First impressions count. In life, in business, when it comes to technology matters, when we think of blockchain. The history and evolution of bitcoin, one of disruption, fluctuation and volatility, seems to have done a disservice to the 10-year old most conspicuous distributed ledger.

Bitcoin just happens to be the most renowned blockchain application that went mainstream. To some, their destiny is undeniably linked and is dyed dark. However, blockchain, more discreetly than noisily, is finding innovative uses in supply chain management, agriculture, land ownership records, traceability (food, luxury goods, etc) apart from the ones in financial services.

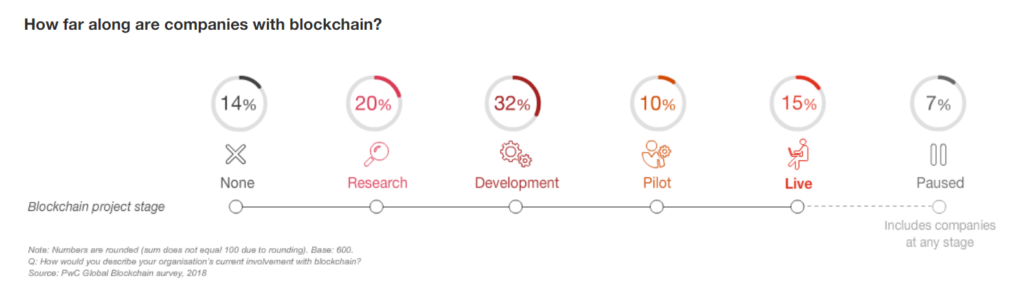

Could blockchain generate USD3 trillion a year in business value by 2030? The path for that prediction to become a reality seems to have started. Our most recent Global Blockchain Surveyreveals that 84% of executives have at least some blockchain involvement, and 15% of them have or had in 2018 – the year of the survey – a live project. But any prediction can fall apart because of a paradox.

The more society understands what blockchain can do, the less the chances to escape its almost heroic destiny: the technology is geared to become the intermediary of trust. And voilà, the paradox: most people and institutions don’t trust blockchain, that can address and help solve a growing trust scarcity in governments, business, society and even among citizens.

The law of supply and demand doesn’t apply in this case. There is too much need for trust and such little ways to rebuild it.

We rarely take the time to reflect on how much technology has influenced our lives and systems.

The printing press was a catalyst in democracy.

The locomotive took us to uncharted territories. The far far west is now Silicon Valley.

Social media’s live streaming has triggered, for the good and the bad, a growing wave of citizen journalism.

To some, blockchain is arguably the most fundamental technological revolution of our time, more than artificial intelligence and other emerging technologies. Can it live up to it?

We’ve built this article upon the ideas and reflections shared during the event “Blockchain (much) more than crypto“, held in Crystal Park in October 2019.

Balancing expectations

Just google it. The overwhelming number of articles where blockchain and trust appear together shows the interest and expectations around it. Some set the bar too high, claiming that the distributed ledger is going to solve a large majority of trust-related issues.

Certainly, blockchain has all the credentials to allow for better, cheaper and more secure transactions. In audit, for instance, it can be a tipping point. In some years time, we could refer to “the audit era before blockchain” as we currently do when we talk about “the era before the internet.” But removing misconceptions about the potential of blockchain is important to manage expectations.

As blockchain emerges as a more mature technology and more tangible cases of applications appear, we’re learning to be more realistic. Rather than a universal, one-size-fits-all solution, blockchain’s main value is versatility. Whether public or private, it’s convenient for all industries, or almost. The common challenge all industries face, however, is determining which parts of the business the technology helps, how to implement it, and how to get the organisation prepared for a radically new way of understanding trust and deliver on trust. The same goes for governmental solutions powered by blockchain.

Sometimes triggered by the media or by the excitement of the market, avid to find new streams of wealth, blockchain is paying the high price of an early fame that Bitcoin and other cryptocurrencies helped shape. None of them is the villain. None.

Intending that blockchain can solve the trust issue, alone, is naive. Solving the trust crisis is an inescapable human responsibility.

What blockchain can do is help nurturing that trust.

