Advising, identifying, instructing, acknowledging, processing, checking, confirming, monitoring, reconciling, reporting, storing, regulating, auditing – the fund-distribution value chain is complex and has many intermediaries. Distributed ledger technologies are, however, bringing about a new business model for the asset management industry.

Fund distribution as we know it

In the last 30 years, we’ve seen the self-revamp of the fund industry’s landscape many times. Its transformation has moved towards the increasing use of intermediaries, thus expanding the fund-industry network and its value chain. From an investor’s decision to invest in a mutual fund, to asset managers, many players (and their respective roles) get involved in the chain. The role of the transfer agent (TAs) has developed over time as a specialist in intermediation between two groups of players. We have, on one hand, the investors and distributors, and on the other hand, the fund and its asset managers and service providers.

In this context, TAs have developed a catalogue of services, such as identifying investors and distributors, transaction management, settling cash and fund shares, calculating distribution fees, and operational and regulatory reporting. Their challenges moving forward will be around:

Investor and distribution identification: time-consuming, manual and risky exercise.

Transaction management: lengthy, multi-step process, with a high risk of operational errors.

Cash settlement: an operational burden of reconciling payment instructions between several counterparties and the time required is usually a minimum of three days.

Reporting: data that exists but needs to be prepared and sent; TAs have to implement a reporting process that is both cost-efficient and convenient for their many different targets.

Distributed ledger technologies will help tackle TAs’ future challenges

Most commonly known as blockchain, distribution ledger technologies are high on the agenda of most of the players in the fund industry, and their adoption is in progress. Here’s how blockchain and smart contracts will reshape the fund-distribution value chain to make TAs’ lives easier:

Decentralised identification

We base our vision of the future AML/KYC process on different key players: trusted parties, identification blockchain and AML/KYC smart contracts. The whole model goes around the principle of “You own your own you”.

So, how will it work? Future investors will have direct access to a mobile transaction platform to perform any transaction into funds they’re willing and eligible to invest in. To gain direct access to the platform, they go through an identification process. Investors then follow a series of steps and receive a digital identity.

Disintermediate subscription process

In the new business model based on distributed ledger technologies, investors have access to the fund through their respective distributed ledger. Once furnished with a digital identity, they’re able to subscribe by simply using the associated smart contract and blockchain. The need for an intermediary disappears.

Who will drive this process forward? To run this business model, the fund and the investor must have a digital wallet, managed by smart contracts. The digital wallet contains, for both parties, an account for digital currency and digital assets. Smart contracts provided by distributors or platforms contain the fund characteristics and the investor’s eligibility criteria.

The model will, therefore, disrupt the omnibus account concept. Account management will become easier with single fund wallets or multi-asset wallets. Distributors will not actively intervene and investors will be able to initiate transactions by themselves, using either a platform or marketplace.

Digital decentralised settlement

The new business model decentralises settlement and makes it almost real-time. To make this work, all involved parties need a digital currency wallet. They pre-fill or fill on demand with the required amount to place and execute transactions on a blockchain. Once the Net Asset Value (NAV) becomes available and all of the smart contract’s checks are fulfilled successfully, payment and share settlement happen almost in real-time.

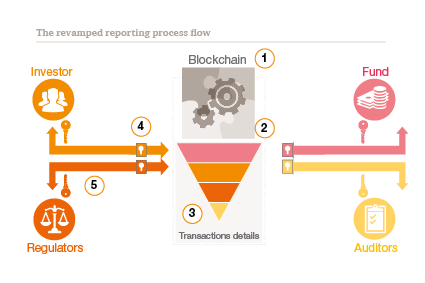

Real-time reporting

Implementing this business model makes reporting duties more efficient thanks to access to reconciled real-time data. As financial information is saved on the blockchain, there are no reconciliation issues. In addition, the database is unique and all participants have access to it, which eliminates mistakes and thus enhances data quality.

We can also customise access to data available on the blockchain. Investors and fund managers, but also regulators and auditors can thus directly access the reconciled data and perform reporting. Therefore, the new business model increases both transparency and investor protection.

Since each party accessing the distributed ledger goes through an identification process, its access to information can be customised. This is why distributed ledger technologies provide a high level of confidentiality. In addition, smart contracts help manage specific reporting requirements, which reduces the risk of calculation mistakes and human error.

Privacy of transactions

There are currently two secretive and emerging applications aiming to guarantee the privacy of transactions:

Quorum;

Enterprise Ethereum.

Private transactions: Transactions whose payloads are only visible to the network participants whose public keys appear in the “privatefor” parameter of the transaction. The “privatefor” can take multiple addresses in a comma-separated list.

Public transactions: Transactions whose payloads are visible to all participants in the same Quorum network. These are created as standard Ethereum transactions in the usual way.

The Enterprise Ethereum project consists of an “enterprise-grade stack” and provides tools for users who demand privacy of transactions – a major pain point for financial institutions today.

What we think

François Genaux, Financial Consulting Leader

Today’s world is made up of markets of intermediaries. The future in the nascent blockchain world will see marketplaces without intermediaries and direct venues between offer and demand. We must also bear in mind that any shift to an asset-management industry driven by blockchain technology will be a step-by-step adoption rather than a big-bang revolution.

If you’d like to know more about how market players will see their roles evolve, check the report we’ve published jointly with Fundchain here.