Banking is at a crossroads, facing threats and opportunities from events like Brexit, as well as continued change from social and technological evolution. Disruption is no longer on the horizon; it’s on banks’ doorstep. Here are three reasons why a banking revolution is underway.

1. Clients want personalised and complete banking advice

It’s no longer acceptable for bankers to build trust solely on the notion that they’re the expert. Today, clients want more personal, more real-time, more effortless interactions.

Also, they’re less tolerant of historic pain points, like processes they consider complicated, time-consuming, and risky; not getting adequate support; feeling undervalued and exploited.

The expert view

Olivier Carré, Banking Leader

Given the demographic shift under way, bankers need to get this new trust equation right and include other services like tax and wealth planning. The inheritors of wealth over the next five to ten years will not necessarily choose to keep their parents’ financial advisors. It’s all the more important that by 2020 this new generation will control more than half of all investable assets, i.e. about US$30 trillion. All in all, this client base shift implies redefining the role of the banker whose ability to provide a complete client experience will be essential.

2. Technology is changing client expectations

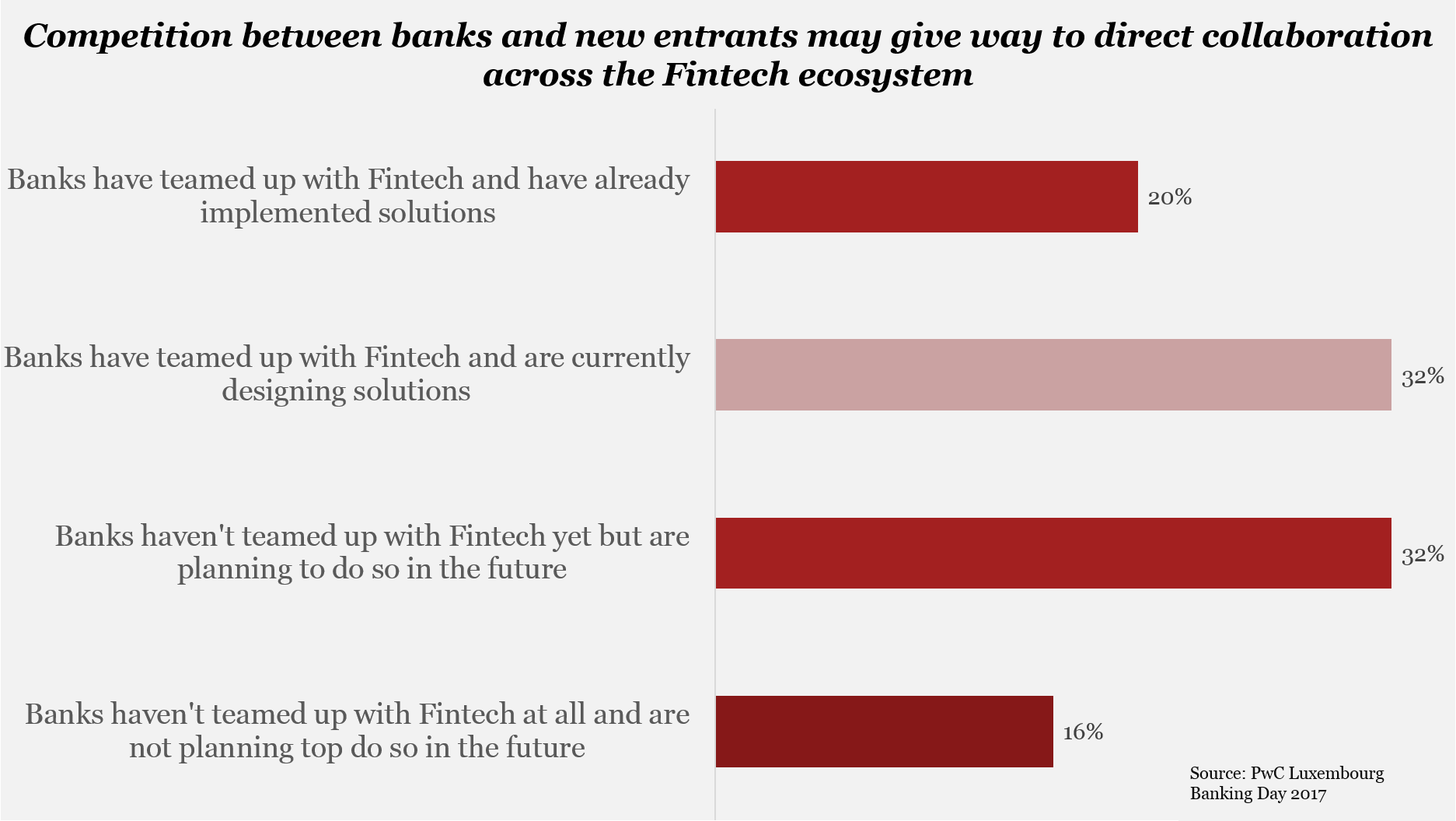

Clients expect offerings, contacts and overall relationships with banks to be seamless and address their particular needs. So, cooperation with Fintech could definitely make the task of becoming customer-centric easier to achieve as the new entrants have important complementary skills. On their side, FinTech could benefit greatly from partnerships with traditional banking players that possess insightful customer data. Spending patterns and wealth data could be important indicators for Fintech tailoring the next game-changing solutions.

