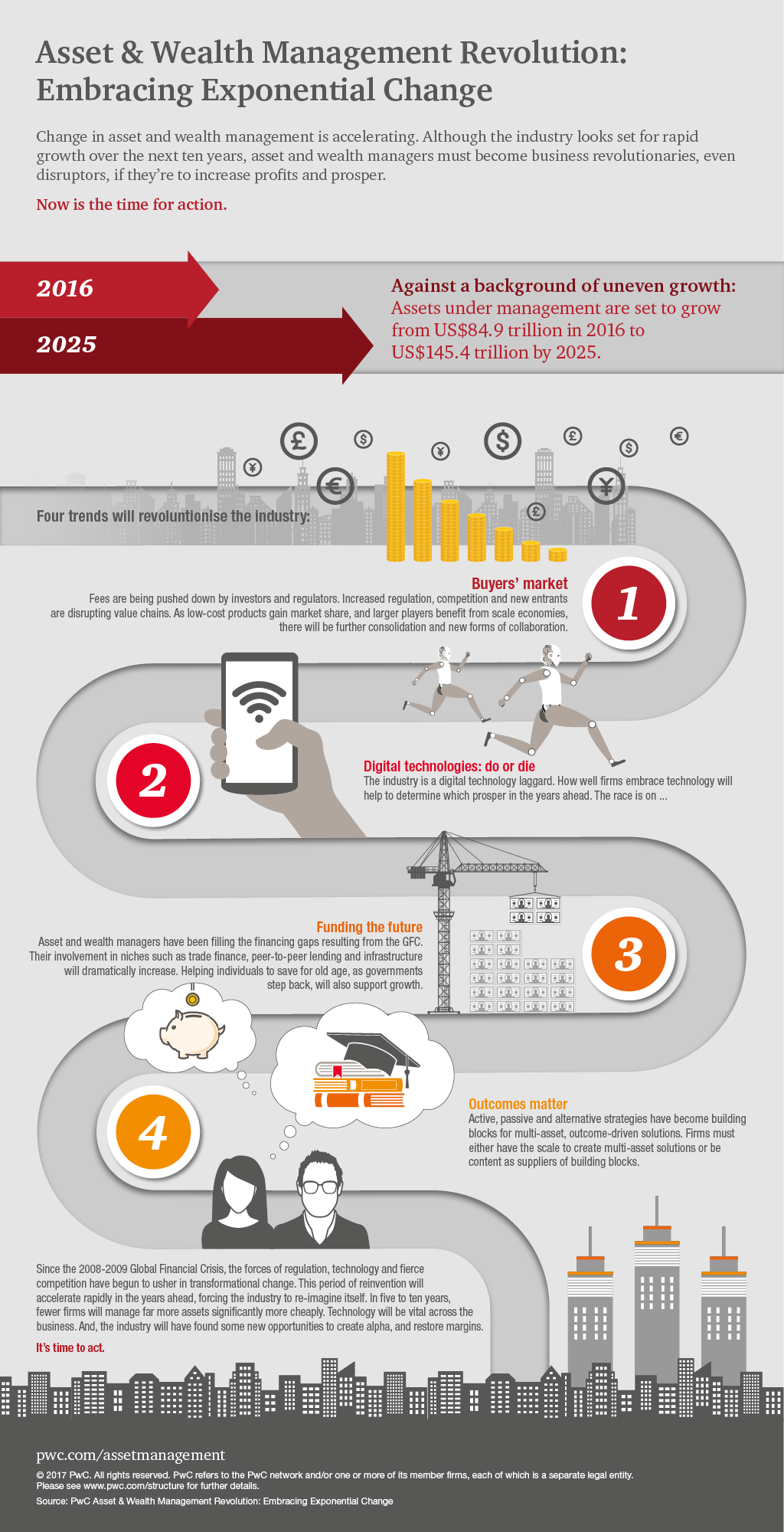

Change in Asset & Wealth Management (the ‘AWM industry’) is now accelerating at an exponential rate. Although the industry is set for growth over the next ten years, asset and wealth managers must become business revolutionaries, even disruptors, if they’re to survive and prosper. We’ve identified 4 interconnected trends that will drive the AWM industry’s revolution. Between them, they will squeeze industry margins, making scale and operational efficiency far more important, and meaning that all firms need to integrate technology in all areas of the business and develop a clear strategy for the future.

