Everlasting growth has been the panacea of the socio-economic model we live in today, a logic not unlike the big bang theory expansion. However, this single idea is increasingly blamed for fueling the latest global economic crises and for aggravating the climate issues we face today. This criticism comes at a high stake because it shakes the ground on which we have cemented prosperity and, therefore, the future we like to imagine for ourselves.

But Mother Earth seems to have other plans. She knows better, conscious about her own limits. Climate change is the most cited danger of the climate crisis, but loss of biosphere integrity, ocean acidification and six other ecological boundaries join the “dark green, almost black” list or environmental perils.

We’re at the crossroads of deciding our greener future. Time is falling short.

Things are moving forward and that’s both encouraging and positive for Mother Earth and for our own sake. One can see that different stakeholders are converging around the idea of a greener future, notably politicians, lawmakers and businesses. For now, the E of ESG —Environmental, Social and Governance— seems to have overcome the S and the G, although we know that all of them are important. Perhaps, the urgency of our present is dictating this temporary preponderance.

A vivid example of this climate crisis is the COVID-19 pandemic. The “coronavirus” story is a reminder of the need for a healthier ecosystem and for working more coordinately and firmly in climate policies.

The content of this article stems from two of the most interesting matters discussed during the 2021’s edition of the “Journée de l’Economie” (JE) event held, mostly virtually, in late April. Both start with the same three letters “t-a-x” but their etymologies are diametrically different. Taxation, from Latin “taxare” means “to charge”; taxonomy, on the other hand, from Greek “taxis”, means “arrangement”. They are set to become key pieces to find the solution to the puzzle called “green future”.

But what’s “green”? The role of taxonomy in sustainable investing

In financial services, especially in the asset and wealth management realm, the question “which investments are sustainable?” is echoing in the air.

With the rise of ESG and the growing commitment of the European Commission (EC) to enforce regulation that can materialise the climate-neutral objective —an economy with net-zero greenhouse gas emissions— set by 2050, the echo is even louder.

At this point, a large number of financial services organisations know they are bound to become key players in the path towards a greener future.

But clear rules and workable action plans are required to achieve far-reaching goals. And the rule-action binomial follows a cause-effect pattern. That’s why taxonomy is so crucial to the “ESG promise”, namely, for ESG becoming the catalyst for a paradigm shift in business. Taxonomy for sustainable finance discerns what is sustainable and what is not, and brings consistency and coherence among all market players in terms of product and service development, compliance and reporting.

In April 2021, the European Union (EU) approved the draft of the EU Taxonomy Climate Delegated Act which includes a classification of economic activities considered environmentally sustainable as per EU law. This document, yet to be reviewed, derives from the Taxonomy regulation that “empowers the Commission to adopt delegated and implementing acts to specify how competent authorities and market participants shall comply with the obligations laid down in the directive”.

Four future legislative initiatives will stem from the Taxonomy regulation which, in turn, includes six environmental objectives. And here is the golden rule: for an economic activity to be considered sustainable, it needs to positively impact one objective (substantial contribution) without harming the others.

Environmental objectives established in the Taxonomy Regulation

The current legislation is only a part of a legislative pack, with 70 economic activities included for the time being, and six sectors covered (forestry, manufacturing, electricity, sewage, transport, building). The Commission will work on transition finance policy and will produce a handful of social taxonomies too.

Who will pay for the transition to net zero?

The path towards a greener future is anything but linear and free of obstacles in the horizon. Scattered along the way are pop up questions that affect stakeholders individually or collectively. And the ones that are finding answers today might be only a part of a longer list yet to come.

In fact, “What’s green” isn’t the only question echoing in the air nowadays. A second one, even more structural, addresses one of the most fundamental questions of all: who will pay for the transition to net zero?

Among the panelists who participated in this year’s JE event, one person’s opinion recalled the years that followed WWII, in which the role of states was fundamental to rebuild the world’s economy. Large public investment created not only jobs that generated tax revenues in return, but also credit. Following this line of thought, the role taxation can play as a catalyst for the transition to a carbon neutral economy doesn’t seem so far-fetched.

In December 2019, the EC issued the European Green Deal 2019, a leap frog step towards becoming climate-neutral by 2050. The document, which includes a wide range of measures to reduce carbon emissions, gives taxation an important role in the transition, acknowledging that “well-designed tax reforms can boost economic growth and resilience to climate shocks”. The deal also declares that “ensuring that taxation is aligned with climate objectives is also essential”.

However, achieving the objective of transforming the EU’s economy requires a set of measures to work in tandem. Among others, the EU Green Deal definespolicy reformsto ensure effective carbon pricing throughout the economy, encouraging changes in consumer and business behaviour, and facilitating an increase in sustainable public and private investment. If the roadmap is executed timely, the EU will produce a 55 legislative package that includes the revision of the EU Emission Trading System (EU ETS) and the Energy Tax Directive, among other 50+ regulations.

Moreover, in this document, the EC promises to help companies to become world leaders in clean products and green technologies.

The carrot-stick approach of taxation

Often, taxes are a synonym for a (heavy) burden.

Indeed, few can deny having had a certain sense of unease when the time to meet tax responsibilities arrives. This is also because we aren’t always that conscious of its benefits when it’s properly invested for the good of the public.

