“The only way to stop the flow of this dirty money is to get tough on the bankers who help mask and transfer it around the world. Banks themselves don’t launder money, after all: people do.”

Robert Mazur, former federal agent who worked as an undercover money launderer

In recent years, money laundering and terrorist financing have been a key area of focus for both regulators and financial institutions across the globe. In the face of rampant criminal activity, global financial institutions spent $181bn on financial crime compliance worldwide in 2019, with European firms spending three to four times more than their counterparts in North America. In the same year, global enforcers imposed more than $8bn in anti-money laundering fines, almost double the amount in 2018 ($4.27bn). 12 out of the world’s top 50 banks were fined in 2019. Eight months into 2020, this trend has continued.

Despite ballooning financial crime compliance costs and fines, the staggering magnitude of money laundering and terrorist financing activities remains. The United Nations Office on Drugs and Crime (UNODC) estimates that the equivalent of 2% to 5% of the world’s GDP, or $800 billion to $2 trillion, is laundered annually. In Europe, the value of suspicious transactions is in the hundreds of billions of euros, according to Europol approximations, while the European Commission estimates that around 1% of EU’s annual GDP, or €160bn, is involved in money laundering and terrorist financing.

By now, it’s become clear that the impact of money laundering and terrorist financing activities is severe and extensive, and affects businesses, economies and societies locally and globally. The 2020 mantra of the Financial Action Task Force (FATF) – “Stop money laundering, save lives” – is indicative of the seriousness of the threat and the urgent need of a potent response.

In this article, we discuss how the global fight against money laundering shares the political agenda of the EU in 2021 and why that’s key to the success of anti-money laundering (AML) and counter-terrorist financing (CTF) efforts.

EU Response: Coherence is key to effectiveness

Recently, the EU institutions have started a renewed effort to crack down on money laundering and terrorist financing. This was done in the aftermath of a series of scandals that shook the EU’s financial sector in the past few years, exposing patchy enforcement across its Member States. The urgency of an adequate reaction was intensified by the COVID-19 pandemic. As Internet usage grew due to lockdown measures,it brought an increase in criminal activities such as cybercrimeand virtual money laundering.

The EU’s renewed focus on money laundering and terrorist financing materialised into the creation of a comprehensive Action Plan that the European Commission adopted on May 7. The Plan outlines concrete measures to be taken by the Commission over the next 12 months to ensure effective supervision, enforcement and coordination of AML and CTF regulations across Member States. In addition, it aims to strengthen the EU’s global role in tackling these criminal activities.

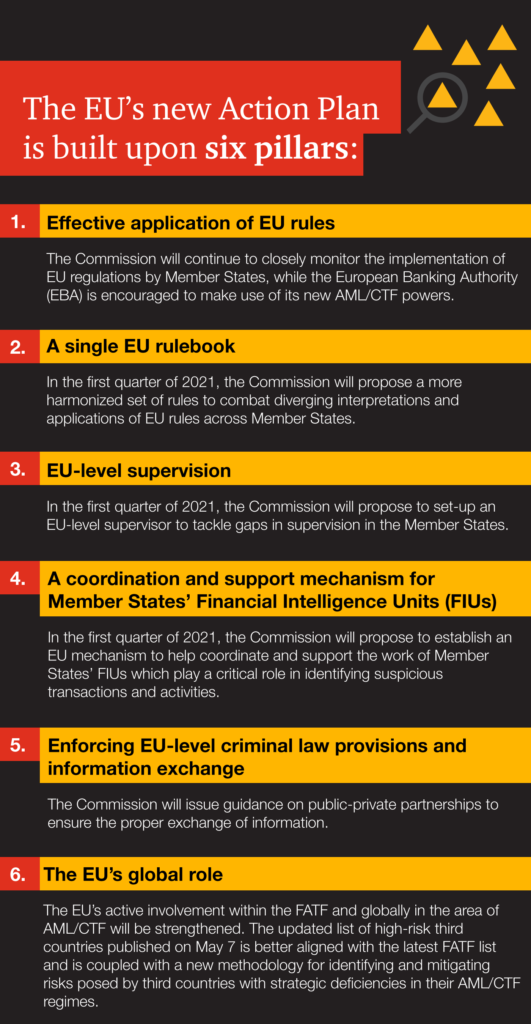

The EU’s new Action Plan is built upon the following main pillars:

1. Effective application of EU rules: The Commission will continue to closely monitor the implementation of EU regulations by Member States, while the European Banking Authority (EBA) is encouraged to make use of its new AML/CTF powers.

