Julia Gillard, who served as the 27th Prime Minister of Australia and Leader of the Australian Labour Party from 2010 to 2013, once said “Our future growth relies on competitiveness and innovation, skills and productivity. These in turn rely on the education of our people.” While Julia has a valid point, we add sustainability to the mix.

Competitiveness can be a catalyst for innovation, driving individuals, businesses and countries to be more creative when it comes to solving local and global issues. It can also push industries into taking one giant leap out of their comfort zone to overcome self-imposed barriers on their long-term objectives. But, ten years on from the global financial crisis, what will it take to remain on top? We see one of these solutions as sustainable finance.

Did you know?

According to the European Commission*, ‘sustainable finance is the provision of finance to investments taking into account environmental, social and governance considerations.’

What do we mean by competitiveness?

The simplest definition is the one proposed by the World Economic Forum (WEF): ‘the set of institutions, policies and factors that determine the level of productivity of a country’. A competitive economic environment is, we assume, a productive one. Productivity leads to growth, leading to high income levels.

In Luxembourg, in an effort to improve the competitiveness of companies and to reduce their production costs, the local political authorities created a legislative framework to instigate the development of the country’s economy. Historically speaking, the Grand-Duchy managed on several occasions to set up favourable business development policies by developing and integrating modern, solid and innovative legal frameworks. Those efforts didn’t come without some victories, mainly in a consistent excellent performance in various international studies on competitiveness.

When it comes to competitiveness, Luxembourg is an example to follow. The country has learned how to tick all the right boxes. It boasts a robust and diversified economy, with solid political, economic and regulatory stability, instigating a solid base for investor protection. According to the Global Competitiveness Report 2018, published by the World Economic Forum, Luxembourg ranked 19th out of 140 territories.

Situated at the heart of Europe, Luxembourg has made huge inroads in terms of innovation and has invested substantial financial and organisational resources into specific sectors. Start-ups are incubated and coached in both public and private spaces for their early development and provide with access to services and support. Government sponsored agencies such as Luxembourg for Finance, Luxinnovation and Luxembourg Trade and Invest are dedicated to building on the country’s unique selling points, attracting business and raising the international competitiveness bar.

Robustness and agility are built into Luxembourg’s national character. The financial centre has a positive track record of adapting to a changing environment and offers a diverse range of financial services connecting investors and markets around the world. The financial centre’s unique cross-border expertise attracts financial service providers from around the globe, while Luxembourg’s capital markets infrastructure makes it the ideal place for companies of all sizes to finance their European and global activities.

Being the first to implement the UCITS Directive into national law, and the first to launch a global platform dedicated only to sustainable financial instruments, theLuxembourg Green Exchange, shows the innovative mindset of this financial centre. Luxembourg is a hub for developing sustainable products that contribute for a greener future.

In this article, we show the main challenges of the banking sector both globally and in Luxembourg and how our financial centre has, and can, find opportunity with future proofing and sustainability in mind.

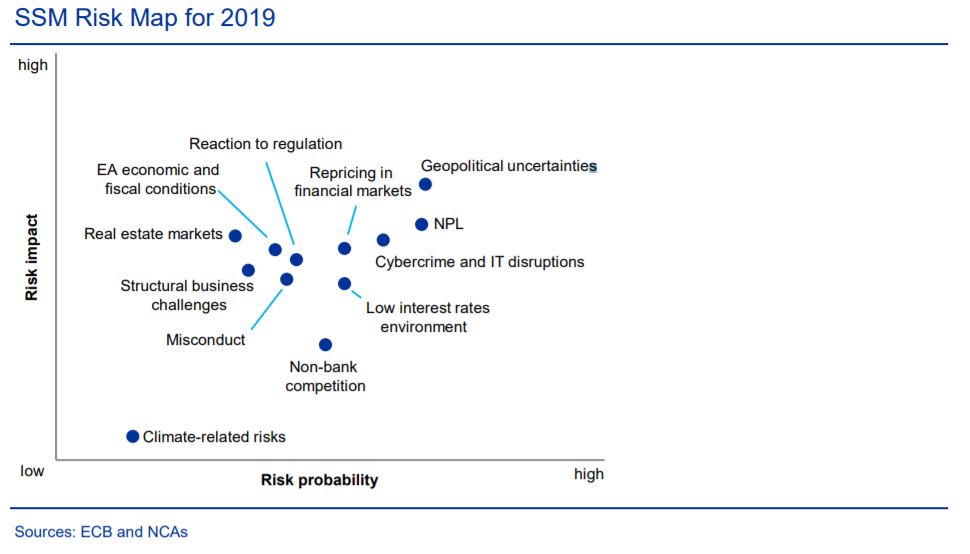

What are main risk drivers of the European banking industry?