The context: Asset & Wealth Management to reach US$ 145.4 trillion by 2025

Dariush Yazdani, Market Research Centre Leader

Assets under management (AuM) will continue to grow rapidly. We estimate that by 2025 AuM will have almost doubled – rising from US$84.9 trillion in 2016 to US$145.4 trillion in 2025. This growth will likely be uneven in consistency and timing: slowest in percentage terms in developed markets and fastest in developing markets. But there are risks. Rising populism in Europe, Brexit negotiations, China’s transition to a consumer-driven economy, Asian geopolitics and the potential changes in US policies on regulation, tax and trade all create uncertainty.

1. Buyers’ market

Fees are being pushed down by investors and regulators. Increased regulation, competition and new entrants are disrupting traditional value chains and revolutionising wealth managers’ raison d’être. Regulations are being introduced worldwide to prevent asset managers from paying commissions to incentivise distributors, leading to lower cost retail products. Meanwhile, institutional investors have the tools to differentiate alpha and beta – they will pay more for alpha but not for beta. As low-cost products gain market share, and larger players benefit from scale economies, there will be further industry consolidation and new forms of collaboration. Asset and wealth managers must be ‘fit for growth’ or they can expect either to fail or to become acquisition targets. So, they must act now.

2. Digital technologies: do or die

The AWM industry is a digital technology laggard. In other words, technology advances will drive quantum change across the value chain. And this will include new client acquisition, customisation of investment advice, research and portfolio management, middle and back office processes, distribution and client engagement. How well firms embrace technology will help to determine which prosper in the years ahead. Meanwhile, technology giants will enter the sector, flexing their data analytics and distribution muscle.

3. Funding the future

Asset and wealth managers have been filling the financing gaps that have emerged since the global financial crisis. So far, they have been first movers, providing capital in areas short of funding due to banks’ regulatory and capital limitations, as well as investing in real asset classes. To generate alpha, their involvement in niche areas like trade finance, peer-to-peer lending and infrastructure will dramatically increase. Equipping individuals to save for old age, as governments step back, will also support growth in AuM. Therefore, action is needed to capitalise on the gaps.

4.Outcomes matter

Investors have spoken loudly. They want solutions for specific needs – not products that fit style boxes. So, active, passive and alternative strategies have become building blocks for multi-asset, outcome driven solutions which will increasingly include environmental, social and governance outcomes). In this vein, demand for passive and alternative strategies will grow quickly. While active management will continue to play an important role, its growth over the near term will be slower than passives. Firms must either have the scale to create multi-asset solutions or be content as suppliers of building blocks. Managers must deeply understand their investors’ needs, tailor solutions and focus on optimising distribution channels. They must also focus on their core differentiating capabilities and move to outsource non-core functions, such as tax compliance. In fact, investors have great choice. And, they will move to optimal solutions regardless of prior loyalties.

What we think

These four trends will transform the industry’s nature and structure. Scale, price, diverse people and technology capabilities will characterise the largest firms.

Steven Libby, Asset & Wealth Management Leader

Smaller, specialist firms will prosper if they offer excellent investment performance and service. The industry must act in three areas:

Strategy – Firms should reorganise the business structure to support their differentiating capabilities and to cut costs elsewhere.

Technology – Every firm must embrace technology as it impacts all functions.

People – Different skills are needed, backed by new employment models. Firms must find and develop people with new skills and adapt their employment models to nurture and retain them.

The revolution at a glance

Embrace the revolution. Discover the world of Asset & Wealth Management by 2025 in our new report.