In this article, we dive into the EU Taxonomy for sustainable finance based on the 2021 report by the UNEP FI (United Nations Environment Programme Finance Initiative), and the European Banking Federation (EBF). We are especially focusing on the Taxonomy in banking.

Given that most companies are at different stages on their journey towards sustainability business alignment, the UNEP FI and EBF sought to focus on it and support the development process. Because the individual commitment of banking organisations is of crucial importance to move towards the alignment, we’re briefly summarising the recently published report and examining it from a practical point of view.

The EU has already committed itself to achieving sustainability. The current EU Taxonomy ties in with this. It ultimately intends to ensure more transparency in sustainability matters across the block. For banks in particular, such new regulations require a sizable transformational work, which they will have to face up to.

The EU banking sector has the potential to be pivotal in the European economy transition towards a carbon-neutral society. It is evident that banks account for about 80 % of the external financing of the EU economy which, among others, underlines their importance.

As part of this transformation process, it became clear that banks see the EU sustainability agenda as an opportunity to further promote the sector’s role in society while aligning interests and strategies with customers, investors, employees and society at large.

When doing so, they see climate change as a global challenge that requires a global response. At the same time, they understand that market positioning and securing the competitive stand are essential and must be mastered.

The current global pandemic and the subsequent economic crisis have made addressing this challenge more urgent. One aspect is already certain today: the EU Green Deal will ultimately change entire sectors and the EU economy. And, as an aftermath, rapidly changing business models require flexible capital solutions.

What the current EU Taxonomy Regulation does is setting a framework for companies to define sustainable activities. And, naturally, banks are also affected by this and called to play an important role in the shift towards sustainability , for instance, by advising and promoting businesses on how to embed sustainability aspects in their capital structure and by developing suitable financing instruments to support existing and new sustainable activities.

How the EU Taxonomy can be applied to core banking products

As part of advising companies on sustainability aspects linked to their capital structure, banks usually offer suitable products and services. It is precisely these products that can be labelled as ‘sustainable’ following consensual and standardised taxonomy. This is important for economic reasons and necessary for banks’ sustainability disclosures in accordance with the EU Taxonomy Regulation.

With this in mind, the EBF and UNEP FI launched a project to assess to what extent and how the EU Taxonomy for banks is applicable to core banking products.

About the EBF and UNEP FI Project

The project asked 26 participants (banks) to review how their existing approach to sustainable finance could benefit from or be challenged by the upcoming introduction of the EU Taxonomy. Using more than 40 current or recently completed transactions, they tested the EU Taxonomy criteria. As a result, the EBF and UNEBEP FI shared key findings on the application of the EU Taxonomy that impact key banking products, namely retail banking, lending to small and medium-sized enterprises (SMEs) and corporate banking, including trade, export and project finance.

Results prompted that the focus is on the benefits and challenges that banks experience when applying the EU Taxonomy to core banking products. Participants in the project also suggested overarching practice principles to follow when applying the EU Taxonomy to retail banking, SME lending and corporate banking, including trade, export and project finance.

The result of the project is a series of recommendations to guide legislators, governments, regulators, industry standard owners and finally the banks themselves. It’s important to note that although the project’s report reflects what the majority of banks involved think, a number of banks have no intention to apply the EU Taxonomy beyond its strictly prescribed scope.

Applying the EU Taxonomy

The EBF and UNEP’s project outcome suggests the following points that core banking organisations should take into account when embracing the EU taxonomy.

Define the use of proceeds—profits or returns from a sale, investment—of the loan or credit facility;

When the use of proceeds is not specified, classify exposure on the basis of clients’ business activities;

Decide into which Taxonomy category the transaction, activity or company falls – Mitigation, Adaptation, Enabling, Transitioning, etc.;

Meet TSC for Substantial Contribution strictly based on evidence;

Subject to a materiality judgement, DNSH (Do Not Significant Harm) and MSS assessments may rely on assumed compliance of clients and assets with relevant legislation. They may also rely on certification schemes and labels and require timing flexibility. In addition, there are other general recommendations in support of legislators, owners of standards and frameworks, labels and certification schemes and banks. See the table below:

Legislators

Take into account the specificities of core banking products which may limit a full application of the EU Taxonomy.