Out of these we selected three to discuss: geopolitical uncertainty, non-bank competition, cybercrime and IT disruptions (as one topic). Let us summarise them in a few sentences.

Geopolitical uncertainties

It’s no surprise to find that political uncertainties both inside and outside of Europe have recently increased. Brexit is just around the corner but the final stages of the transition and the withdrawal agreements still represent mere attempts. Banks and supervisors continue to develop their contingency strategies, taking into consideration challenges that range from business continuity and transitional risks, regulatory risks and macroeconomic repercussions. Also, concerns related to rising trade protectionism and escalation of trade disputes are reaching new levels. The development of some emerging market economies might have a negative impact on Europe’s financial markets. Finally, the risk of global regulatory fragmentation imposes an additional vulnerability.

Non-bank competition

The competition is tightening as mainly fintechs enter financial markets. Certain industries that only faced local competitors, find themselves competing with far more dynamic entities. In the banking sector, traditional banks, that relied heavily on stature, conservatism, longevity, good reputation and solid processes and strategies, now face new banking challengers who are able to adapt much more quickly to these changing times and the needs of the consumers.

Cybercrime and IT disruptions

Cyber criminals are growing more sophisticated. Companies are under mounting pressure to invest heavily in cybersecurity. Cyber incidents can lead to financial losses and indirect ramifications that destroy customer confidence such as a leak of customer data. At the same time, banks must modernise their core IT infrastructures to reduce costs, provide a better customer experience and become more efficient. As fintechs are quicker to adapt to customer demands, and big technology companies have access to a vast pool of client databases, “Jurassic” banks need to step it up if they do not wish to become extinct.

What are the main concerns in Luxembourg’s banking sector in 2019?

The world continues to break economic and technological barriers. All industries are being pushed away from their traditional silos in order to keep up with market and customer behaviours. Luxembourg is no exception. The global concerns we mentioned above also affect the local banking sector.

New market entrants that were attracted by Luxembourg’s favourable environment turned the local banking landscape upside down. How? Because traditional banks are forced to rethink their strategies, processes and customer relationships, hence creating a new generation of service offerings.

Keeping control over costs and compliance has never been so critical. In Luxembourg, defining new target operating models, adapting to a new operating environment and reshaping existing procedures or processes, as well as reconsidering IT infrastructure, systems and applications are permanent challenges for banks operating locally.

The digital maturity of Luxembourg banks is still lower compared to other European countries. However, they’re investing and putting their efforts into digitalisation and are still running the race for transformation to fully address customer expectations.

Technology continues to make its way through business operations and processes. It seems ironic but in the digital age, how banks interact with, and service, their customers is still the biggest differentiator. From anticipating a loan or a mortgage to the potential use of bank data to provide insights to support corporate clients’ business strategies, the method of delivery of these demands will be more embedded in businesses objectives.

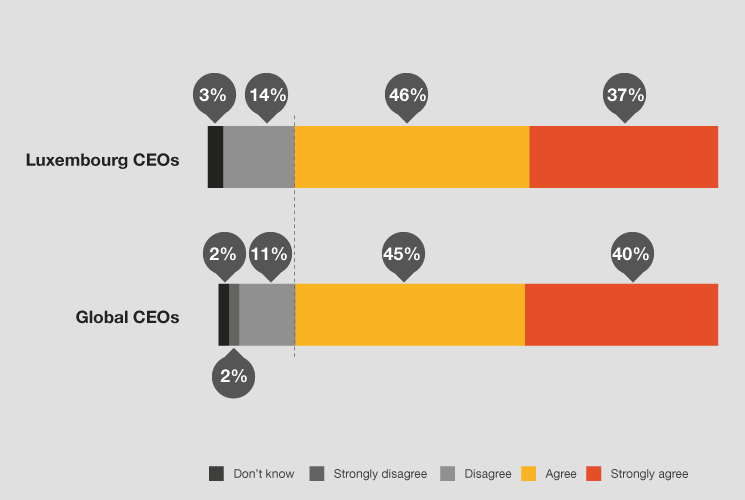

In Luxembourg, according to our CEO survey over 80% of CEOs believe that AI will significantly change the way they do business, according to our 22nd CEO Survey – Luxembourg findings(see graphic below). We also have to take into account that AI will also impact client relations and help anticipate customer needs.

