Less than two years ago we wrote a blog entry about securitisation, in which we attempted to explain in layman’s terms what securitisation is, and examined the opportunities and challenges of these structures. In the article, we also looked at the Luxembourg securitisation market through our 2020 Securitisation Market Survey.

Now, it’s time to take stock of what has happened since then. What are the latest legal developments? How has the market in Luxembourg evolved? More generally, has the industry overcome the challenges brought by the 2008 financial crisis and the COVID-19 pandemic? This blog sheds light on these questions.

Don’t have time to read the whole blog entry? Then watch our “Blog in 1 minute” video for a quick summary of its main points:

New Luxembourg Securitisation Law explained

On 9 February 2022, Luxembourg securitisation participants were greeted with some exciting news. The Luxembourg Parliament voted for a long-awaited and much welcomed new law, with the aim to modernise the Luxembourg Securitisation Law of 22 March 2004, which had been in place for almost 18 years.

Indeed, the securitisation market has been experiencing significant developments since the past 10 years, however the legal framework and the Commission de Surveillance du Secteur Financier’s (CSSF) interpretation weren’t adapting accordingly… until recently. So, what has changed?

In a nutshell, the new law enables Luxembourg to become an even more attractive securitisation jurisdiction. The two major changes apply, on the one hand, to assets and, on the other, to the refinancing, bringing more flexibility for both.

It enables actively managed — by the vehicle or a third party — collateralized debt obligations (CDOs) and collateralized debt obligations (CLOs) to more easily set up in Luxembourg, and the refinancing offers more possibilities.

A brief history of the Luxembourg securitisation regulatory framework

Let’s take one step back to give you some context on how this new law came to life. Before, there were some practical challenges when structuring a deal. For one, the previous law required you to issue a security, however the definition of what a security is varies from country to country.

German investors, for instance, are fans of promissory notes, which, from an accounting angle, are quite similar to a loan but also have an additional security factor — so, they’re something in between, making the lines blurred. Given the ambiguity, it’s no surprise that there were questions about whether promissory notes were really a security and could be issued from a Luxembourg securitisation vehicle. There was no consensus on this point.

Then came the question: why not change the current framework to become more flexible on the liability side? And so, in the new law, the term “security” was replaced by the term “financial instrument”, making it clear that 100 percent loan financing is also possible.

In other words, now the refinancing of a transaction is no longer limited to securities but any financial instrument, including promissory notes or loans, as long as the repayable amount depends on the securitised risks.

This change aligns the new law with the European Securitisation Regulation (more on that later), which also doesn’t require financing solely in the form of securities. Furthermore, it will reduce the legal formalities and costs to set up those securitisations, which do not require securities financing.

Additionally, Luxembourg was lacking new legal forms, such as the limited partnership (SCS) and special limited partnership (SCSp). Now, the options of legal forms that can be used for a securitisation companies are enlarged by “société en nom collectif”, “société en commandite simple”, “société en commandite spéciale” and “société par actions simplifiée”, which have been established in Luxembourg law since the adoption of the Securitisation Law in 2004. This will make securitisation even more attractive for investors like private equity houses or family offices who already extensively use partnership structures in the Grand Duchy.

Luxembourg, Ireland and the securitisation race

It’s no secret that, Luxembourg is one of the two major securitisation locations in Europe for the simple reason that it offers better conditions and greater experience than other European countries. But, as we’ve just mentioned, it isn’t alone in the securitisation race. In fact, every quarter, it’s usually competing for first place with Ireland.

