The crypto-assets market has experienced an impressive growth over the past year and made the headlines quite a few times. While crypto-assets are still taking their first steps compared to other asset classes, they have undergone an incredible transformation since the creation of bitcoin in 2008, evolving from a niche market, consisting mostly of IT-savvy early adopters, to a global phenomenon amassing 1.7 trillion dollars for cryptocurrencies (as of this writing).

This blog article looks into the crypto-assets regulatory framework at global, European and local levels, and examines Luxembourg’s crypto-assets industry, highlighting five key facts drawn from a recent market study.

Don’t have time to read the whole blog entry? Then watch our “Blog in 1 minute” video for a quick summary of its main points:

An overview of the crypto-asset regulatory framework

With the rising popularity of crypto-assets comes scrutiny too. More specifically, regulatory scrutiny. It goes without saying that the regulatory environment around crypto-assets is still a fractured one and doesn’t yet provide the level of investor protection that other asset classes do. This, in turn, may be hampering the development of a congruent European crypto-asset market and reinforces the perception that crypto-assets are a risky, speculative investment.

Although this perception isn’t completely unfounded—the Financial Stability Board, the international watchdog that monitors financial authorities in 24 countries, has warned that the flourishing crypto market could pose a serious threat to the stability of the global economy— a prompt response from regulators can counter its current structural vulnerabilities. Regulators are taking action, however it could come, to a certain extent, “too little, too late”, or rather, too fragmented.

Europe’s regulatory framework on crypto-assets

At European Union level, the European Commission’s proposed Regulation on Markets in Crypto Assets (MiCA), which is part of the EU’s Digital Finance Strategy, is unquestionably a step forward towards a coherent and innovative-friendly crypto-assets regulatory framework. Expected to come into force within the next 18 months, it will apply to any individual or entity that issues crypto-assets or provides crypto-assets services. The goal is is to establish and enforce uniform requirements to the entire crypto-assets industry in the EU, with a focus on consumer protection, market integrity and financial stability.

As mentioned, MiCA is expected to come in one or two years’ time which could seem like an eternity in the crypto-asset space that evolves pretty quickly. Nonetheless, due to the latest geopolitical developments, which have put pressure on the legislative process, it could be here sooner than expected. Even so, the current situation begs the question: what happens between now and the application of MiCA? Well, some European countries, such as Switzerland, Germany and the UK, have opted to ratify their own regulations to seize the first-mover advantage with both hands.

Crypto-assets regulatory developments in Luxembourg

For instance, it clarified that Undertaking for Collective Investment in Transferable Securities (UCITS) funds and Undertakings for Collective Investment (UCIs) addressing non-professional customers and pension funds are forbidden to invest directly or indirectly in Virtual Assets. The document also outlines the conditions under which Alternative Investment Funds (AIFs) may invest in crypto-assets, as well as the requirements for the Alternative Investment Fund Manager (AIFM) and the specific Anti-Money Laundering (AML) considerations.

Lastly, in a FAQ document on virtual assets for credit institutions issued in January 2022 by the CSSF, the regulator states that credit institutions may directly invest in virtual assets and open accounts that allow customers to invest in virtual assets. On the other hand, credit institutions cannot open bank accounts in virtual assets, must submit a business case as well as an application file to the CSSF to provide virtual assets services and must set up an effective investor protection framework.

Cases around the globe

On the world stage, we witness different approaches to crypto. While El Salvador became the first nation to adopt Bitcoin as legal tender, India has reinforced oversight with strict tax guidelines and marketing rules on crypto-assets, and China went a step further and banned crypto altogether.

The United States (US), on the other hand, had been falling behind in the crypto regulatory space… until recently. There had been discussions on a wide-ranging oversight of the cryptocurrency market, including an executive order. They materialised into something more concrete on 9 March 2022, when President Biden signed the expected executive order on digital assets. This development is an important step as it sets the mood for how the US wants to handle crypto moving forward, and also—and perhaps more importantly—because it’s the first time a national policy is outlined in a whole-of-government approach with a precise agenda and due dates.

The executive order is beyond doubt positive for the US, but also for the entire crypto ecosystem as it may help thwart the narrative of the individuals who believed crypto was just a trend and would eventually fade away into oblivion. This, in turn, will further drive interest and capital to the crypto space globally, and can likely lead to other countries, including the Western ones, to accelerate their own crypto policy-making and regulatory frameworks.