Carbon taxation, which can be considered a sort of “pollution tax” —a fee imposed on businesses and individuals— and other environmental taxes shouldn’t necessarily translate into a higher tax burden.

Taxation policies can drive behavioural change with targeted measures addressing individuals and/or businesses. The sanction approach to taxation or “the stick” equals to payments or to penalties (in case of non-compliance); the incentive approach or “the carrot”, on the opposite side, can be explained as a benefit obtained after having observed certain expected behaviour.

Both types of policies coexist in Europe. Currently, tax incentives (the carrot) are almost at the same level as stick-like taxation. For instance, the subscription tax reduction for sustainable investments (as defined by EU Taxonomy Regulation 2020/852) in Luxembourg or the Energy Transition Tax Credit (CITE) in France, which addresses individuals and is applicable to up to 30% of the cost of works to improve energy efficiency, up to a limit of €8,000 for a single person and €16,000 for a couple. Equally, by granting subsidies to e-cars or hybrid car owners, the German government incentivises taxpayers to buy electric vehicles.

In the race to reach the zero emissions goal by 2050, there are, as we have already discussed, many questions, perhaps because it is the first time in history that we are working together towards a goal of such a magnitude. And carbon taxation doesn’t escape the interrogation room.

Which approach, the stick or the carrot, is more impactful for the greener economy, to drive change? Or, to whom should one give the carrot, the producer, the final consumer, or distribute it among all stakeholders?

(Re) distribution and (re) investment are what’s expected from this type of policies and any measure on this regard calls to consider carefully the perspective of the taxpayer and the perspective of the state alike. Certain countries have had issues linked to distribution of taxes. Because, are they going back into the economy or supporting the greening of the economy? Or are they addressing less-favoured sectors of society?

We still have a long learning curve in this regard. The good news is that we have already started.

Environmental tax, the EU case

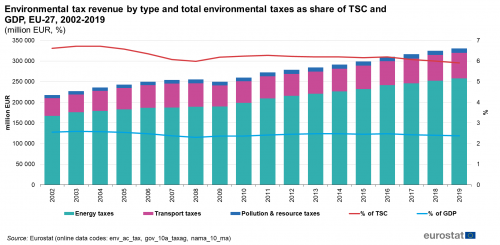

According to EUROSTAT, the 2019 value of the EU environmental taxes was EUR 331bn. Although it is about EUR 113bn higher compared to 2002, it has decreased from 2.6% to 2.4% in relation to GDP. Also, the ratio of environmental tax revenue and EU government’s total tax revenue (taxes and social contributions) decreased from 6.6% in 2002 to 5.9% in 2019.

Environmental Tax Revenue by type and total environmental taxes as share of TSC and GDP, EU-27, 2002-2019 (source: Eurostat)

As we can see, EU environmental tax revenues haven’t increased over time; on the contrary, they have slightly decreased. Because of this tax revenue erosion, governments will have to consider and evaluate other types of taxes that can fill the gap. Among the existing four types of environmental taxes – energy, transport, pollution and resources – the energy tax’s revenue was the only that grew in the period mentioned above because of raises on fossil fuels taxes.

Moreover, due to changes in consumption patterns, existing environmental tax revenues may be greatly reduced, for instance if people drive electric cars massively, something already happening in Norway. When energy taxes won’t be effective, will it be necessary to tax electricity higher, for instance, or think about taxation on alternative energies at some point?

In Luxembourg, EUROSTAT reports that the share of revenues of environmental taxes was 4.4% by 2019 (ratio of environmental taxes to total social contribution). This tax didn’t follow any “stick or carrot” approach, however. The motivation behind it has been primarily economic (to attract, what is called, the “fuel tourism”) and, when it was created, it didn’t intend to influence or change any behavior anything. Let’s mind that any increase in carbon taxation – tax on fuels, more precisely – will likely be translated into a decrease in revenues.

During the event, several voices called for Luxembourg to pay special attention to redistribution matters and to think of other energy sources that can be used once fossil fuels fall into oblivion or are socially deprecated.

Incentivising indirect stakeholders’ engagement in the environmental taxation issue

The greener future calls for as many stakeholders involved as possible, either because they are the ones paying taxes or because they are called to change behaviours induced by environmental taxation policies.

To engage indirect stakeholders, some of the possibilities discussed during JE 2021 were extending credit systems, applying super tax deduction for those investing the adoption of greener technologies or in bringing about innovation in green tech, and reductions in tax.

According to a quick survey done during the event, 20% of participants thought that the first option was the best; the two latter options got 40% each. These results coincide with what PwC Luxembourg’s experts had thought as the most effective tax-related ways to drive behavioural change in indirect stakeholders.

Combining stick and carrot taxation policies seems to be the approach to follow. What is needed is a fiscal policy package addressing countries’ specificities linked to the different stakeholders that take part in the taxation equation; groundbreaking measures justified by the country’s specificities.

What we think

François Mousel, Partner, Clients and Markets Leader at PwC Luxembourg

Like Julius Cesar once did, we have “crossed the Rubicon” for our greener future, and there is no point of return, especially because time is running fast and, to many, falling short. And while there isn’t a nation to conquer, there is a planet to preserve, hence we should not shy away from using all tools at our disposal, including strong incentives.

Learn more about the “Journée de l’Economie 2021” here.