The PRIIPS Kid is undeniably a good idea. But will it deliver as expected?

Packaged retail investment and insurance products (PRIIPs) include all publicly marketed financial products that have exposure to underlying assets—stocks, bonds, etc.—that provide a return over time, and have an element of risk.

Or, to put it in simpler words, it’s what banks and other financial institutions in the European Union offer to consumers when they want to save for a specific objective such as a house purchase, obtain a master’s degree or for a child’s education. One could say that it’s a different way to save money to achieve a single goal or a set of goals linked to a tangible outcome.

According to the European Commission, the PRIIPs market is worth up to €10 trillion. They are essential to funnel investment from citizens (retail investors) to the real economy.

PRIIPs, however, aren’t precisely easy to digest. Often overly complex, the information that financial institutions make available to retail investors tends to contain abundant industry jargon and doesn’t make it easy for them to compare between different investment products.

Could this complexity lead to misleading advice? Needless to answer, the fact that the financial institutions are both sellers and advisors likely leads to conflicts of interest.

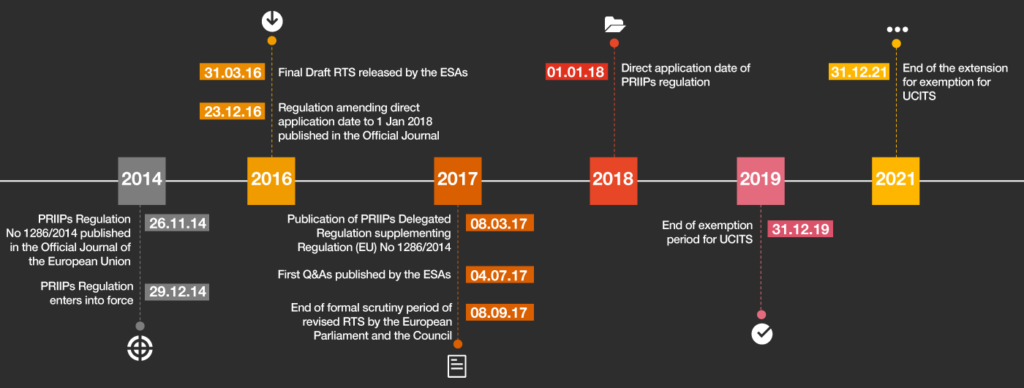

Five years ago, what’s commonly known as the PRIIPS regulation was published. Officially coined with the No 1286/2014, the text appeared on 9 December 2014 in the Official Journal of the European Union.

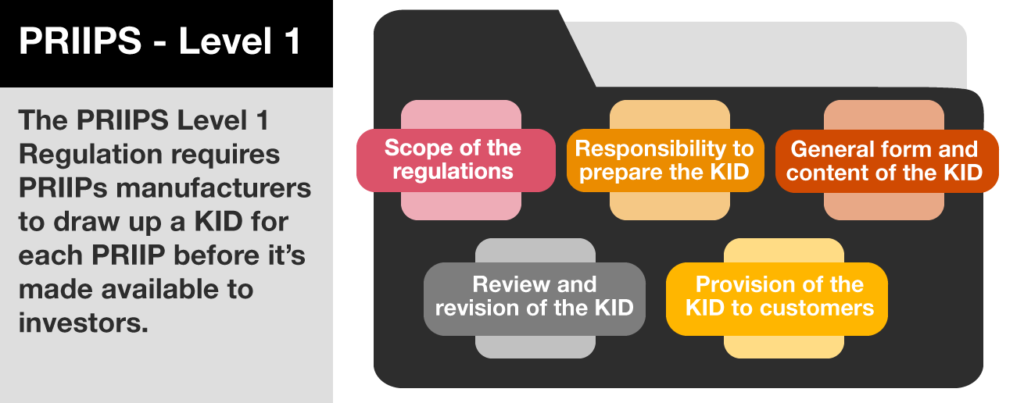

With the aim of enhancing investor protection standards for retail clients and increase transparency in the market, the PRIIPs regulation targets both PRIIPs’ product manufacturers and distributors who have to prepare a KID (Key Information Document) for each product defined as PRIIPs.