Before this almost certainly game-changer development in the US, the Crypto-assets management survey (more information on this below) looked into the countries considered as the leading jurisdictions. Results show that Luxembourg isn’t considered a prominent actor (or at least not yet). On the other hand, and maybe not surprisingly, the US is—even though the country still doesn’t have a unified regulatory framework—followed by Switzerland and Hong Kong.

Click to enlarge | Source: “Crypto-assets Paradigm shift of short-term trend?” 2022

1, 2, 3, 4, 5 facts about crypto-assets in Luxembourg

This market study of Luxembourg’s crypto-assets industry looks into the drivers of growth as well as the opportunities and challenges to help Luxembourg market participants in their decisions on how to approach this innovative and disruptive asset class.

We share with you five key findings from the study:

1. Mixed feelings

There’s a mix of enthusiasm and hesitation around crypto-assets within Luxembourg’s financial services landscape. On the one hand, 18% of respondents already consider crypto-assets as a strategic priority for their business, while 43% expect them to become a strategic priority in the coming two years.

Additionally, 39% see some potential on crypto-assets from an investment strategy standpoint, while 28% see high potential. On the other hand, a significant portion of respondents remain hesitant, with 39% having no real plans to engage in crypto-assets activities for the time being.

Click to enlarge | Source: “Crypto-assets: Paradigm shift of short-term trend?” 2022

Click to enlarge | Source: “Crypto-assets: Paradigm shift of short-term trend?” 2022

2. Attractiveness

When asked about the most attractive crypto-assets features from an Asset Management perspective, respondents mainly agreed on its innate diversification potential, with 77% of them highlighting it as the most valuable attribute.

Other attributes such as the asset class’ inflation hedging properties and the risk-adjusted return potential have also been recognised by 38% and 23% of respondents, respectively.

Click to enlarge | Source: “Crypto-assets: Paradigm shift of short-term trend?” 2022