Ensure consistency and compatibility/comparability of criteria between the EU Taxonomy and other applicable legislation and regulations, including at national level.

Seek global alignment of taxonomies, facilitate international data collection and provide comparability mechanisms of criteria for applicability of the EU Taxonomy beyond EU borders.

Consider and seek to address the timing mismatch between corporate data availability and banks’ ability to apply and disclose against the EU Taxonomy.

Facilitate the collection and handling of data, through the development of tools to facilitate the application of the EU Taxonomy.

Owners of standards and frameworks, labels and certification schemes

Clarify alignment with the EU Taxonomy.

Banks

Start methodical data collection for taxonomy-relevant information as part of new origination, on a best effort basis, based on internal strategy and priorities.

Banks

Devise industry guidelines for the implementation and application of the EU Taxonomy to core banking products, in conjunction with relevant industry bodies.

The demand for green/sustainable financial products is constantly increasing today and banks’ prompt response to this new realm is self-evident, however, the challenge is to remain relevant and compliant with stricter and more extensive regulation.

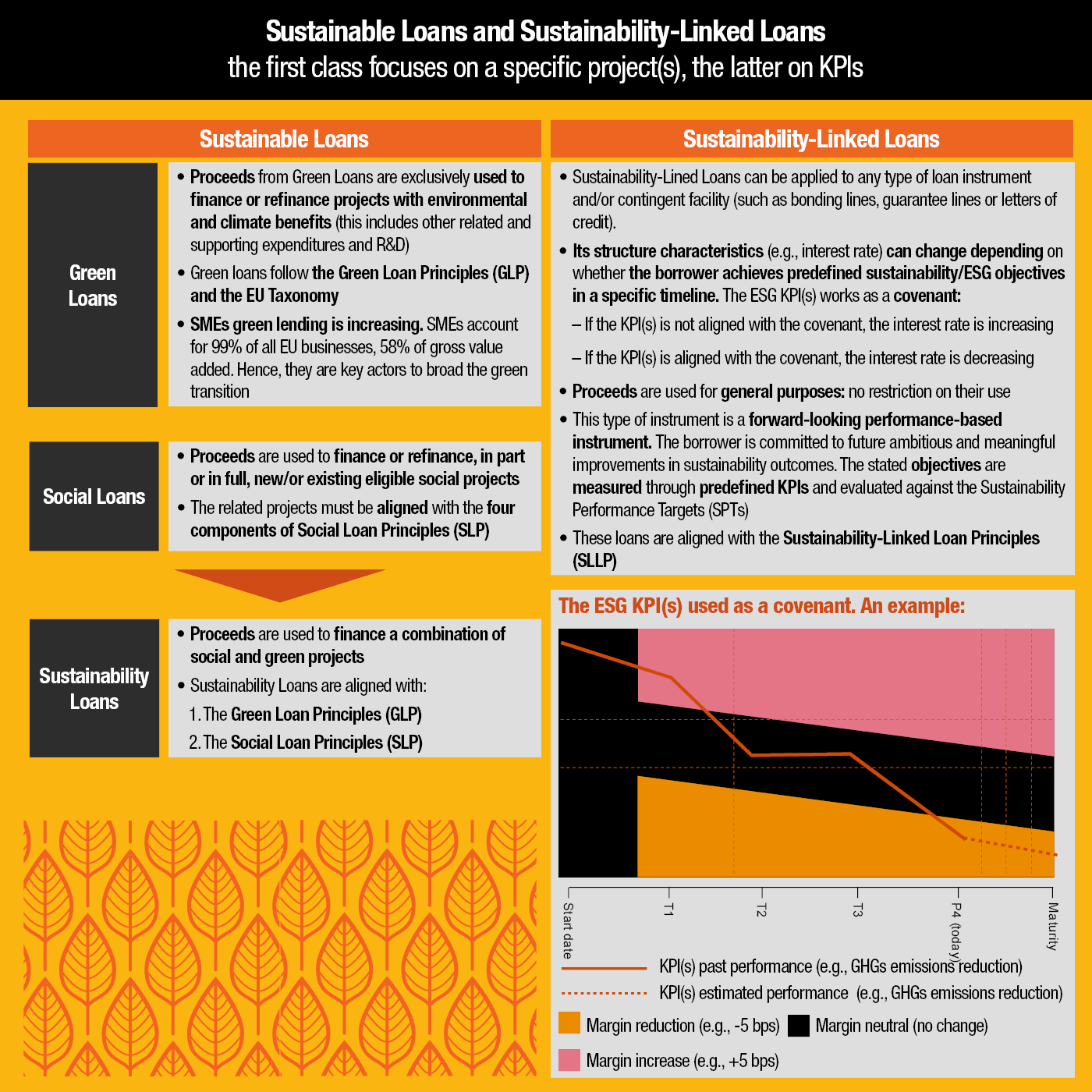

The so-called ‘Sustainability-linked Loan Principles’, for example, have been developed to facilitate and support environmentally and socially sustainable economic activity and growth.

The primary objective of these principles is to promote and preserve the integrity of the sustainability-related loan product by providing guidelines that capture their fundamental characteristics. And, ultimately, it’s about promoting sustainable development in a sound and clear way.

To give you a detailed example of a sustainable product, we thought it is worth focussing on sustainable-linked loans.

The following infographic illustrates the need to distinguish between different types of sustainable loans. Especially for sustainability-linked loans certain key performance indicators (KPIs) are taken into account here e.g. Greenhouse-Gas (GHG), that are used in order to determine the corresponding sustainability indicators.

In practice, this means a double incentivisation based on the following:

A specific ESG criteria is defined as a KPI – for example, GHG emissions;

Then a target for GHG is set or a target corridor is agreed with the customer;

If the target is reached, the interest rate remains the same or decreases – positive for the client;

If the target is not reached, the interest rate is adjusted upwards – positive for the bank.

The positive influence of the EU Taxonomy on banking

