With more than 200 active reinsurance captives, the Luxembourg financial centre is considered the European leader in the market. This is mainly due to its stable legal, regulatory and tax framework—confirmed by the maintenance in 2022 of Luxembourg’s AAA financial rating—as well as the highly qualified international professionals and specialists that are part of the country’s workforce.

In this blog, we aim to show you why captive reinsurers want to apply the International Accounting Standard for Financial Information, or in short IFRS 17, and how it contributes to the better management of these entities. We also outline some methodological simplifications for a less costly implementation in terms of time and resources.

Don’t have time to read the whole blog entry? Then watch our “Blog in 1 minute” video for a quick summary of its main points:

But before we jump into that, let’s briefly explain to you—or refresh your mind on— what a captive reinsurance company is.

Reinsurance captives in Luxembourg

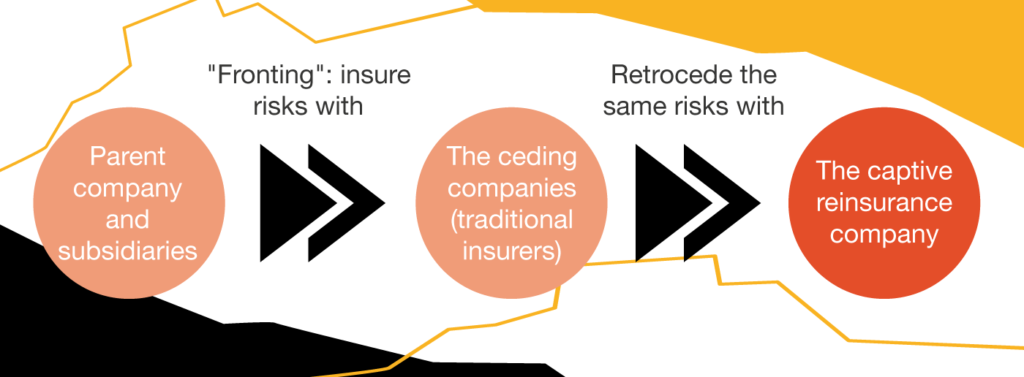

A captive reinsurance company is a company whose main role is to cover the risks arising from its parent company—generally a multinational industrial or commercial group—and its subsidiaries via fronting operations—that is, the implementation of insurance cover—with traditional insurers, ‘the ceding companies’.

The classic operation of a reinsurance captive can be schematised as follows:

The advantage of this ‘intra-group’ insurance operation is twofold:

It guarantees effective risk management through a better assessment of the risks covered, due to the absence of moral hazard, adverse selection or various frauds;

It enables better management of intra-group cash since a portion of net premiums and equity remains within the group, in particular through cash pooling or intra-group loans.

The captive market is growing mostly because traditional insurance is proving to be unsuitable for covering very specific and extreme risks, such as cyber, climate and pandemic risks, which unfortunately increasingly tend to normalise.

This also applies to coverage unavailable on the standard insurance market or that’s too expensive, such as coverage of the overall balance sheet or key-person risks. In addition, the mechanism of the provision for fluctuation of claims (PFS) plays a decisive role, particularly in tax terms.

Why should captives apply IFRS 17?

Let’s get down to brass tacks. The IFRS 17 was published by the International Accounting Standards Board (IASB) in 2017 and adopted in 2021 by the European Commission.

In force since 1 January 2023, it aims to provide a true and fair view of insurance contracts through a better evaluation of cash flows. It allows to harmonise the way in which insurance contracts are accounted for and presented in the financial statements, and therefore facilitates comparability between the different companies.

The truth is, the implementation of the IFRS 17 standard within insurance and reinsurance companies requires a considerable financial and operational investment.

Quite naturally, you may be wondering now about the application of this standard to organisations such as captive reinsurers given their size and financial means.

Indeed, taking into account the captives’ size—the majority have a balance sheet size of less than EUR100m—and especially the fact that it’s exclusively a matter of hedging intra-groups (‘self-insurance’), some market players believe that there is no need to apply IFRS 17, in particular for group consolidation purposes.

In addition, these market participants often refer to article B27(c) of the standard to justify the non-applicability to captive reinsurers. This article provides that for so-called self-insurance, that is, retaining a risk that could have been covered by insurance:

“(…) there is no insurance contract because there is no agreement with another party. Thus, if an entity issues an insurance contract to its parent, subsidiary or fellow subsidiary, there is no insurance contract in the consolidated financial statements because there is no contract with another party. However, for the individual or separate financial statements of the issuer or holder, there is an insurance contract.”