Blockchain’s holy grail

Also called “the trinity”, there are three characteristics intrinsically associated to blockchain:

Decentralisation

Scalability, or the ability of the technology to manage a massive number of transactions at the same time.

Security

At this point, few could dare to deny the need for more secure, stable systems on all business and social levels. The blockchain’s holy grail, therefore, arises as a promising alternative to fulfil that need.

The socio-economic context in which any technology development will deploy can greatly influence its rise or its fall. Not only certain common understanding is needed; it takes political and business will too.

Purists think of blockchain as public, peer-to-peer networks. It means no central administrator or centralised data storage. Then, for blockchain to be widely adopted, we need to engage ourselves in answering a fundamental, unavoidable question: how much control are we, as a society, willing to give up?

There is a growing debate around private, public and hybrid blockchains and what they are suitable for and in which circumstances. Until now, most POC (proofs-of-concept) on blockchain have been run at organisation level, and, as expected, private blockchains have been the preferred choice because of the possibility to address specific needs.

Blockchain, a loyal team player

Give a dog a bad name (and hang it). Blockchain has also earned, free of charge, the reputation of disruptive technology. Indeed, it has all the potential to become one, but it can also be complementary to legacy systems, a loyal team player.

This approach is gaining ground in the technology’s path to maturity. It’s also more convenient for reversing the negative headlines that have grabbed all the attention because small-scale initiatives that actually work and become reference cases are proving blockchain is a powerful intermediary of trust.

Blockchain is yet to find a clear lane in regulated industries like financial services. Although executives and CEOs show growing trust, clients want to see a more robust bet.

There is so much going on around it lately. The Libra stablecoin project, China’s CBDC—Central Bank Digital Currency, the call for a global digital cryptocurrency to mitigate certain international monetary system weaknesses, etc. all of them have blockchain as an underlying technology.

Ironically, the best strategy to adopt blockchain is to unblock the mistrust chain.

Blockchain is more than crypto

What do we mean when writing “blockchain is the intermediary of trust”?

Well, we mainly think of data, because blockchain’s main power is, precisely, how it manages and deals with data. Technically, its data structure is explained as a back-linked record of blocks of transactions, which is ordered. But we don’t want to get technical.

Simply put, the trust blockchain brings is embedded in how data is managed, stored and transferred. This has triggered a growing number of blockchain-powered processes and solutions across several sectors other than the cryptocurrencies industry, especially in Asian markets.

India, for instance is using blockchain to issue birth certificates, a document many people lack. With the registration of data profiles in the public sector systems, benefit distribution is improving, access to welfare for instance. Using blockchain technology to land ownership recording is also gaining ground.

In Asia, blockchain-based bottle traceability is used in the wine industry to guarantee authenticity. The technology is a mighty ally to fight counterfeiting, a growing problem high profile wineries face.

In an effort to address food safety concerns, Walmart China teamed up with us to launch a blockchain-based platform for traceability. Elton Yeung, strategy and innovation lead at PwC Mainland China and Hong Kong, said in the release, last June: “We believe that Walmart’s Blockchain Traceability System will be an excellent example of blockchain technology applied in the retail industry, helping to improve food safety and quality management, and providing a strong guarantee for building consumer trust.”

Europe and the US are more focused on using blockchain in financial services but there are some interesting examples in other fields. For instance,the Belgian First Division has brought back the love for collecting sports trading cards with a significant twist. By issuing crypto-trading cards that fluctuate in value based on individual players performance, fans can trade their cards via an online auction platform. Equally, influential football clubs like Arsenal Borussia Dortmund and Real Madrid are using blockchain-based platforms for people to find, collect and trade authenticated collectibles via mobile technology.

The company behind this solution is Fastastec, that teamed up with us to develop this project.

Blockchain has started being used to authenticate luxury goods and detect fraud. The group LVMH launched AURA, cryptographic provenance platform, earlier this year.

The US-based company V-chain has developed “CodeNotary”, a distributed-ledger solution to guarantee the veracity and integrity of digital assets to teams and to others outside the team. They want clients to build continuous trust into their entire DevOps process. The solution “Smart Credentials” we developed in-house also covers a similar need. By issuing digital certificates in real time, our blockchain solution reduces exposure to fraud and give individuals more control over their personal data.