Even though the wider application of the EU Taxonomy isn’t fully applied yet, there are benefits associated with it that are already influencing positively the entire banking landscape.

Banks generally consider the EU Taxonomy as a beneficial initiative to foster and advance sustainable finance because of the consistency and greater transparency it brings into the industry.

The majority of the institutions are of the opinion that common definitions will improve their approach to managing all aspects of environmental, social and governance (ESG), including the way to interact with customers.

That the application of the EU Taxonomy will benefit the overall reputation of the industry by mitigating the perception of greenwashing is undisputed. Ultimately, most banks welcome clear guidelines in identifying green assets, setting targets and aligning their long-term business strategies and models with the transition to sustainability.

The downside of the coin

Because coins unavoidably have two sides, there are also disadvantages or, more accurately, challenges that the implementation of the EU taxonomy framework poses to banks. In particular, the application to retail loans, trade finance transactions and general-purpose put banks to a tough test.

According to the project run by EBF and UNEBEP FI, the availability and quality of data and information proved to be the most difficult challenge when assessing the so-called DNSH criteria. This, especially in the segmentation of the alignment based on turnover/revenue and in the alignment of SMEs and non-EU resident companies.

Not to mention that banks anticipate operational complexities when assessing and classifying multi-sector clients, coping with increasing documentation requirements and modernising IT processes.

In conclusion, the primary aim of the project was to develop a practical understanding of the applicability of the EU Taxonomy to banking products and to generally test the practical application.

Since the results were, overall, encouraging, banks should now move on to the next phase and focus on the development of guidelines and methodologies. The focus on possible cooperation with sustainable finance/ESG platforms and other stakeholders seems advisable in order to support the implementation of the given recommendations.

A sustainability-linked product shelf already plays an essential role in banking. The transformation process towards sustainable finance is gaining momentum and institutions need to react today to avoid the customer churn of tomorrow.

Daniel Theobald, Senior Manager, Banking Advisor at PwC Luxembourg

Especially in the lending business of banks, entirely new business models are arising, because so-called sustainability agents advise customers on how to deal with sustainability as a corporation and even support them in choosing the right KPI as a covenant.