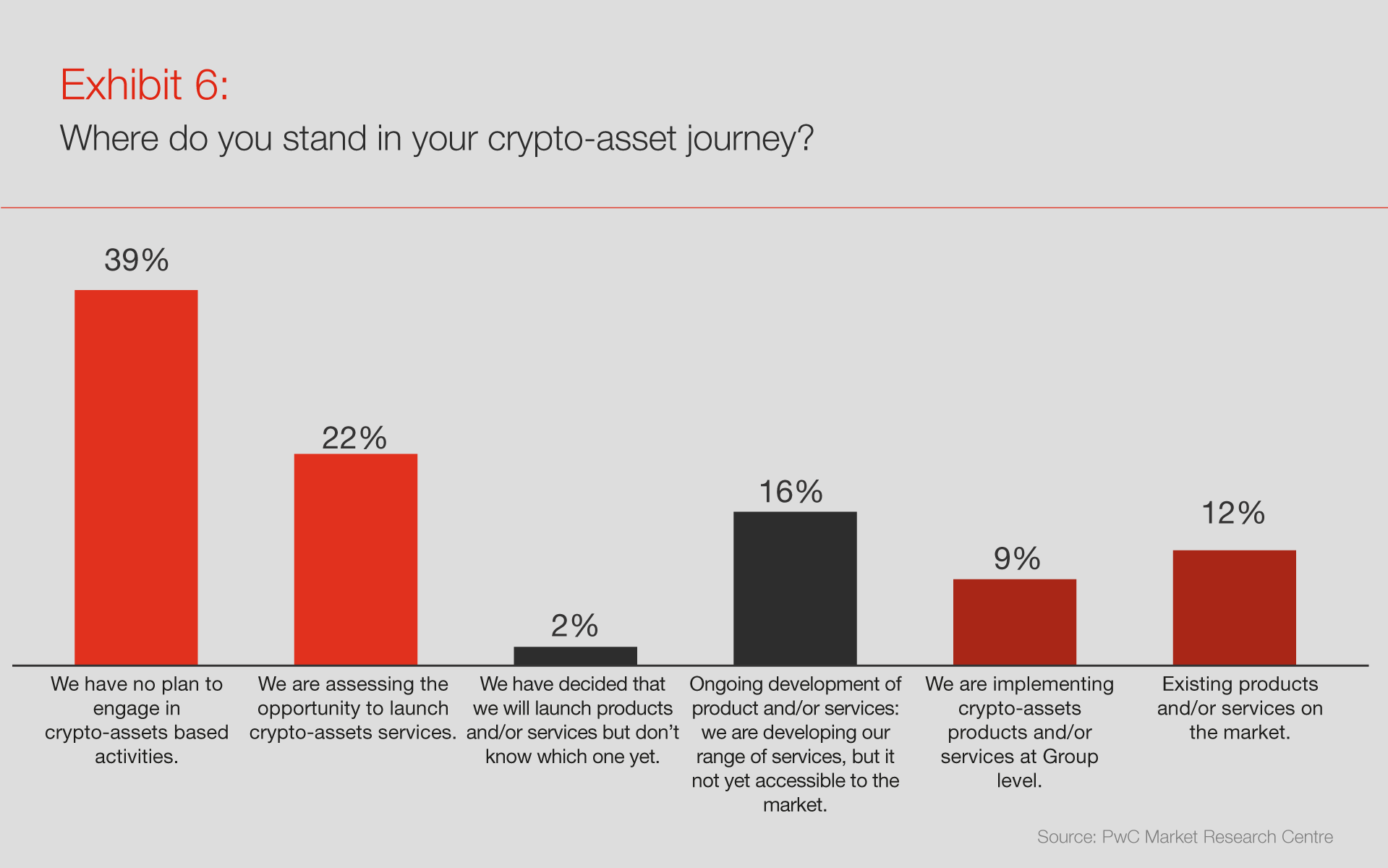

3. Readiness

The level of maturity varies greatly across surveyed entities, however a majority of respondents (61%) said they are embarking or planning to embark on their crypto journey—either assessing, developing or already providing crypto-asset products or services. That said, 22% are still assessing the opportunity, while 39% have no plan to engage in the asset class.

Click to enlarge | Source: “Crypto-assets: Paradigm shift of short-term trend?” 2022

4. Vehicles

When it comes to the type of vehicles, 70% of respondents see alternative funds as the most appropriate structure for crypto-assets, while 65% would favour unregulated structures. This overwhelming preference over ETFs or UCITs, echoes, to some extent, the regulatory uncertainty or vacuum that currently exists in the crypto space.

Click to enlarge | Source: “Crypto-assets: Paradigm shift of short-term trend?” 2022