Finding the “sweet spot” between competition and co-operation where traditional banks and Fintech truly collaborate might be cumbersome. However, once a modus operandi is established, both parties will profit. Only then will the banks be able to stem the tide of business model disaggregation by new entrants in the Fintech space.

3. Europe is redefining itself

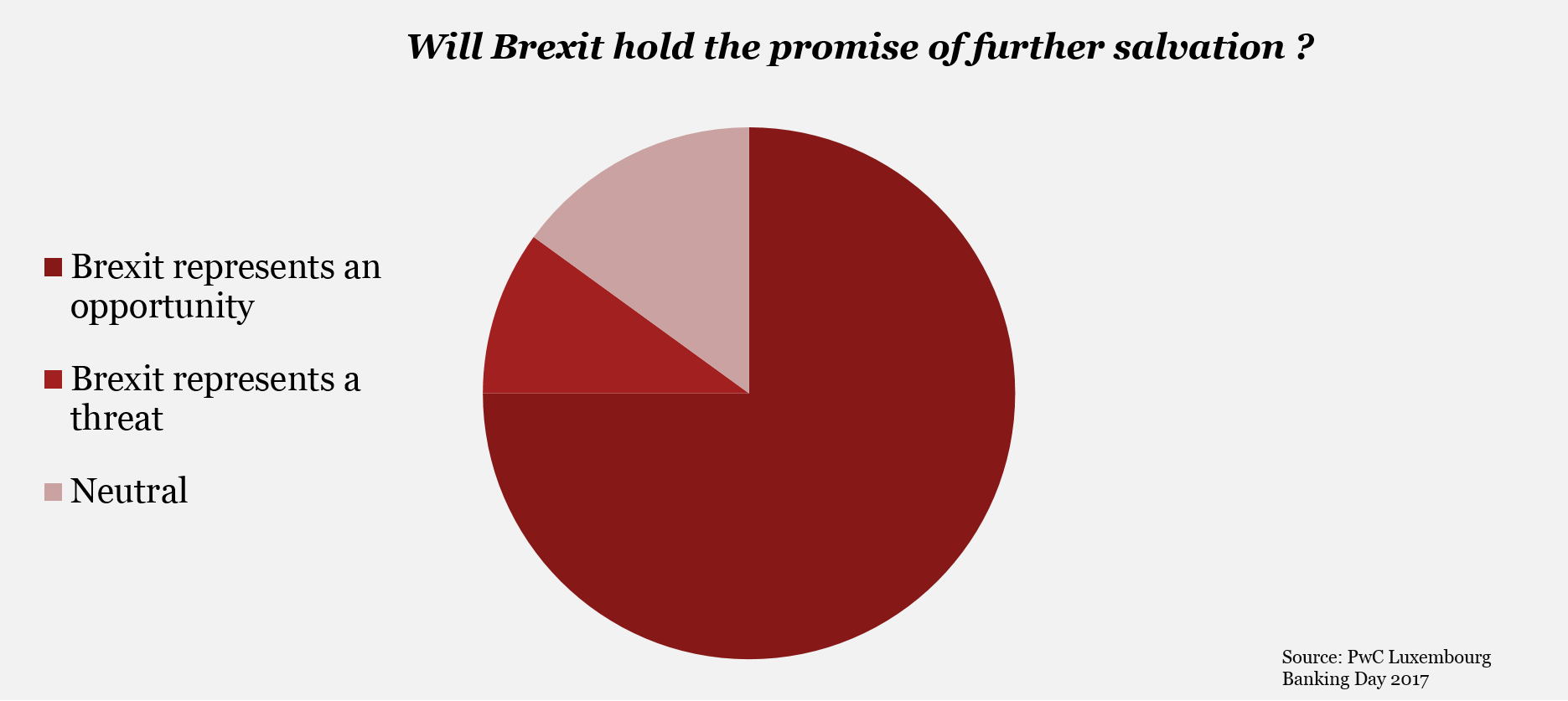

Questions remain as to whether Brexit holds the promise of further salvation in this industry. So far, Luxembourg played the friendship and complementarity card.

The banks that come to settle in Europe need a stable country within which to operate in the Single Market. In this case, Luxembourg can offer pragmatic answers in an accessible, open and multicultural environment.

To get an overview of the what Banking in Luxembourg looks like, read our brochure.