But the recompense of goals with unambitious challenges is often times flavourless. Since the PRIIPs Regulation direct application at the beginning of 2018, the road hasn’t been precisely smooth and several issues have arisen. As a consequence, The European Supervisory Authorities (ESAs) launched a consultation paper in late autumn the same year and the process hasn’t yet concluded. ESAs gather the European Banking Authority (EBA), European Securities and Markets Authority (ESMA) and European Insurance and Occupational Pensions Authority (EIOPA).

The purpose of this article is to revise the why, the what and the how of the PRIIPS KID project to reflect on whether this well-intentioned idea can deliver as intended. And in case it isn’t possible, we want to dig deep into the roots.

PRIIPS KID timeline

The KID’s Echography

Let’s go back to the basics first.

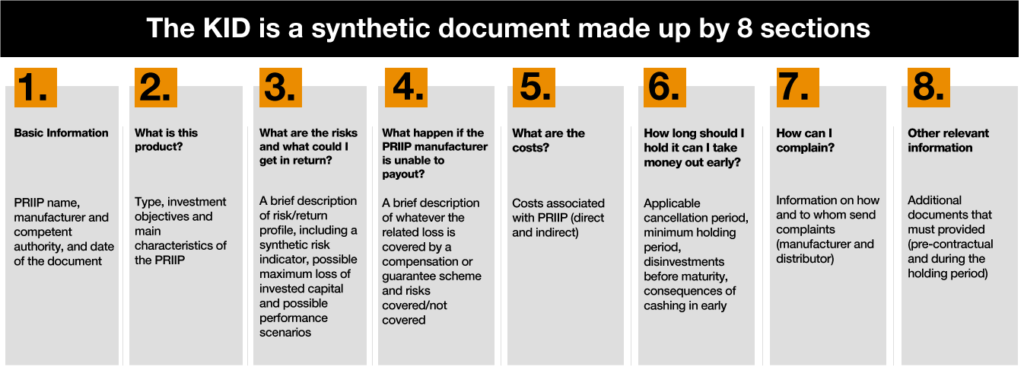

A KID, simple by definition, requires investment products to be explained in plain language. It contains information on costs, risk rating and investment profile—potential gains and losses of one’s chosen investment product. Product manufacturers have to divulge this information through their corresponding website before distribution.

A KID is a piece of content that wants not only to transfer information but to educate investors so they can make convenient investment decisions.

When you wish to instruct, be brief wrote Cicero, the famous Roman orator, more than 2000 years ago. But for a KID to fulfill its purpose, good intentions aren’t enough. Prior to that, the PRIIPs regulation has to get around many challenges and fight the wave of criticism.

After almost two years of directly applying the PRIIPs regulation, has it really improved the disclosure of the investment products within its scope? Conceived in the previous decade (2009), the regulation needs to address issues such as how UCITS manufacturers will comply with the law or how understandable and compelling KIDs really are for retail investors.

MIFID 2, PRIIPs and UCITS, tête à tête

The PRIIPS Regulation is the MIFID 2 of retail investors, they say. In fact, the former is consistent with the Markets in Financial Instruments Directive—MiFID 2 and Insurance Distribution Directive—IDD, whose joint aim is to recover investors’ trust in the financial markets.

Similar in spirit, but different in scope in terms of the types of funds and products they target and the moment when the investment information must be issued, both the PRIIPs and MIFID2 are undeniably aligned.

The “affair” PRIIPs/UCITS—please, allow us to call it that—is a bit different though.

The existing UCITS Directive (2009/65/EC) contains a requirement for Key Investor Information Documents (KIID) which are like those of KIDs. For this reason, the European Commission gave a temporary exemption to manufacturers and persons selling units of UCITS funds or advising on them.

Due to expire on 31 December 2019 originally, a period during which they would be exempted from the PRIIPs regulation terms [see article 32 (1) of Regulation (EU) n° 1286/2014], the date has been extended for two more years until 31 December 2021. Those manufacturers and persons, then, will apply the Regulation as of 1 January 2022.