2. A single EU rulebook: In the first quarter of 2021, the Commission plans to propose a more harmonized set of rules to combat diverging interpretations and applications of EU rules across Member States.

3. EU-level supervision: In the first quarter of 2021, the Commission will propose to set-up an EU-level supervisor to tackle gaps in supervision in the Member States

4. A coordination and support mechanism for Member States’ Financial Intelligence Units (FIUs): In the first quarter of 2021, the Commission will propose to establish an EU mechanism to help coordinate and support the work of Member States’ FIUs which play a critical role in identifying suspicious transactions and activities.

5. Enforcing EU-level criminal law provisions and information exchange: The Commission will issue guidance on public-private partnerships to ensure the proper exchange of information.

6. The EU’s global role: The EU’s active involvement within the FATFand globally in the area of AML/CTF will be strengthened. The updated list of high-risk third countries published on May 7 is better aligned with the latest FATF list and is coupled with a new methodology for identifying and mitigating risks posed by third countries with strategic deficiencies in their AML/CTF regimes.

Building up greater AML competence at EU Level

The six pillars are not only centred around a more uniform implementation of the existing legal framework and better coordination between the authorities of the individual Member States, but also around the build-up of more competence at EU level. The message seems clear: financial institutions should get their AML/CTF policies in order, because these policies will be subjected to an increased level of scrutiny.

A resolution on a comprehensive AML/CTF strategy followed the publication of the Action Plan. The European Parliament adopted it on July 10. This resolution promotes a much stricter stance towards Member States who fail to transpose Anti-Money Laundering Directives (AMLDs) into national law within the specified deadlines. The resolution also encourages the consistent application of freezing and confiscation orders to streamline the process for recovering illicit funds across the Union.

In the adopted resolution, the Parliament reiterates the need for a transparent and robust methodology for assessing high-risk third countries with strategic deficiencies in their AML/CTF regimes. It also suggests a complementary “grey list” alongside the Commission’s revised list of high-risk countries, which will come into force in October 2020. Likewise, the resolution emphasises the importance of cooperation among FIUs, law enforcement and judicial systems across Member States and calls for interconnected beneficial ownership registers. Finally, it stresses the need for enhanced EU-level AML/CTF supervision and supports granting the European Central Bank (ECB) with independent powers to revoke the licenses of EU banks breaching AML/CTF regulations.

The European Court of Auditors to focus on AML/CTF

The European Court of Auditors (ECA) also joined the list of high-profile EU institutions that recently shifted their focus to AML/CTF. In June, the ECA announced that it has launched an audit of the effectiveness of the EU’s efforts to combat money laundering in the banking sector.

The focus of the audit is on:

a) The Commission’s assessment of the transposition of EU legislation into Member State law;

b) The assessment and communication of known AML risks to banks and national authorities involved in AML;

c) Coordination and information sharing at the Member State and EU level;

d) Actions in response to suspected breaches of EU AML legislation in Member States.

The audit has been included as a high-priority task in the ECA’s annual work programme for 2020 and the audit report will be published in the first half of 2021.

The recent measures implemented by EU institutions should also be analysed against the backdrop of Directive (EU) 2018/1673 (the Sixth AMLD), which was published on November 12, 2018, four months after the Fifth AMLD came into force. The Sixth AMLD, which must be transposed into Member State legislation no later than December 3, 2020, complements and reinforces the Fourth AMLD by laying down minimum rules on criminal liability for money laundering.

What we think

Birgit Goldak, Partner, Risk Assurance Services at PwC Luxembourg

“Events since the early 2000s have shown, and many sources can be quoted, that money is the oxygen of organised crime and terrorist financing. Dry out the cash and you mitigate the issue. This is much easier said than done. In recent years, the increased focus on the creation of rules for understanding business, understanding risk exposure to being misused for money laundering or terrorist financing and asking questions as to who is the true beneficial owner have helped to set the right direction of travel. The cost of compliance, albeit high, is lower than the cost of non-compliance and so the motivation of compliance is increasing concurrently.“