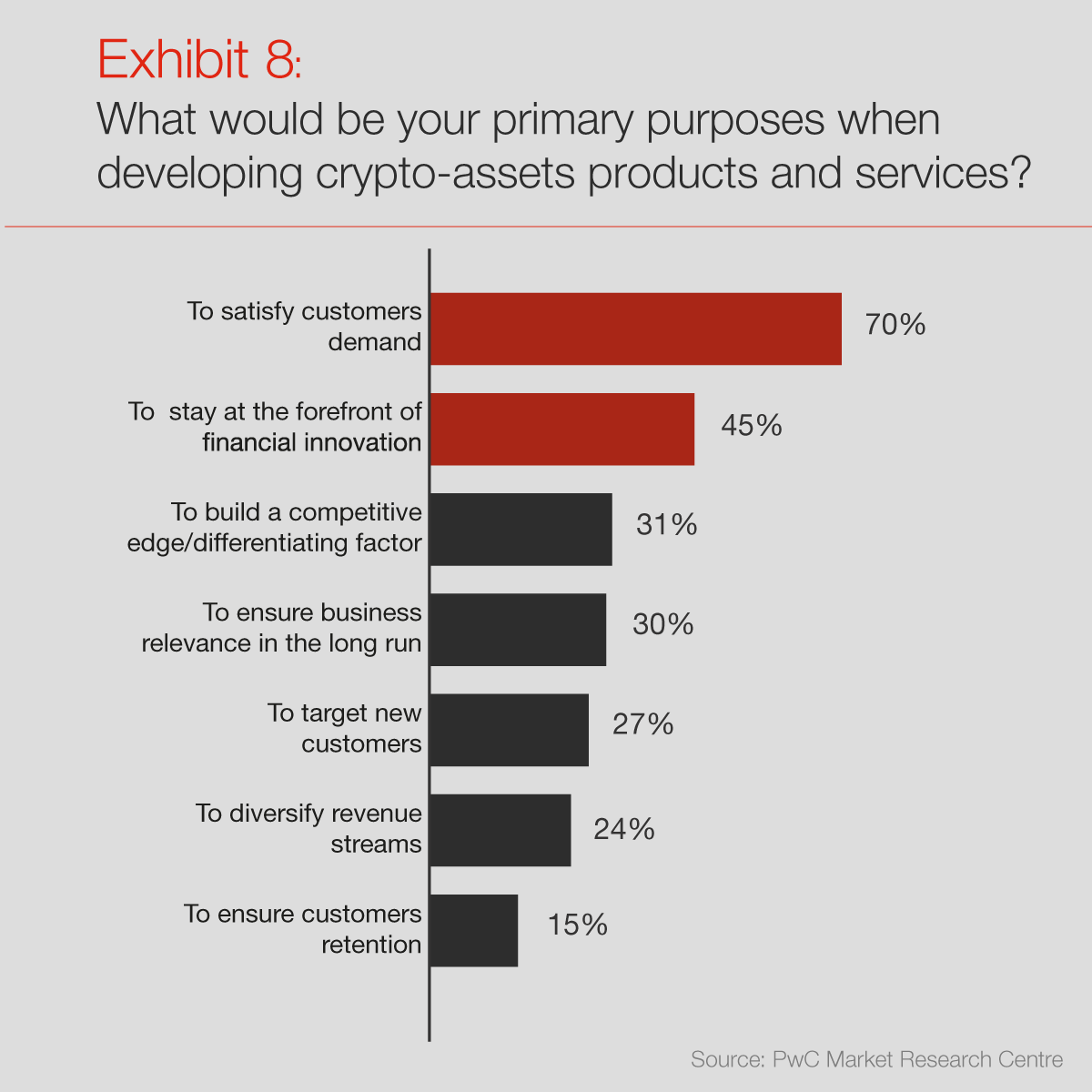

5. Motivation

How developed a country is in terms of crypto-assets depends not only on the number of active players in the field, but also on the level of demand.

Perhaps unsurprisingly, the respondents of the survey confirmed this view, as 70% of them affirmed that customer demand satisfaction is the main driver behind the development of crypto-asset products.

