestly, simplistic.

It’s actually the mix of diversity factors that makes the inclusion and management of it so important. One of its benefits is to bring functional experience that seems to be pivotal to a board’s diversity. According to research from the University of Toronto’s Rotman School of Management, “women [in boards] were more likely than men to contribute additional, new, and more distinct types of expertise”.

Getting back to the Luxembourg case, the upward trend on female presence on boards also signifies the first step to addressing long-term risks, such as those resulting from potential lawsuits and reputational damage that the ESG investments trends are only augmenting.

The standard directors’ profile: what does it look like?

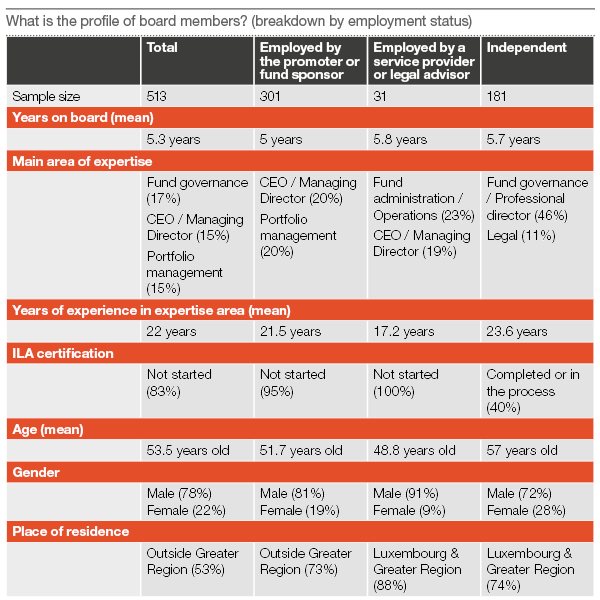

The typical board member of Luxembourg-based funds and management companies is accurately exemplified by Bernard, a fictional character we’ve created to illustrate the case.

Bernard is in his mid 50s and, although he doesn’t think seriously of retirement yet, he has started flirting with the idea of buying a house somewhere in the Canary Islands and moving there. His job, after all, isn’t anything he can complain about and allows him to dream of that possibility. Indeed, he’s an executive director in an important Luxembourg management company and, since 6 years ago, he has taken part in the board.

With his 20-year experience in fund governance and portfolio management, he considers that the need for a fund director’s official certification isn’t truly urgent or even necessary. However, training in specific legal, tax, or new investment vehicles is.

Bernard doesn’t live in Luxembourg. He visits Luxembourg once a month, but with the COVID-19 crisis, those visits have become more scattered over time. His habitual residence isn’t in the greater region either. .

On average, 19% of directors employed by a promoter or fund sponsor are women; that number drops dramatically to 9% when it comes to directors employed by service providers.

However, the case of independent directors is slightly different. First off, our research has revealed that they are gaining ground and are more numerous, currently representing 35% of Luxembourg boards, up 5% compared to results in 2018. In the case of alternative investment funds (AIFs), they even represent half of the board. Second, in comparison with others, independent directors are more likely to be female, representing 28% of boards. On top of that, they are, on average, five years older than executive directors and live in Luxembourg or the greater region.

The drivers of the growing presence of women in boardrooms

Maybe this progress has been driven by political and regulatory pressure, for instance, in the shape of quotas? Let’s face it, in the most ideal situation, the growth of women’s presence in boardrooms should be the result of a true commitment to including gender diversity because of the benefits it is expected to bring. But quotas exist because any other voluntary approach moves too slowly.

In diversity matters, having no formula could be the best formula. If quotas are effective growth drivers of female leadership in certain countries, why not continue applying them more consistently then? On the other hand, if voluntary targets, like in the case of Luxembourg, work, then why change strategy?

Nevertheless, the formula gets more complicated because another driving force could be growing pressure from investors who increasingly show interest in environmental and social matters. The rise of ESG—Environmental, Social and Governance— investments and the need for accurate ESG reporting are a clear example. The weight of each component of ESG in investors’ decisions, though, is yet to be seen but we tend to think that, for now, the Environmental part outweighs the other two.