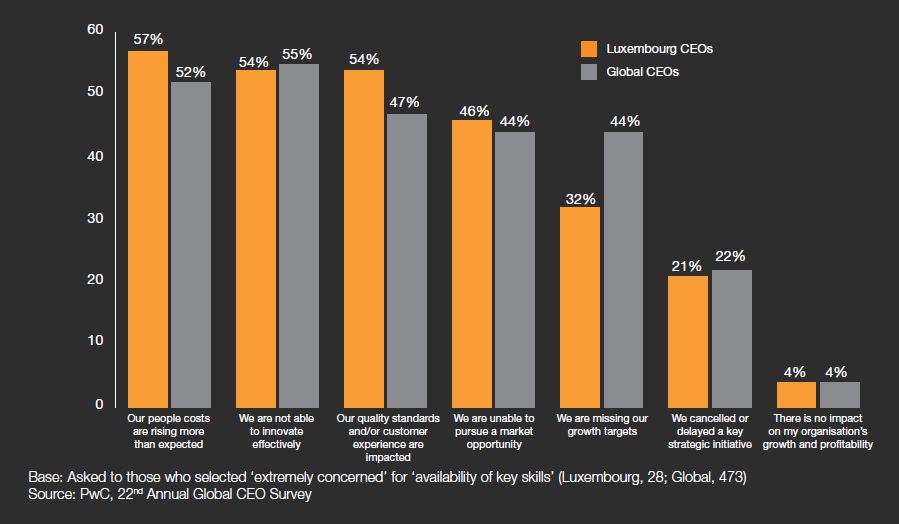

Directly related to technology’s impact, CEO’s are confronted with a need for higher skills and new types of expertise. 57% of Luxembourg’s CEOs stated that people costs are rising more than expected. This is impacting their capacity to innovate effectively as well as the quality of their customer experience.

In Luxembourg, hiring from competitors is common practice, but in turn it creates a rise in salary costs. Much like with global CEOs, Luxembourg CEOs see upskilling as the main solution to fix the talent gap. They struggle to recruit the right people with the right skill set, especially as technology is becoming a mandatory tool in financial services due to the growing customer demand. According to our latest Banking and capital markets trends 2019, we can’t forget that technology isn’t everything. While operations continue to become automated, machines aren’t able to replicate human traits. There’s a need for a human workforce with strong soft skills creativity, empathy and leadership to create balance with the digital world.

To tackle the skills gap and the impact technology has in specific industries and sectors, the ‘Digital Skills Bridge’ initiative was put into place in May 2018. It aims at providing technical and financial assistance to upskill employees in companies facing major technological disruptions.

What does the future look like?

Sustainable finance might have the potential to answer these and other important questions with regard to the future of the financial sector.

Sustainable finance has a long history – already in 1972, the report entitled, “The Limits to Growth” written by the Club of Rome, shifted the focus towards a sustainable economy. Considering sustainability in modern business, the COP 21 Agreement was signed in 2015 by 185 countries in Paris marking another turning point for sustainable finance. Since then, the joint commitment of many different stakeholders of ecosystems around the world (e.g. governments, regulators, international organisations, private institutions) has also started to involve the world’s financial sectors in the fight against climate change and to contribute to a more sustainable future.

In particular, Luxembourg has developed into an international platform for sustainable, social and green finance. The latest Global Green Finance Index (GGFI) shows that Luxembourg ranks among the top Green Financial Centres worldwide and contributes to a more sustainable global economy. Forecasts made by GGFI indicate that Luxembourg’s sustainable finance offerings will improve significantly in the short- to medium-term.

Following the rising importance of sustainable finance, and as a contribution to the development of Luxembourg’s Financial Centre, the concept of Impact Banking has been developed. It aims to position Luxembourg’s banking sector as a front-runner in the field of Sustainable Finance.

The concept of Impact Banking will empower banks to utilise Luxembourg’s USPs – e.g. its globally unique financial ecosystem, its regulatory agility, its market access or its specialised human capital – to:

Rapidly develop new – sustainable – business models, products and services;

Actively shape and influence the development of new regulations in the field of sustainable finance;

Benefit from the ‘first mover’ implementation of new EU regulations and requirements long before international competitors do; and

Drive sustainable revenues within their group as sustainable finance competence centre.

One question remains, what is the future of sustainable finance?

Sustainable finance will take two different paths. On the one hand, sustainable finance will face an increasing professionalism. Sustainable business models will have to meet rising market specific and regulatory requirements. Intermediary financial companies have not only to assess their own actions in sustainability, but to differentiate between superior and inferior investment opportunities. On the other hand, risk factors resulting from climate change and European Commission rising social uncertainty needs to be assessed. Financial companies especially have to examine these risk factors on their debtor’s default probability and their climate adaptation abilities.

What we think

Roxane Haas, Partner at PwC Luxembourg

“Technology is changing our world and is embedded in everything we do, but it is people and humans who drive transformation in financial organisations. Our workforce in banks will strengthen their collaboration with technology and machines will never replace the empathy and creativity humans have. A “tech-savvy humanist workforce” is key for the future of banks.”

Michael Hauer, Director at PwC Luxembourg

“One of the core success factors in developing sustainable business models will be the alignment of the corporate strategy and the investment approach with the product or service strategy in a credible manner. The access to new markets and client segments will drive the long-term value for future oriented market players in the field of sustainable finance. Fintech will ensure its efficiency.”