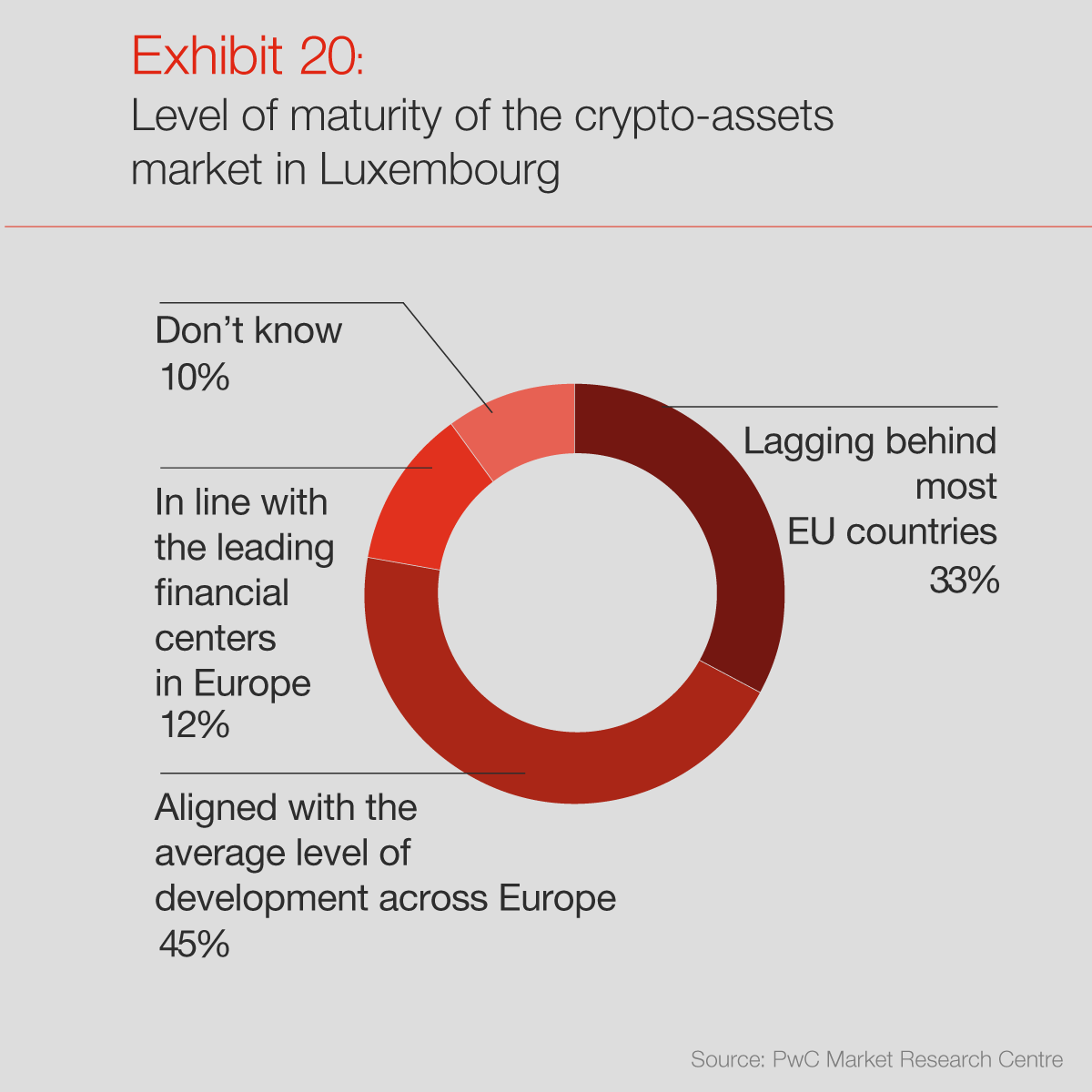

In Luxembourg, this demand, however, is seen to be rather limited or inexistent by 74% of respondents. This could explain why most also consider Luxembourg to be aligned or lagging behind other countries in terms of crypto-assets development. It could also explain why 39% haven’t engaged yet in crypto-asset related activities.

Other reasons to develop crypto-assets products include to stay at the forefront of financial innovation (45%), and to build a competitive edge (31%).

Click to enlarge | Source: “Crypto-assets: Paradigm shift of short-term trend?” 2022

(Click to enlarge | Source: “Crypto-assets: Paradigm shift of short-term trend?” 2022

The global crypto-assets industry is undeniably expanding rapidly and the numbers show it: there were almost 300 million crypto owners around the world as of December 2021, compared to only 100 million in January 2021, and this number is expected to reach 1 billion by the end of 2022.

However, it’s clear that this growth isn’t yet uniform, varying greatly across regions, industries and investor types. For instance, retail investors have been showing a great appetite for crypto-assets, while their institutional counterparts have been far more cautious due to the existing regulatory challenges.

Given today’s context, what the future holds for the crypto-asset space may not be entirely clear yet, but there are some clues. What we do know is that this future largely depends on if and how the challenges the industry faces—namely, regulatory fragmentation, lack of clarity on mainstream energy and AML concerns, the perception of the sector as opaque —will be addressed and surmounted.

In other words, to bet wholly on crypto-assets, financial players will first need a regulatory environment which gives them a degree of protection and certainty comparable to that of more established asset classes.

As the report points out, if Luxembourg players want to grab the crypto-asset opportunity and position the country at the leading edge of this industry, there are a few steps to take:

Authorities want to keep a continuing dialogue with market players to stay up-to-date with industry needs and trends, and provide support as needed.

Stakeholders want to enhance coordination and cohesion, not only between incumbents and traditional players but also through public-private initiatives.

Develop the appropriate financial education of crypto-assets so that both investors and market participants can effectively weigh the challenges and opportunities of this rapidly evolving field.

What we think

Thomas Campione, CFA Blockchain and Crypto-assets leader at PwC Luxembourg

While markets have been turbulent lately, looking at the global picture and the industry structural developments, I expect 2022 to be a pivotal year for the crypto-assets management industry. It is critical that Luxembourg and the broad financial industry embrace the topic and do not stay away from the conversation because of contradictory signals.