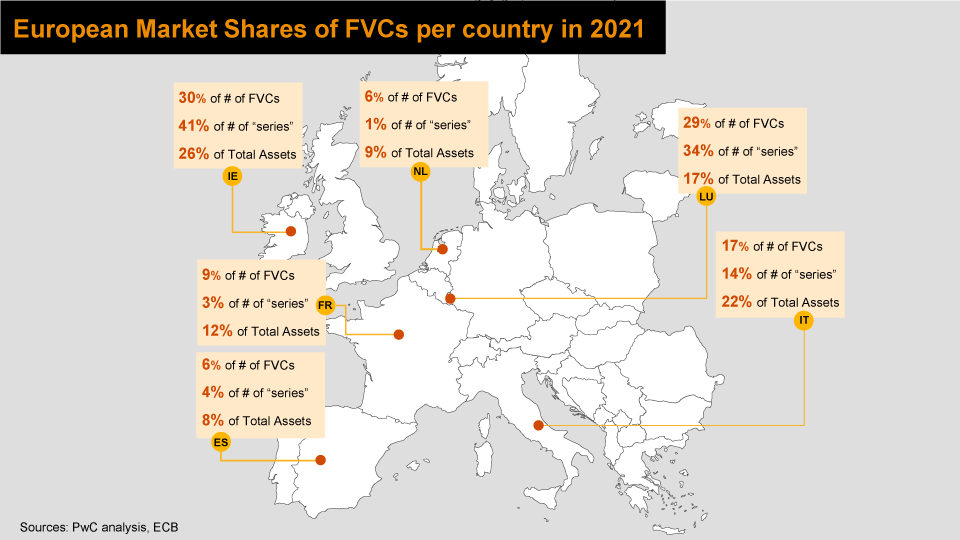

If we look at the latest numbers from the last quarter of 2021, Ireland is currently winning the race, but it’s a close one. The country currently has 30% of the number of Financial vehicle corporations (FVCs), while Luxembourg has 29%. When it comes to the number of “series”, Ireland has 40% while the Grand Duchy has 34%, and for total assets the percentage is 26% and 17% respectively.

Click to enlarge | Sources: PwC analysis, ECB

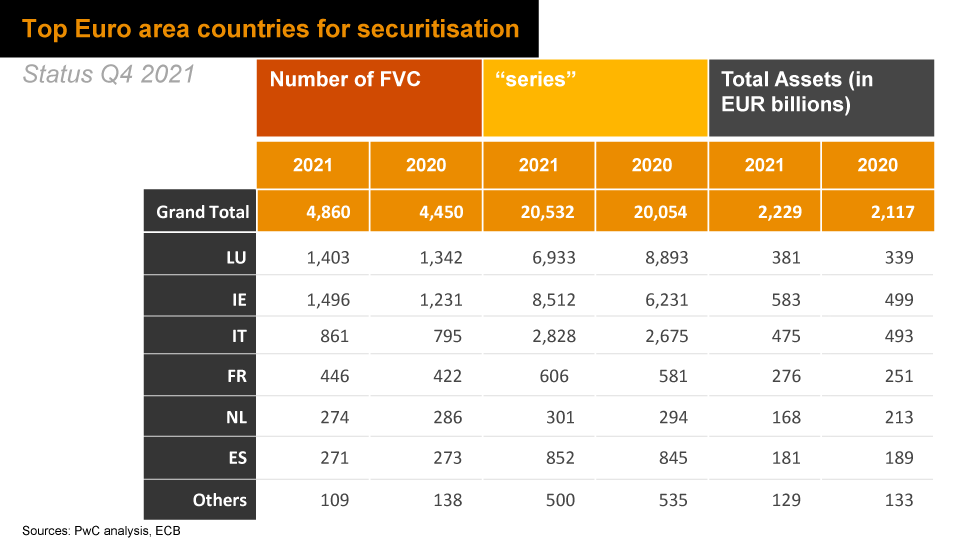

Click to enlarge | Sources: PwC analysis, ECB

The reality is that each country has to offer different attractive features that can be a decisive factor when opting to set up a vehicle in one country over the other. This said, Luxembourg has, without question, raised their game with the new law and while it’s currently behind Ireland, this could soon change.

Now that active management is allowed for Luxembourg securitisation vehicles for risks linked to bonds, loans or other debt instruments, the Grand Duchy might be able to gain some ground and attract more CDO/CLO structures that have historically rather been set-up in other jurisdictions such as Ireland, which were more flexible in this regard.

To give you a bit of background on this, in its Frequently Asked Questions on Securitisation published in 2007, the CSSF stipulated that the risk of a securitised position should only come from the asset itself — that is, from the performance of the asset — and not from the additional risk posed by the asset manager.

