The PSD2 is the revision of the first Payment Services Directive (PSD) that the European Commission adopted in 2007. It aims to regulate the activities of payment service providers and to create a harmonised framework across Europe. With this new regulation we expect an increase in the number of providers in the ecosystem and new internet-based business models. Greater choice and transparency for consumers are part of the “combo” the regulations wants to foster. While this can be seen as an opportunity for big companies, Fintechs face several challenges. One of them is to comply with all the new regulations, despite their digital advantage and their ability to quickly adapt to users’ needs and expectations. Can Fintechs take full advantage of the PSD2 wave and collaborate with banks to stand out successfully? This is what we explore in this article.

The impact of PSD2 in the online payment landscape

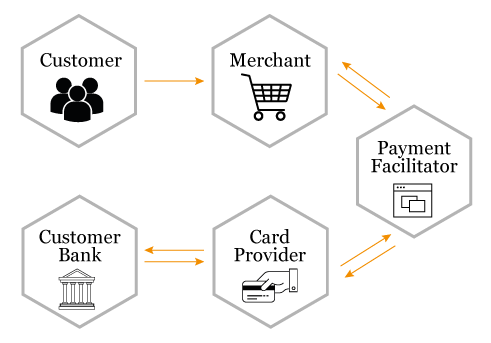

The European Commission sets out to improve customers’ security and lower barriers to foster innovation. There are two new main payment services: the Payment Initiation Services (PIS) and the Account Information Services (AIS).

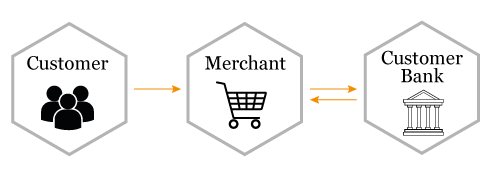

The Payment Initiation Service Provider (PISP) gives customers the chance to bypass traditional intermediaries by allowing third parties to make payments from their bank account. The Account Information Service Provider (AISP) gives third parties access to bank accounts and provides account aggregation services to the customer. Combined, these two changes open the door of the banking and payment landscape to new players, like Fintechs and GAFA ( the technology giants Google, Amazon, Facebook and Apple)

Yes, the PSD2 sets in motion the revolution of the payment industry by giving businesses, and payment service providers access to the golden pot at the end of the rainbow: the bank account.

All regulated institutions will be able to access the bank account given that the owner, the consumer, authorises that specific action that PSD2 regulates. All payment transactions within the EU and all payment-providing services have to, or will be, compliant. Juggling the requirements, the implementation of new regulated products, new security and risk management policies and procedures are the main challenges for Fintechs and other small companies.

At the same time, new doors opened for new payment methods and business strategies. Sinead Ovenden, PwC Ireland financial services partner, explains that the introduction of PSD2 on 13 January this year created a level playing field for new entrants and traditional market players offering financial services. It offers more opportunities for competition and innovative payment service providers. PSD2 changed the payments landscape by putting an end to the banks’ monopoly over customer data and payment services. Market players will need to analyse the emerging payments landscape and identify new revenue opportunities for services, something most have yet to do, suggests Marco Folcia, PwC Partner and European PSD2 Leader.

The needed tech-approach means Fintechs are in the perfect position to take full advantage of PIS, AIS and open banking as they already have experience in using technology to enhance their business on a daily basis. They are now exploring new ground that once belonged to the banking sector, and use the data on customer behaviour to improve customer experience, understand spending habits and develop products and services banks didn’t provide before.

What are the current challenges for banks, online payment services and Fintechs?

As we move from an age of cash to one of online payment channels more online solutions will arise, and cash-based services are likely to lose ground compared to other payment means. Even so, both banks and online payment services face a few common challenges:

Card-based solutions dominate Europe and the U.S markets. If mobile solutions don’t improve the way they sell themselves online, customers are unlikely to be receptive or willing to try them.

No new technologies, no gain. If companies don’t use the newest technology, less customers will be interested in adopting it.

Lack of consistency of mobile payment methods in the payment markets. Customers are unable to know in advance which stores use a certain type of mobile payment. Customers then, may fall into a state of uncertainty and doubt when adopting mobile systems in the long-term. Why embrace something you won’t be able to actually use all the time?

The factors described above are only a piece of the puzzle that connects to another: customer behaviour. To Marco Folcia, banks need a proper strategic response to avoid becoming disintermediated by more customer-oriented third-party offerings. Payment markets across the globe differ depending on the region they’re implemented as the adoption will depend directly on customer behaviour and whether modern payment systems are in place.

When it comes to open banking, we can’t expect a significant change overnight. Ovenden explains that it will take some time for open banking to fully evolve but, without agile change to data management, the traditional bank may become more of a utility, with Fintech solutions becoming a more common method for retail transactions.

For Fintechs, the challenges differ. There is need for a team-up between Fintechs and banks if both want to have successful impact in the years to come.

Even with the advantage of adapting quickly to the market and using the latest technology, Fintechs still have to make major investments to build user-friendly products, to build and maintain a client database compliant with the GDPR and ensure the level of security required to protect their data and their customers’ data. Ovenden notes that security will be important to ensure that customers still trust their bank services, and the balance between this and new, appealing services will determine consumer confidence and uptake. She emphasises that the security measures outlined in the regulatory technical standards need to be applied. We are now in a PSD2 transition period (between January 2018 and September 2019). The security requirements continue to be developed, as the interactions between providers and complexity of cybersecurity are vast.

What we think

Emmanuelle Caruel-Henniaux, Partner at PwC Luxembourg

How the Fintech industry overall will use PSD2 to their benefit remains to be seen, but their tech-first mind-set and their ability to create solutions to the new regulatory requirements will give them a boost in comparison to traditional methods of payment and regulated institutions. At the same time, it also means they are actively looking at the benefits of open banking, AIS and PIS, develop products internally, and convert them into marketable technology. In the end, if the potential of PSD2 is fully met in the upcoming years, everyone stands to benefit from the new regulation, from the traditional market players to Fintechs and to consumers.

Online payments post-PSD2

Online payments post-PSD2