Nevertheless, in the case of a captive reinsurance company (see below), there is very often a third party involved, namely the fronting insurer, which, as we mentioned before, plays the role of the ceding company. Therefore, it’s a counterparty external to the group regarding the IFRS 17 standard, which is contractually liable vis-à-vis the insured—the parent company and subsidiaries—for the compensation of claims.

In addition, some captives also abate part of the risks accepted with specialised operators on the international reinsurance market. Hence, the interpretation of article B27 alone isn’t sufficient to exclude captive reinsurance companies from the scope of application of IFRS 17.

Notwithstanding this debate, we list below the advantages of applying this standard for captives.

Advantages of applying IFRS 17 for captives

Going beyond the regulatory requirements, the IFRS 17 standard offers considerable advantages for the efficient and forward-looking management of reinsurance captives. We have summarised the main ones for you:

Theme

Advantages

Pricing

Better pricing of accepted and retroceded risks due to the fact that IFRS 17 provides future cash flows faithfully projected at market value. This can therefore lead to a better optimisation of fronting fees or retrocession commissions, and thus an optimisation of costs and commissions.

Reserving

Adequate claims provisioning for a better budget forecast. Indeed, IFRS 17 allows, through the calculation of the best estimate, to neutralise the usual volatility induced by the local Generally Accepted Accounting Principles (GAAP) statutory provisioning.

KPIs

Possibility to perform a precise calculation of Key Performance Indicators (KPIs) with the IFRS 17 standard, such as Return on Equity (ROE) or Return on Risk-Adjusted Capital (RORAC), thus promoting better monitoring and management of the financial performance of captives.

Consolidation

Better integration of the captive’s accounts into the IFRS consolidated financial statements of its parent company. This enables, among other things, increased transparency and comparability of the captive’s accounts with the other sister companies of the group.

Valuation

Better valuation of captives, particularly for mergers, acquisitions or sales operations.

Rating

Contributes to a better estimate of the parent company’s rating by financial rating agencies via an improved estimate of intra-group financial flows from the captive.

How can captives apply IFRS 17?

Now let’s outline some methodological simplifications that could be applied for a smoother approach to the standard. This could be achieved by exploiting the synergies with the Solvency II calculations.

Undeniably, given the small size of reinsurance captives and the operational complexity of implementing IFRS 17, the simplifications listed in the table below could be applied while respecting the fundamental principles of the standard:

Theme

Simplifications

Aggregation of contracts

For the IFRS 17 grouping of contracts, captives may consider Solvency II lines of business (LoB) by annual cohort.

Measurement model

Captives can easily consider applying the Premium Allocation Approach (PAA) method based on the elements of the Local GAAP statutory account. However, a case-by-case analysis needs to be carried out for multi-year contracts.

Contract boundary

Captives could consider more or less the same contract boundaries as Solvency II.

Discount rate

The European Insurance and Occupational Pensions Authority (EIOPA)’s interest rate curves, applying adjustments to take into account the duration of the assets of the EIOPA’s reference portfolio and the duration of the captive’s liabilities.

Financial cash flows

Reuse of the same cash flows as those of Solvency II, with some adjustments, especially regarding expenses.

Risk adjustment

Approach based on the cost of capital. For example, by applying an adjustment to the Solvency II Risk Margin.

To conclude

Despite the operational complexity, we strongly believe that all captive reinsurance companies should consider applying IFRS 17 with some simplifications and proxies based on materiality criterias. The advantages, as we outlined in this blog, are bountiful.

If asking all captive reinsurance companies to apply IFRS 17 is too ambitious, we think at least those whose parent company publishes IFRS consolidated accounts should go for it.

In addition to compliance with accounting and regulatory requirements, the application of IFRS 17 will also effectively contribute to better management of reinsurance captives and thus strengthen the solvency and financial condition of these entities over the long term.

Our experience in the reinsurance sector and particularly captives in Luxembourg allows us to measure the challenges and constraints that captives may encounter when implementing IFRS 17.

Applying IFRS 17 enables reinsurance captives to have the appropriate and precise tools to better assess the risks and the financial performance indicators of the company. Thus, IFRS 17 will go a long way in enhancing the primary role of captives as an effective intra-group risk management tool.

Timothée Muller, Manager, Actuarial and Risk Modelling Services at PwC Luxembourg

When reinsurance captives capitalise on the synergies with the Solvency II calculations, the implementation of the IFRS 17 standard could prove to be less resource-intensive and time-consuming.