However, when an asset manager is managing a portfolio, there is not only a risk related to the assets not performing (that is, defaulting), but one also has to add the risk of the asset manager making the wrong decision — such as selling a well performing bond or loan, but then buying another one that will bankrupt in two months. To sum up, there’s an additional risk in such circumstances. This meant that CDOs and CLOs structures, which are abundant in Europe, ended up going to Ireland and The Netherlands, and not Luxembourg.

A small parentheses regarding The Netherlands. A few years ago, the Value Added Tax (VAT) rules changed in the country, so many vehicles moved out of the Netherlands to… you guessed it. Ireland! Once more, Luxembourg missed an opportunity because it didn’t offer the possibility of having active management.

Ultimately, it all comes down to timing. If the Grand Duchy had had the law two years ago, maybe more vehicles would have come to Luxembourg. As the expression goes, “could’ve should’ve would’ve”.

This said, the grass isn’t necessarily greener on the other side (meaning, Ireland, although it is quite green over there). From a legal standpoint, Luxembourg offers legal certainty on the compartment segregation, which Ireland currently doesn’t have. There are clear advantages for Luxembourg and now, with even more flexibility and a stronger toolbox, these advantages have increased.

While things are slowly starting to move in terms of the number of requests, especially in audit and tax, it will take some time to see the impact of the new law bear fruit. By that we mean between six to twelve months. This is because the good news first needs to be further spreaded, which is already happening, and the decision makers will also need to take the step to move to Luxembourg and set up the structures here.

A short note on the securitisation reputation

Once your reputation is damaged, it’s hard to recover it, but not impossible. Yes, it takes time, patience and usually encompasses making changes. And, as importantly, you must be given the benefit of the doubt when asking for a second chance.

This is more or less the case of the securitisation market. After a rocky period following the 2008 subprime crisis, which we touched upon in our previous blog article, the industry has slowly, but surely, rebuilt its reputation over the last five years.

This regulation establishes a general framework for securitisation on a European level and creates a specific framework for simple, transparent and standardised (STS) securitisation, also called “high-quality securitisation”. With this renewed push for securitisation in Europe, one can say with some confidence that its bad reputation has now been “forgiven and forgotten” by the market.

What’s next for securitisation in Luxembourg

At the end of the last quarter of 2021, Luxembourg had a total of almost 1,400 securitisation entities, of which about 1,310 were securitisation companies and about 70 were securitisation funds managed by around 53 Management companies. This is a 13 percent increase compared to the previous year that shows the Luxembourg securitisation market continues to grow.

However, there’s still one challenge for the Luxembourg securitisation market and that’s ATAD 1 (Anti-Tax Avoidance Directive) and, by default, the interest limitation rules. Once upon a time, some securitisation vehicles under the EU Securitisation Regulation were, thanks to the Luxembourg tax law, exempted from the ATAD interest limitation rules in Luxembourg. However, as the law changed, this exemption no longer applies.

The impact on the market isn’t that significant because usually these vehicles only entail interest income, and if you have interest income and pay interest to your investors, you are fine. However, if you have any income other than interest income (referred in the regulation as “borrowing costs”), the securitisation vehicle could be taxed on part of its income, which will ultimately affect the revenues of the investors. In a way, this goes against the very core principle of a securitisation vehicle, which should be more or less tax neutral.

In Ireland, on the other hand, tax authorities have been more accommodating. So much so they have come up with a sort of single company world wide group. This means that if your structure only includes a securitisation vehicle and one stichting (one single shareholder) behind it, you are exempted from the ATAD interest limitation rules.

To sum up, Luxembourg is at a disadvantage here as there is still a lack of clarity on the ATAD 1 interest limitation rules. So, watch this space for future updates.

This long-awaited law introduces some small but very important adjustments, and further increases the flexibility and legal certainty of Luxembourg securitisation transactions. It also spells out aspects that weren’t so clear in the previous law. This law, which stems from the market participants’ needs, has a positive impact in the industry and, hence, it’s much appreciated by all stakeholders. I expect to see new structures being set up in Luxembourg in the near future.