ESG could become an influential factor for the growth of female presence in boardrooms and, by extension, in leadership positions in business. Should companies be required to disclose gender diversity indicators in their annual reports under the SFDR or the NFDR, perhaps it may naturally improve the women’s presence ratio in board and leadership positions without needing to put quotas in place.

When talking to some of our female partners on this matter, they pointed out that, five years ago, walking into an industry conference was an almost monochromatic experience: it was all men dressed in dark suits.

Nowadays, the room is more colourful. They see an increasing number of women attending conferences (online or presential), in management positions or as speakers. There are, doubtlessly, qualified women in the industry who can become board members. What’s missing is the boost.

We think all drivers are influencing, more or less successfully, the growing presence of women in boardrooms. Some organisations are being purely driven by regulatory pressure, while others have a thorough reflection on gender diversity and, therefore, a more systemic approach.

But the timid success or the trend shouldn’t leave anyone complacent. Recent statistics from the MSCI who serve asset managers, banks and wealth managers report a slowdown in the rate of increase for female representation on boards in 2020. According to the same source, having all the efforts and commitment running, female representation in the boardroom will only reach 50% by 2045.

Women in Europe’s boardrooms

The European Union (EU) has been active in shortening the imbalance between women and men in leadership and decision making since more than a decade ago. By the end of 2012, the European Commision had already presented a directive proposal to improve gender balance among non-executive directors of businesses listed on the stock exchange. But bickering and diversified political agendas have played their cards and, until today, the directive remains stuck in the EU legislative pipeline. The aim is to reach a minimum of 40 % of women on non-executive boards of EU companies.

We have mentioned before that each European country is following their own approach to accelerate the presence of women on boards and decision making roles in business. Austria, for instance, starting in 2018, applies a quota set at 30% women on board positions for listed companies. That’s anything but new in Europe. Norway in 2003 and France in 2010 had already implemented these quota-driven measures but the number of countries using it is growing. In Q3 2020, Switzerland followed Austria, approving a provision that requires large companies to introduce a gender quota of 30% for their boards of directors and of 20% for their executive boards.

Germany is taking visible steps towards gender equality in boardrooms. Earlier this year, it has approved a draft law for the equal participation of women in leadership positions in both the private and public sectors.

According to the European Women on Boards Gender Diversity Index 2020, 34% of board members are women, and 28% of leadership functions fall under female professionals’ responsibility. Out of the 668 companies studied in the latest research (Luxembourg, unfortunately isn’t included in the report), only 62 have a GDI (Gender Diversity Index) of 0.8, being 1 the highest. Sweden, France, Norway and the United Kingdom rank on top. On the other hand, only 42 companies have a female CEO and only 9% Chairs of boards are women.

The perfect gender parity formula, isn’t quite there yet (and it won’t be)

There isn’t a perfect formula to achieve gender parity on the board or increase women participation in leadership positions. After all, gender matters are deeply rooted in our education and social systems, even before the moment we are born. Finding people to blame isn’t the right approach, unarguably. What’s clear is the need to accelerate the journey to equality, with governments and businesses giving and sharing actionable advice and tangible measures that guarantee that parity, once achieved, can be maintained because it’s entrenched in organisation’s core and values.

We suggest that short-term regulatory measures must be accompanied by long-term changes to the education systems.

Beyond gender equality, the issue of diversity in race and ethnicity at the board level of funds and management companies also merits further investigation that we want to address in future editions of the Luxembourg Fund Governance Survey.

What we think

Serene Shtayyeh, Risk Assurance Services Leader at PwC Luxembourg

When looking at the Fund Governance surveys we have run over the last decade, they show that the percentage of female board members has slowly improved over the years. Whether the progress is fast enough or whether regulated quotas are needed is unclear with plenty of differing opinions out there. What is clear however, is that a lack of diversity will no longer be acceptable to stakeholders, whether it be gender or ethnicity. Systematic planning by companies, corporate training and yes, maybe regulation, is therefore needed in the industry.