This extension is the result of a targeted review of the PRIIPs Delegated Regulation that the ESAs initiated in autumn of 2018. This regulation, adopted on 8 March 2017, supplemented the original one from 2014.

More recently, the ESAs have released a Consultation Paper that proposes amendments to the PRIIPs Delegated Regulation of 2017. The current consultation will lead to a review that likely won’t be the last, not only because this is a work in progress, but also because the outcomes of the so-called consumer-testing exercise will not be available until mid 2020.

The consumer-testing exercise aims to identify a user-friendly format that consumers understand, with clear information to compare and choose investment products that best suit their interests. The sample included all countries in the EU.

What fund product manufacturers and distributors need is regulation alignment because the regulatory burden seems like an endless tunnel whose toll tariffs aren’t cheap. Could the one-size-fit-all approach of the PRIIPs regulation work, after all?

The KID on the divan

Let’s dissect the nature of the KID by asking three basic but clarifying questions: why, what and how. You can think of it as a sort of introspective trip to the spirit of the regulation.

Why the KID?

There were two sets of objectives or ambitions embedded in the project, one of individual nature, the other of general. Indeed, developing a KID would allow, on the one hand, for comparability of similar products. On the other, it would serve as a tool to enhance the retail investors’ understanding of such products and their embedded features.

On top of that, it would enhance the practical development of the EU Single Market, an ambition of particular relevance to Luxembourg.

What’s the KID?

Detailedly explained in the section The KID’s Echography (see above), we would like to add that this document isn’t aiming to replace but to complement, existing relevant (and detailed) investment information, both contractual and pre-contractual.

How the KID does it?

The KID was built upon two assumptions. “Too much information kills information”, is the first; “some information is a “must have”, is the second. Indeed, the KID’s purpose is to be a consumer-friendly three-page investment document.

To do so, regulators ran different tests. The agreed methodology introduced not only performance scenarios, but also elements of behavioural economics. For instance, the risk level scoring risk, currently in different shades of grey, was originally designed with the colours of a traffic light. But, because such an approach would trigger a consumer bias leading to relate the green colour with no-risk investments, it changed later on.

But “the proof of the cake is in the eating”, the saying goes.

There were good ingredients to start with, but two years of the PRIIPs regulation application have shown that, in reality, the KID is too complicated for many end users. On top of that, because UCITS manufacturers can use the pre-existing KIID, thanks to an exemption period, full comparability has not been achieved when it comes to disclosure of costs.

Similarly, there are exogenous factors such as social change we should consider too. Many new retail investors access information via portable devices such as smartphones. Is the three-page KID based on paper tackling this reality? Obviously not.

Challenges remain, both scope and breadth related. From the fact that some products seem to simply not fit in (so, what can we do about them?) to the provision of useful information on performance and the scenarios around it.

Regarding the latest, the use of past performance could lead to unrealistic expectations of return, in particular within a world of negative rates. Indeed, in this case, contrary to what Lord Byron said, “the past is (NOT) the prophet for the future”.

Documented behavioral basis makes us be overly optimistic. For instance, thinking that the 4% return obtained during the last 10 years can be replicated in the near future is unlikely to happen under current market conditions.

Other challenges are less obvious, yet must be addressed, including the need or not to change the Level 1 text in order to be able to achieve intended objectives.

If this is the case, let’s not shy away and do it!

What we think

Carlos Montalvo Rebuelta, EMEA Insurance Risk and Regulatory Leader

Feasibility is a precondition for an idea to be deemed good… so let’s get the PRIIPs-KID project done. We can! It’s worth both the try and the expected success.

Anthony Dault, Audit and Advisory Insurance Partner at PwC Luxembourg

More than ever, conduct should be a priority for insurers and intermediaries. It will drive customer confidence and trust, and ultimately loyalty, to a higher level. It should not be jeopardised through an imperfect three-page document. Get your KIDs right, this is part of conduct!