Blockchain in the Old Continent

Europe is slowly being seduced by blockchain but the lack of regulatory consensus ralentises the adoption pace. That isn’t surprising in the old continent. It is well-known for its propensity to give clear guidance and define comprehensive regulatory frameworks. Nevertheless, European Union experts foresee a multiplication of “crypto companies” once countries find certain consensus around KYC—Know your customer and AML—Anti Money Laundering aspects.

The European Union wants to champion blockchain in public and public sectors. To foster interoperability and standarisation, stimulate knowledge sharing and collaboration, maximise impact across sectors and promote adequate skills and training, all actors must work together.

To put theory into practice, research done by the EU Commission’s Joint Research Centre (JRC) looked at blockchain beyond financial applications. Following a co-creation approach,

It searched for tangible transformation ideas in nine industrial sectors (#Blockchain4EU) such as space and aeronautics, food processing, transport and logistics and energy.

An interesting research outcome is Gigbliss, a hair dryer connected to the energy grid. Gigbliss’ three models—auto, balance and plus—run on a smart contract.

Blockchain through the Luxembourg lens

What can be done to improve the Luxembourg blockchain competitive ecosystem?

Quite frankly, there is large room to take action. At institutional level, the country has built an interesting institutional structure to support blockchain. Infrachain, for instance, works on creating a governance framework for blockchain applications to become operational. Lëtzblock, on the other hand, promotes the understanding and adoption of distributed-ledger technologies and blockchain across both public and private sectors.

At business level, some businesses are already implementing blockchain solutions. The case of one of the largest Luxembourg companies that operates in the iron & steel industry is illustrative. After an exercise of assessment, the company has integrated the technology into various processes—traceability, predictive maintenance, 3D printing of spare parts, logistics automation (consumables ordering). Because the company relies heavily on data process models, addressing cybersecurity issues is a must, and blockchain happens to be very handy on this arduous task.

Critical to any attempt to integrate blockchain into organisational processes is to think of the goal, the value it will bring, and the skills needed for deployment before thinking of the “how”.

Thinking of blockchain in Luxembourg is also thinking of upskilling, to close the knowledge gap.

Final reflections

Blockchain moved out of the lab to go through a pilot mode and, in some cases, is already at the production stage. Despite being a technology in which trust, immutability and shared governance join forces for the good, it has yet to go over a trust paradox and the lack of understanding of how it works.

Blockchain is a distributed ledger technology which versatility can support countless business processes, but, by no means, it’s a technology approach. What it prompts, however, is a profound reflection on how organisations understand governance, data management and control.

The future business warfare won’t only relate to avant-garde products or innovative business models. “Pure” competition will give space to “coopetition”. Indeed, with a cautious mix of cooperation with suppliers, customers, and competitors producing complementary or related products, businesses may gain more than what they do when playing alone. Blockchain is set to be an enabler of coopetition because of its embedded traceability and data management.

[Any new technology] “starts out clunky and looks like a toy, school will ban it, parents will fear it, talking heads will bemoan it, and boring people will feel superior for not wanting it, until one day it is as normal and unremarkable as the book.

Would this be the story of blockchain too?

Did you know?

As from 1 October 2019, we are accepting Bitcoin payments. As part of the firm’s market assessment, what quickly became clear is that we could not continue to invest in the field, promote it, build solutions for clients and support their transformation while not being exposed to it.

What we think

Thomas Campione, Blockchain & Crypto-assets Leader at PwC Luxembourg

The story of blockchain hasn’t been easy. Misconceptions on its benefits and potential uses make any reversing exercise to build a better reputation very difficult. See, while the technology is developing at a very fast pace, adoption levels are lagging behind.

We need to go beyond these misconceptions and demonstrate how blockchain can bring benefits both in terms of new revenue streams and costs efficiency/processes streamlining. Similarly, understanding better the technology features like decentralisation and demonstrating with actual cases how it can reshape traditional delivery models and enhance user engagement. With this, the blockchain reputation will be positively impacted. Blockchain will also play a major role in augmenting the impact of other technologies such as AI and IoT.

Things are advancing. Major traditional players have moved beyond the wait-and-see mode and I am extremely bullish on the upcoming developments in 2020.